US open: Stocks rise as bond yields hit monthly low

US futures

Dow futures +0.02% at 34604

S&P futures +0.2% at 4236

Nasdaq futures +0.34% at 13856

In Europe

FTSE -0.4% at 7073

Dax -0.45% at 15582

Euro Stoxx +0.02% at 4096

Learn more about trading indices

Stocks rise, tech leads as bond yields fall

US stocks are set for another fairly subdued start as US treasury bond yields continue to fall even as inflationary pressures appear to be building. Either way inflation remains the key focus for the weary market ahead of tomorrow’s US CPI data.

Yesterday’s JOLTs job openings revealed 9.3 million openings, up by 1 million highlighting an inability of firms to fill roles. With over 8 million fewer workers in the workforce than pre-pandemic companies may well need to start hiking wages into order to attract workers, pointing building inflationary pressures.

Chines CPI rose 1.3% YoY, this was up from 0.9% in April, although missed forecasts of 1.6%. PPI, however, surged to a 13 year high of 9% YoY in May, well up from 6.6% in April and ahead of forecasts. These price increases could potentially trickle out across the globe.

Yet with US treasury yields at the lowest level in a month as inflation fears are calming in the market and bets of an earlier move by the Fed easing. High growth tech stocks which are most sensitive to interest rate expectations are set for a stronger start with the Nasdaq futures set to outperform US major indices.

Equities

So called meme stocks remain very much in focus with Clover Health the latest to become the retail traders’ favorite. The stock trades 22% pre-market after 86% gains yesterday.

GameStop is due to report after hours.

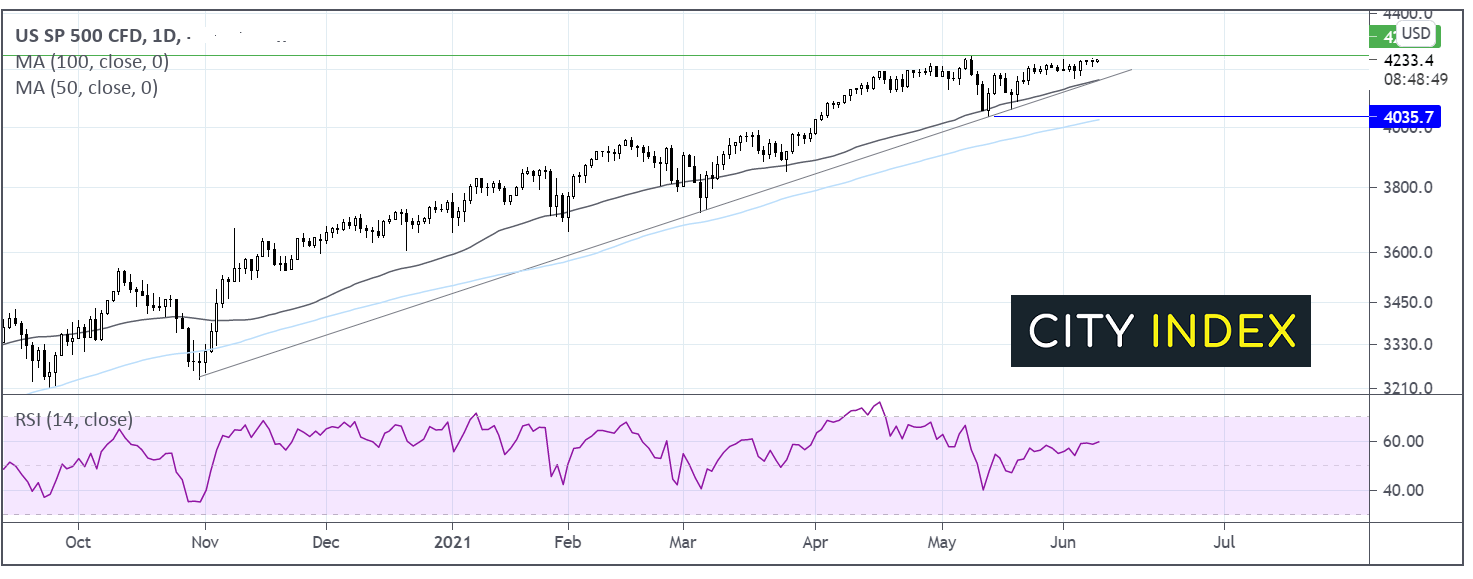

Where next for the S&P?

The S&P is edging higher as it trades under 15 points from its all time high. The move higher is slowing although there is little to suggest that it won’t break through 4245 to hit fresh all time highs. It would rake a move below 4155 the confluence of the 50 sma and the ascending trendline dating bavck to November to negate the near term uptrend. A break through here could see the price drop towards 4035 the May low and the 100 sma.

Source: StoneX, TradingView

FX – USD edges higher, EUR digests mixed bag of data

The US Dollar is edging lower, tracing treasury yields southwards as expectations of a move by the Fed eases, despite signs of inflationary pressures growing.

GBP/USD is advancing after BoE Chief Economist pointed towards tapering support. Haldane saw the UK economy firing on all cylinders, with price pressures building. His bold statement to reduce support comes as he is leaving the BoE shortly. Brexit concerns are acting as a weight on the currency amid worsening relations between Britain and the EU.

GBP/USD +0.15% at 1.4176

EUR/USD +0.18% at 1.2195

Oil rises, WTI breaches $70

Oil is extending gains from the previous session amid an improving demand outlook and as concerns over Iranian oil flooding back into the market ease. WTI crude oil pushed through $70 for the first time since 2018.

Rapid vaccine rollouts in the West and the easing of lockdown restrictions, combined rising optimism of a strong driving season in the US and Europe are boosting demand expectations. The EIA upwardly revised its oil demand outlook for the US to 1.49 million barrels per day, up from 1.39 million barrels. Adding to the upbeat mood API data revealed a draw in crude oil stockpiles of 2.1 million as expected.

Separately the US Secretary of State calmed fears of Iranian oil re-entering the market by saying that even if the nuclear deal was revived with Iran hundred’s of sanction would remain in place.

EIA crude stockpile data is due later.

US crude trades +0.4% at $70.25

Brent trades +0.5% at $72.45

Learn more about trading oil here.

The complete guide to trading oil markets

Looking ahead

15:00 BoC Rate Decision

15:30 EIA Crude Oil Inventories

Latest market news

Yesterday 08:33 AM

Latest Commodities articles

April 17, 2024 03:02 AM

April 15, 2024 12:48 AM

April 14, 2024 11:37 PM