US futures

Dow futures +0.04% at 35417

S&P futures -0.15% at 4490

Nasdaq futures -0.25% at 15336

In Europe

FTSE -0.16% at 7130

Dax -0.5% at 15780

Euro Stoxx -0.43% at 4163

Learn more about trading indices

Risk off dominates

US stocks are set to open in a mixed fashion struggling to build on recent record highs on the back of weaker data and as investors wait anxiously for the Jackson Hole.

US GDP Q2 second reading was upwardly revised to 6.6% on an annual basis, this was up from 6.5% but still short of the 6.7% forecast. The US economy received a bigger than initially expected boost thanks to robust consumer spending as stimulus checks were hand out. A rapid vaccination drive also boosted travel and confidence. However, momentum looks to be slowing more recently as covid cases rise reflected in consumer confidence and retail sales last data week.

Meanwhile US jobless claims rose to 353k last week up from 348k slightly missing forecasts of 350k.

The numbers come ahead of the start of the Jackson Hole Symposium. To say that this is the most eagerly awaited event of the week or even the month would be a gross understatement. Federal Reserve Chair Jerome Powell’s hotly awaited keynote speech will take place tomorrow with investor’s ears pricked for any clues over when the central bank could start tapering its $120 billion per month bond buying programme.

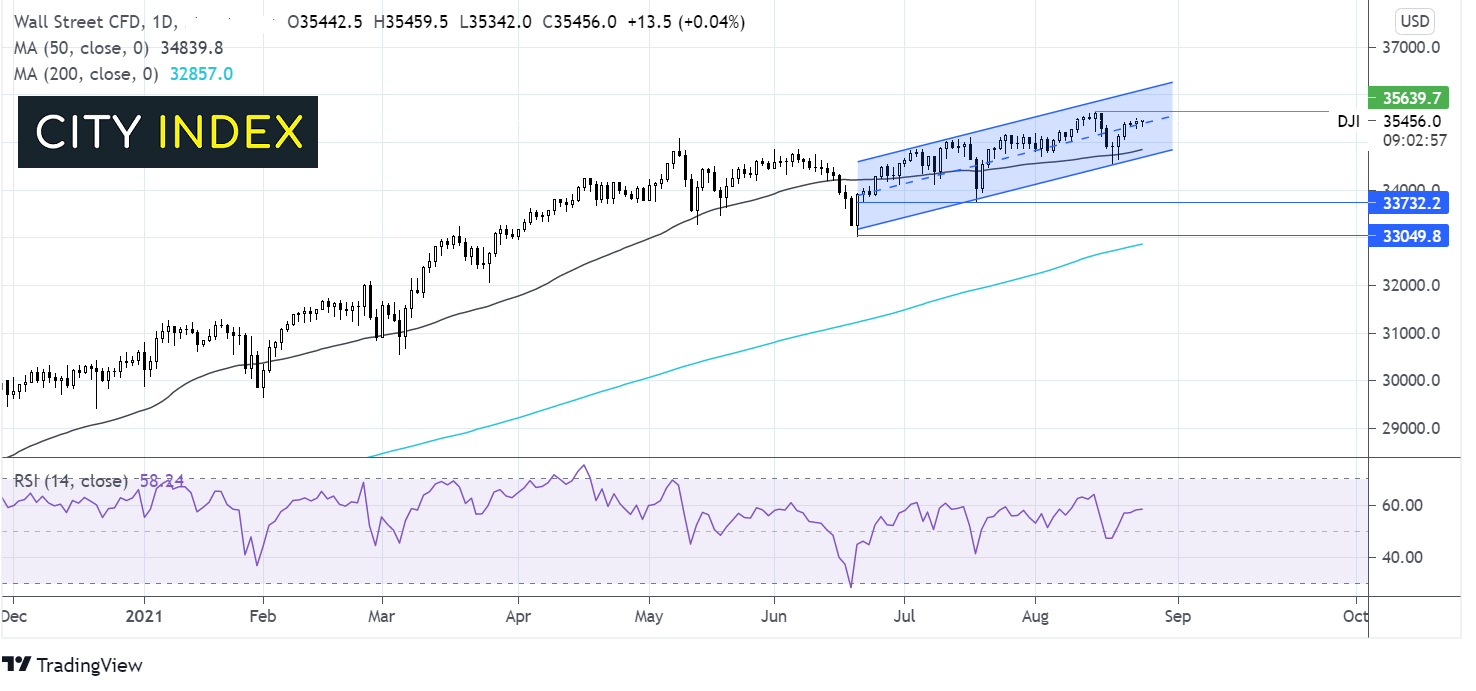

Where next for the Dow Jones?

The Dow Jones trades within an ascending channel dating back to mid-June guided higher along the mid line. The price is extending the rebound from the 50 day ma reached last week with the all time high of 35630 insight. A close below the 50 sma around 34800 and the lower band of the ascending channel could be significant, negating the near-term uptrend.

FX – USD rises after 3 days of losses

The US Dollar is holding steady following the weaker than forecast data and as investors look to the Jackson Hole Economic Forum for further clues.

EUR/USD is holding up despite weaker than forecast German GFK consumer sentiment data. Consumer morale fell a worse than expected -1.2 points in September, down from -0.4 and below the -0.8 forecast. Weak data comes following disappointing German IFO business sentiment and weaker than forecast German manufacturing PMI in Monday. Supply chain bottlenecks, chip shortages and rising covid cases mean the economic recovery in Germany is losing momentum.

GBP/USD -0.15% at 1.3742

EUR/USD -0.02% at 1.1774

Oil falls snapping 3 day winning run

Oil prices are moving lower as the three day rally comes to an end. Oil prices are falling for the first time this week amid renewed concerns over rising COVID cases and as Mexico restored some oil production.

Covid fears are dominating even though EIA data revealed that US crude inventories fell last week for a third straight week and fuel demand increased.

Its also worth considering that fuel demand could be peaking as the US summer driving season will start to wind down over the coming weeks.

US crude trades -0.9% at $67.67

Brent trades -0.8% at $70.82

Learn more about trading oil here.

The complete guide to trading oil markets

Looking ahead

15:00 Jackson Hole Symposium

16:00 ECB’s Schnabel

23:00 NZD Roy Morgan Consumer Confidence

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels

- Place the trade.

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM