US futures

Dow futures +0.36% at 36376

S&P futures +0.45% at 4735

Nasdaq futures +0.78% at 15963

In Europe

FTSE +0.78% at 7543

Dax +0.39% at 16002

Euro Stoxx +0.75% at 4311

Learn more about trading indices

7% inflation fails to stall equity rally

US stocks are set to open higher shrugging off surging inflation, as the broadly inline reading eased concerns of a faster move by the Fed and as investors continue to find comfort in Jerome Powell’s testimony before Congress.

US CPI jumped to 7% YoY in line with estimates and the biggest annual gain since 1982. On a monthly basis CPI rose 0.5%, ahead of the 0.4% forecast but also down from November’s 0.8%.

Core inflation jumped to 5.5% YoY, up from 4.9% and ahead of the 5.4% forecast.

Yesterday, before Congress, Powell reassured that the US economy could withstand the required rate hikes in 2022 to bring inflation under control. The Fed’s target rate for inflation is 2%, substantially below today’s print.

Inflation is rising on the back of supply chain disruptions in addition to rising wages as the employer’s struggle to fill millions of vacancies.

The Fed is widely expected to start raising interest rates in March and today’s data hasn’t changed that view.

In corporate news:

Lucid is expected to be in focus after it plans to build an electric vehicle factory in Saudi Arabia in the coming 3 to 4 years.

Didi Global is on the rise following reports that the ride hailing company’s Hong Kong IPO announced last month could happen in Q2 this year.

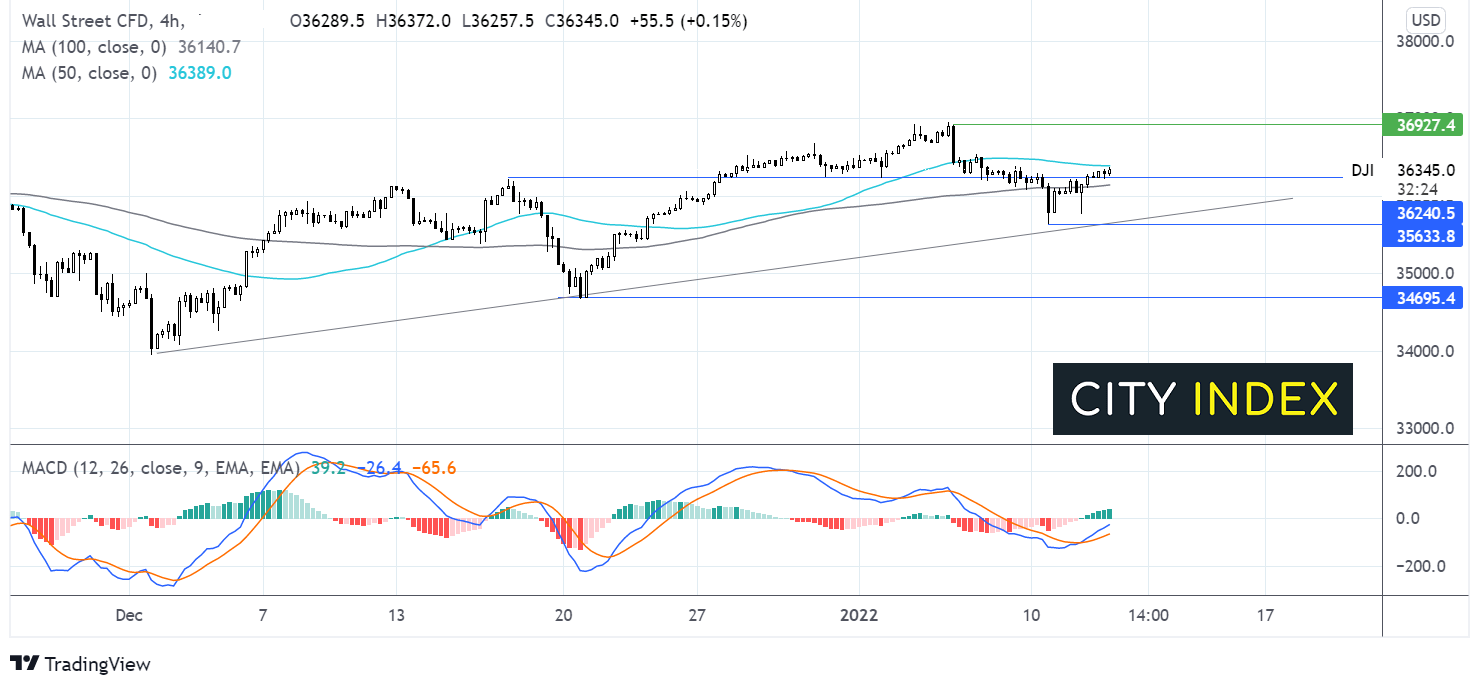

Where next for the Dow Jones?

The Dow Jones is extending its rebound from 35640 low hit earlier in the week moving above the 100 sma on the 4-hour chart and a key resistance level at 36200. The bullish cross over on the MACD is keeping buyers hopeful of further gains. Buyers will be looking for a move above 36400 the 50 sma in order to build towards 36900 and fresh all time highs. It would take a move below the 100 sma at 36140 to negate the near term uptrend and a move below 35630 for sellers to gains tractions.

FX - USD falls post CPI data

The USD is falling following the closely watched inflation data. The in line data eased fears of faster moves by the Fed to raise interest rates.

EUR/USD is allying as US CPI data drives the USD lower and the pair higher. The Euro shrugged off weaker than expected Eurozone industrial production data and an unexpectedly decline in German wholesale prices to 16.1% YoY, down from 16.6%.

GBP/USD +0.29% at 1.3674

EUR/USD +0.34% at 1.1406

Oil rises extends gains shrugging off Omicron concerns

Oil prices are on the rise as investors shrug off Omicron concerns instead finding confidence in Jerome Powell’s testimony before Congress. Powell said that the US, the world’s largest oil consumer should weather the current COVID surge with only short-term impacts.

Adding to the upbeat picture surrounding oil, OPEC+ producers are failing to reach their new upwardly revised output targets amid technical difficulties.

The current picture is bullish for oil and could result in oil prices rising quickly across Q1.

EIA crude oil stockpile data is due to be released.

WTI crude trades +0.3% at $81.00

Brent trades +0.2% at $83.54

Learn more about trading oil here.

Looking ahead

15:30 EIA weekly crude oil stockpiles

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels

- Place the trade.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest USD articles

Yesterday 01:12 PM

April 24, 2024 01:23 PM

April 23, 2024 11:09 PM

April 23, 2024 11:01 PM