US futures

Dow futures +0.24% at 34460

S&P futures +0.35% at 4370

Nasdaq futures +0.3% at 14798

In Europe

FTSE +0.03% at 7108

Dax -0.44% at 15291

Euro Stoxx -0.37% at 4066

Jobless claims unexpectedly rise

US stocks are heading for a stronger start as investors digest a mixed bag of data and await news from Washington over government funding.

On the data front, US GDP the final reading for Q2 was upwardly revised to 6.7% QoQ, up from 6.6% revealing that the economic rebound in the April – June period was stronger than expected.

However, US jobless claims unexpectedly rose again last week. 362K Americans filed for unemployment benefit, this was up from 351k the previous week and marked the third straight week of gains. The data comes following surprisingly weak US NFP last month. The Fed have said that they are watching the labour market recovery closely for clues for when to move on reining in support.

The weaker jobless claims appear to be unnerving the market pointing to potential weakness in the labour market recovery. It would take another weaker NFP for the Fed to consider delaying tapering bond purchases and after a few weeks of rising jobless claims, this could be a possibility.

Separately the Senate Majority leader Chuck Schumer said that lawmakers had reached an agreement to avoid a government shutdown, extending spending until December 3rd.

Fed Chair Powell is due to speak later.

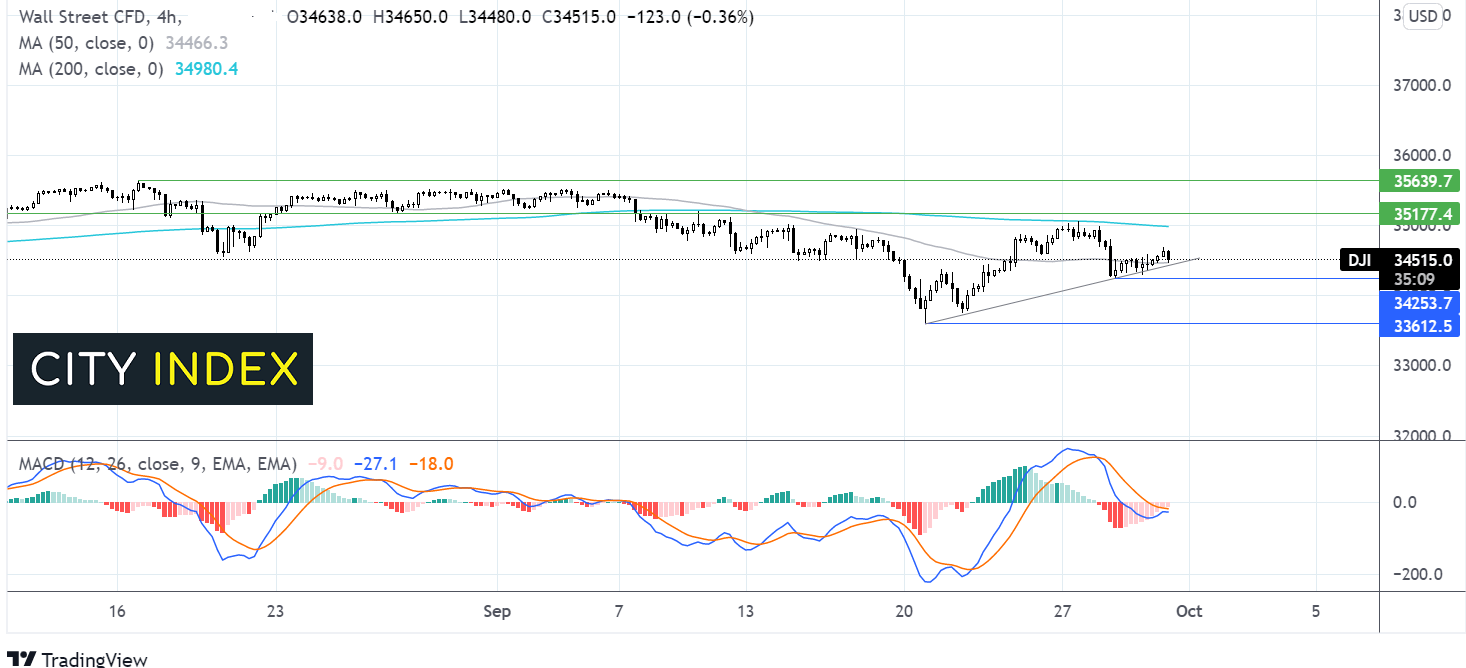

Where next for the Dow Jones?

The Dow Jones is extending is recovery from 33613 low on September 20. It trades above its ascending trendline and is retaking the 50 sma on the daily chart. The receding bearish bias on the MACD is keeping buyers optimistic of further upside. Any move higher would need to retake the 200 sma at 34980 and 35000 the weekly high in order to cement a bullish trend. On the downside a move below 34250 could see the sellers gain traction towards 33612.

FX – USD extends gains, German CPI keeps rising

The US Dollar is trading around its highest level in as year, underpinned by elevated US treasury yields and expectations that the Federal Reserve will start tapering bond purchases by the end of the year.

EURUSD trades at yearly lows on the back of stronger USD. German CPI rose by less than expected at 4.1%, but still up from 3.9% in August. The fact that inflation continue to rise will raise questions over how transitory it really, prompting a more hawkish response from the ECB.

GBP/USD +0.24% at 1.3485

EUR/USD -0.12% at 1.1583

Oil eases as stock piles rise

Oil prices are heading lower pulled lower by rising US crude inventories and a strong US Dollar. EIA data revealed that stockpiles increased by 4.6 million barrels in the week ending September 24th, this is the first rise in stock piles for almost two months.

Separately the US Dollar trades at an almost one year high which makes buying oil more expensive for holders of other currencies.

Losses have been capped by a more bullish outlook. Citigroup is forecasting a 1.5 million barrel per day deficit on average over the next 6 months, even with supply increases.

WTI crude trades -1.2% at $73.90

Brent trades -1.17% at $77.20

Learn more about trading oil here.

Looking ahead

15:00 Fed Chair Powell testifies

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels

- Place the trade.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Indices articles

Yesterday 03:00 PM

April 24, 2024 03:30 PM

April 18, 2024 04:46 PM