US futures

Dow futures +0.23% at 35840

S&P futures +0.3% at 4583

Nasdaq futures +0.54% at 15600

In Europe

FTSE +0.65% at 7273

Dax +0.94% at 15760

Euro Stoxx +0.85% at 44225

Learn more about trading indices

Stocks look to earnings

US stocks are set to open on the front foot with the tech heavy Nasdaq leading the charge. Upbeat earnings expected to boost the mood, in addition to Tesla making the $1 trillion milestone.

Wall Street earnings are once again sufficiently strong to overshadow any concerns over inflation ahead of a slew of central bank meetings over the coming 10 days.

After gaining over 12% in the previous session on the back of a 100,000 EV order by Hertz, the EV maker was just 0.1% lower pre-market today. Facebook is also heading higher pre-market after not only reporting solid user growth but also a buyback promise of $50 billion more in stock. This sufficiently distracted from the fact that revenue growth at the social media giant had slowed to 35% year on year, down from 50% earlier in the year.

Big tech is likely to remain firmly in focus with earnings from Microsoft and Alphabet due after the close.

On the data front US consumer confidence could dampen upbeat spirits if the reading comes in lower than forecast. Consumer morale is expected to decline again in October which will mark the fourth straight month of deteriorating sentiment.

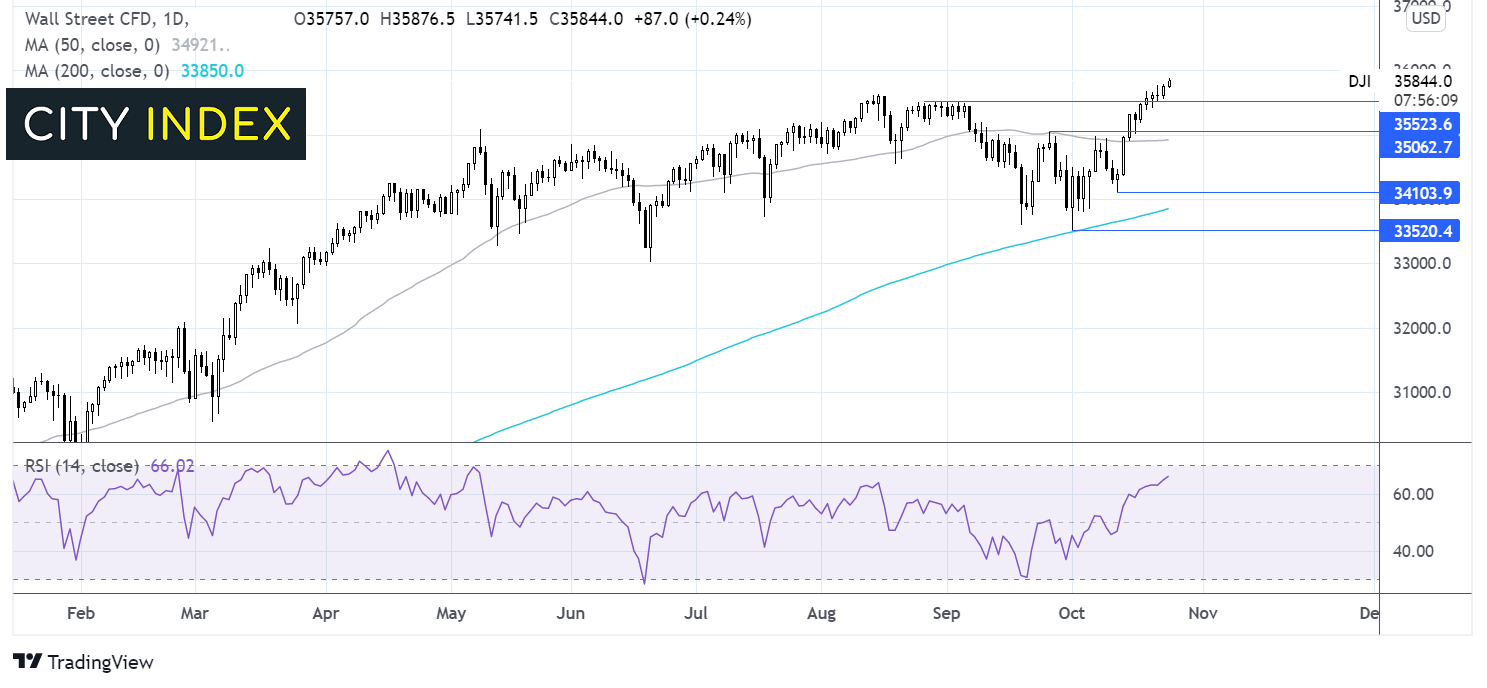

Where next for the Dow Jones Index?

After breaking out at the end of last week the Dow is set to climb higher. There are few signs on the chart that this move higher has run its path. Support can be seen at 35535 and 35000 – a move below here could negate the near term up trend. It would take a move below 34125 for sellers to gain momentum.

FX – USD pares gains GBP rallies

The US Dollar pared earlier gains as it traced US treasury yields lower. This could well be the calm before the storm as investors wait for central bank announcements from a slew of banks including the BoC, the BoJ and the ECB this week, followed by the RBA, the Fed and the BoE next week.

GBP/USD trades higher, hitting a 3 day peak above 1.38 following on from upbeat CBI retail sales distributive trends. The CBI report revealed that the sales index surged to 30, up from 11 in September and well ahead of the 13 expected. GBP jumped on the news.

GBP/USD +0.2% at 1.3793

EUR/USD +0.07% at 1.1616

Oil pares losses

After starting the session in the red, oil prices have pared earlier losses and continues to trade around multi year highs. Whilst there are some potential headwinds building the price remains under pinned by strong demand in the US, the world’s largest consumer and tight supply.

Iran and the West are entering a crucial stage in talks. However, we’ve been here before. Any agreement between Iran and the West which would see the sanctions removed on Iranian oil is unlikely to ne imminent.

API crude stock pile data is due to be released late today ahead of EIA data tomorrow.

WTI crude trades +0.18% at $83.60

Brent trades +0.12% at $85.31

Learn more about trading oil here.

Looking ahead

14:00 US New Home Sales

15:00 US Consumer Confidence

21:30 API Weekly Crude Stock Piles

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels

- Place the trade.

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM

Latest Indices articles

April 18, 2024 04:46 PM

April 17, 2024 11:00 AM

April 16, 2024 08:00 PM

April 16, 2024 04:54 PM