US futures

Dow futures -0.4% at 34743

S&P futures -0.36% at 4390

Nasdaq futures -0.15% at 14906

In Europe

FTSE +0.03% at 7052

Dax -0.32% at 15698

Euro Stoxx -0.08% at 4120

Learn more about trading indices

Risk off dominates

US stocks are pointing to lower open on Friday putting the SP500 & Dow Jones on track for the worst weekly performance in 2 months.

Risk aversion has dominated across the week amid fears that the Fed will start tapering bond purchases as covid cases rise globally. The prospect of the Fed reining in support as new covid restrictions in some countries slow the global economic recovery is proving too much for the market to handle.

Safe havens have outperformed across the week whilst riskier assets such as stocks have tanked. Cyclicals have underperformed tech stocks.

Adding to the downbeat mood China continues with its regulatory crack down. The Hang Seng tumbled another 1.8% hitting a 10-month low. Chinese stocks listed in the US will be under the spotlight.

Safe havens have outperformed across the week whilst riskier assets such as stocks have tanked.

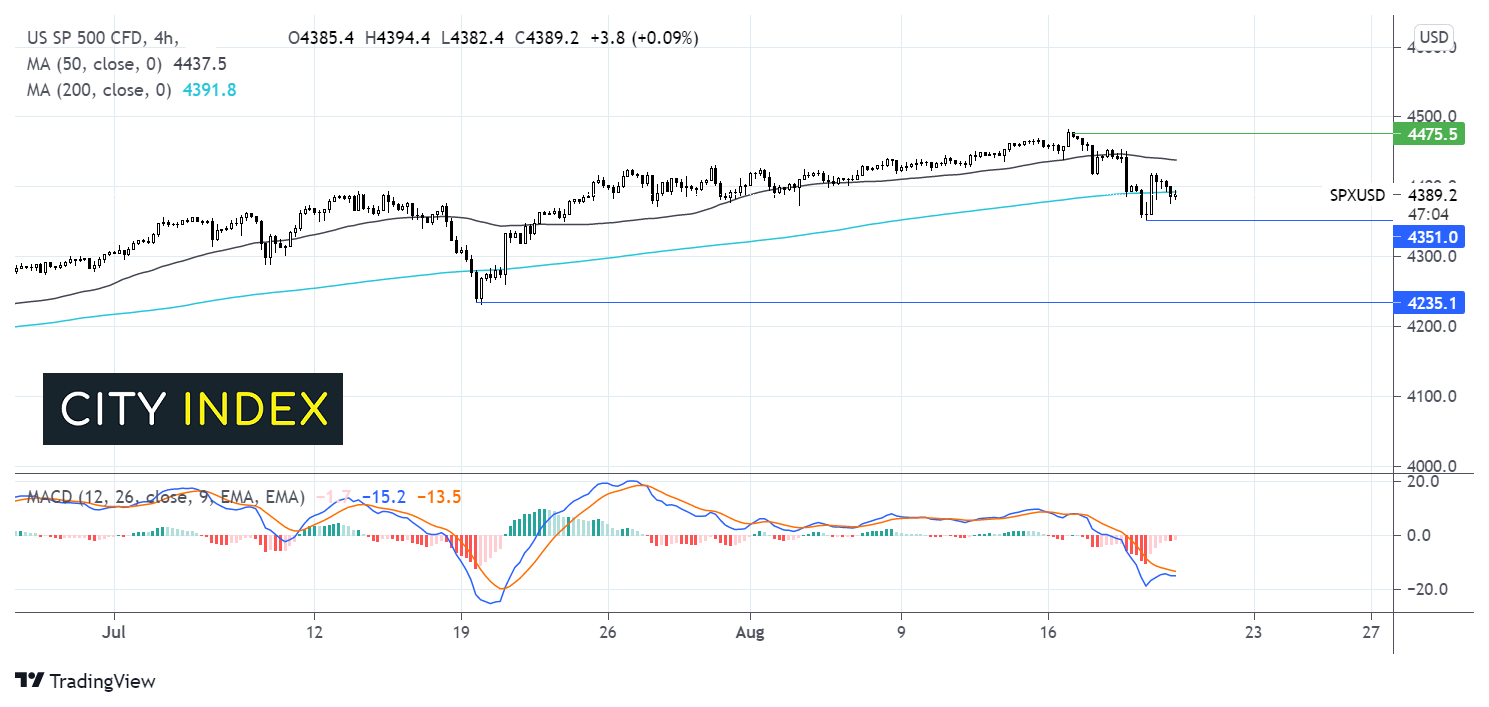

Where next for the S&P 500?

The S&P 500 is resuming losses after a mild bounce in the previous session. Yesterday’s move higher saw the S&P500 close over its 200 sma on the 4 hour chart which could bring some optimism to the buyers, as well as well as the receding bearish bias on the MACD. For now, the price is back testing the 200 sma at 4400. A break below this level could open the door to 4350 yesterday’s low before 4230 the July low comes into focus. On the upside resistance at 4440 the 50 sma with a push above here opening the door to 4475 and fresh all-time high.

FX – USD at 9 ½ month highs, GBP tumbles as retail sales fall

The US Dollar is on the rise extending gains from the previous session and hitting a fresh 9 ½ year high against major peers as investors seek safety. Fears are growing that the rise in COVID cases could dampen the economic recovery just as central banks are starting to rein in stimulus.

GBP/USD- the Pound trades under pressure after weaker than forecast retail sales data. UK retail sales unexpectedly fell -2.5% MoM in June, well below the 0.3% growth forecast. Retail sales tumbled as covid cases rose and Pingdom sent more and more people into isolation.

GBP/USD -0.22% at 1.3606

EUR/USD -0.06% at 1.1670

Oil moves lower for a fourth straight session

Oil prices have picked up off three-month lows but are still trading down around 5% across the week. Rising covid cases, tougher lockdown restrictions particularly in China Japan, Australia and New Zealand is raining concerns over the health of the economic recovery and weighing on the demand outlook.

US crude trades -0.92% at $62.90

Brent trades -0.88% at $65.70

Learn more about trading oil here.

The complete guide to trading oil markets

Looking ahead

18:00 Baker Hughes rig count

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels

- Place the trade.

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest Crude Oil articles

April 22, 2024 04:00 PM

April 19, 2024 03:35 AM

April 17, 2024 05:00 PM

April 17, 2024 03:02 AM