US futures

Dow futures +0.35% at 34445

S&P futures +0.01% at 4197

Nasdaq futures -0.35% at 13654

In Europe

FTSE -0.1% at 7015

Dax -0.2% at 15423

Euro Stoxx +0.3% at 4042

Learn more about trading indices

Stocks trade mixed as inflation concerns creep in

US stocks are set for a mixed open after mixed data and less dovish Fed speak.

Beating forecasts, initial jobless claims fell to 406k. This is down again from the previous week’s reading of 444k and below estimates of 425k. It is a new pandemic low as the labour market recovery appears to remain on track. The numbers bode well for next week’s non-farm payroll numbers.

Q1 GDP held steady at 6.4%, missing forecasts of an upward revision to 6.5% QoQ.

Separately US durable goods orders fell 1.3% MoM in April, down from 1.3% growth in March.

The stream of data comes in the wake of a slightly more hawkish tone from the Fed’s Randal Quarles who suggested that the time to start taper talk could be nearing.

More hawkish Fed

The broadly upbeat data combined with Fed Quarles’ comments is driving up treasury yields which have popped back above the key 1.60% level. With inflation expectations and expectations of an earlier move by the Fed on the rise tech stocks are coming under pressure whilst the rotation into value appears to be back in play. The Dow Jones, the index most closely tied to value stocks is outperforming its peers.

Markets are looking jittery ahead of tomorrow’s PCE data, the Fed’s preferred measure of inflation. Given how sensitive the markets are to inflation expectations and Fed tightening concerns, we could see elevated levels of volatility heading towards the reading.

Equities

More retailers will be releasing quarterly results today. These include Best Buy, Dollar General and Costco. Software maker Salesforce is also due to report.

NVIDIA will be in focus after reporting forecast beating Q1 results with revenue up a staggering 90% compared to last year.

Snowflake trades 3% lower pre-market after the cloud software company revealed faster than expected revenue growth of over 100%. However, losses also grew faster than forecast, doubling across the period.

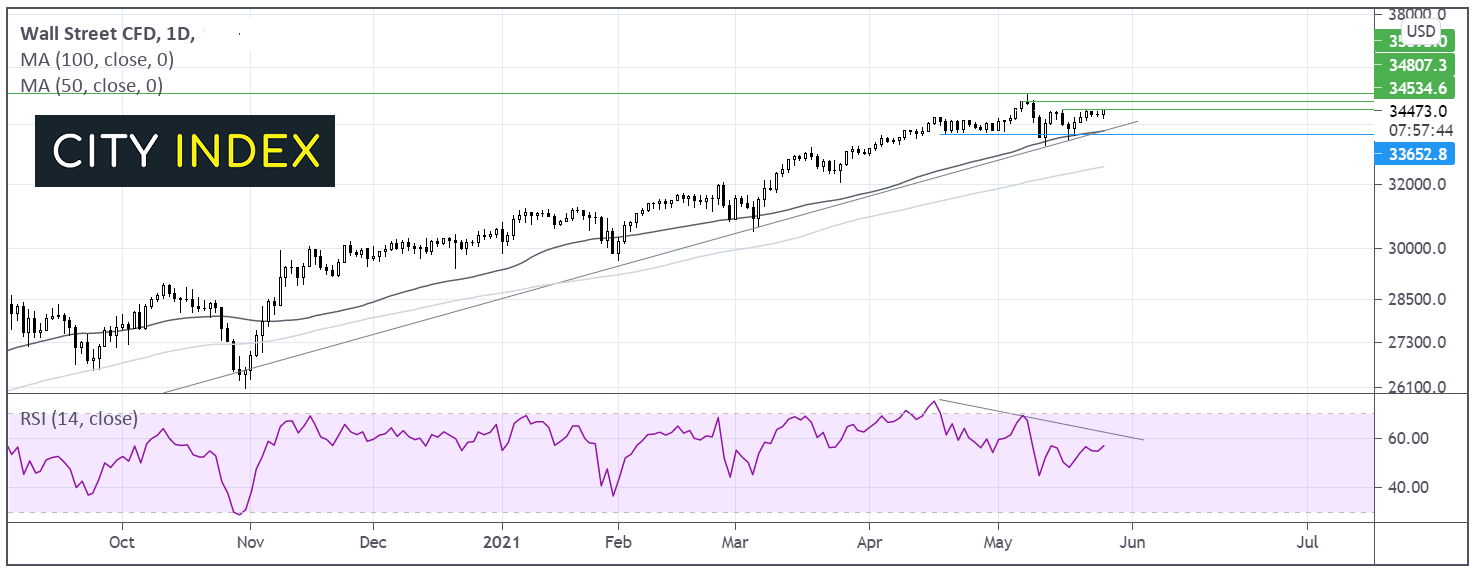

Where next for the Dow Jones?

The Dow Jones continues to trade above its ascending trendline support dating back to early April last year, although the price has struggled to push past last week’s high of 34500. A move beyond here is needed to attack 34850 and push on to 35000 the all time high. However, its also worth noting the negative RSI divergence which suggests that momentum is waning and can precede a move lower. A move below 33650 the 50 sma, horizontal support and the ascending trend line support could negate the near term up trend.

FX – USD pauses after solid rally, EUR lackluster after German consumer confidence misses

The US Dollar is edging lower after strong gains in the previous session. The US Dollar Index rallied 0.5% on Wednesday after a subtle shift in tone from Federal Reserve Randal Quarles, who, inline with the latest FOMC minutes suggested that the time for taper talk could be approaching.

EUR/USD is failing to capitalize on the weaker greenback following weaker than expected German consumer sentiment data. GKF sentiment survey ticked higher to -7, up from -8.6. This was short of the -5.2 expected.

GBP/USD +0.3% at 1.4171

EUR/USD -0.15% at 1.2194

Oil awaits further clarity on Iran, EIA data

Oil continues to consolidate around $66 on Thursday as the bulls pause for breath after a strong run up at the start of the week.

The oil market continues to weigh up re-opening optimism and the prospects of a strong US driving season against the possibility of Iranian oil lifting supply.

Indirect Iran – US nuclear talks begin again this week. The oil markets will be watching for signs of progress which could lead to the sanctions on Iranian oil exports being lifted. Any such move would see oil supply ramp up gradually in the second half of this year and heading into 2022 so demand should be well on the road to recovery by then which is keeping oil supported at these levels.

US crude trades -1% at $65.45

Brent trades -1% at $68.00

Learn more about trading oil here.

The complete guide to trading oil markets

Looking ahead

15:00 Pending Home Sales

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Latest Crude Oil articles

April 22, 2024 04:00 PM

April 19, 2024 03:35 AM

April 17, 2024 05:00 PM

April 17, 2024 03:02 AM