US futures

Dow futures -0.04% at 34112

S&P futures -0.1% at 4170

Nasdaq futures -0.24% at 13897

In Europe

FTSE +0.08% at 6907

Dax +0.6% at 15285

Euro Stoxx +0.76% at 4007

Learn more about trading indices

Jobless Claims unexpectedly drop

US stocks are set for a quiet open after a strong rally in the previous session. All three major indices finished the previous session solidly higher.

The improvement in the US labour market which was seen last week continued. 547K Americans made initial claims, down from 586k recorded last week and well below the forecast rise to 617k.

This is the lowest level for jobless claims since the pandemic and reveal that the recovery in the labour market remains on track.

Investors continue to wrestle over the vaccine led recovery and stronger earnings against rising covid cases particularly in India and Japan. Cases in India breached 300,000 a new grime global milestone.

Airlines will be in focus after results were not as bad as feared. Strength of demand for airline shares could provide clues as to the strength of the reopening trade.

Jobless claims are by far the most important US macro data to be released this week, a week that has been dominated by earnings.

US pledge on Earth Day

President Biden has pledged to cut the carbon dioxide emissions by 50% by the end of the decade compared to 2005 levels.

The pledge comes as the US looks to re-establish itself as a leader of the environmental agenda, after years of falling behind with Trump.

The new targets mean an accelerated move away from combustion engines in transportation. EV’s will be increasingly more in focus. Elsewhere, companies which are reducing their carbon foot print will be better positioned to respond to climate change risks and tightening regulation going forward.

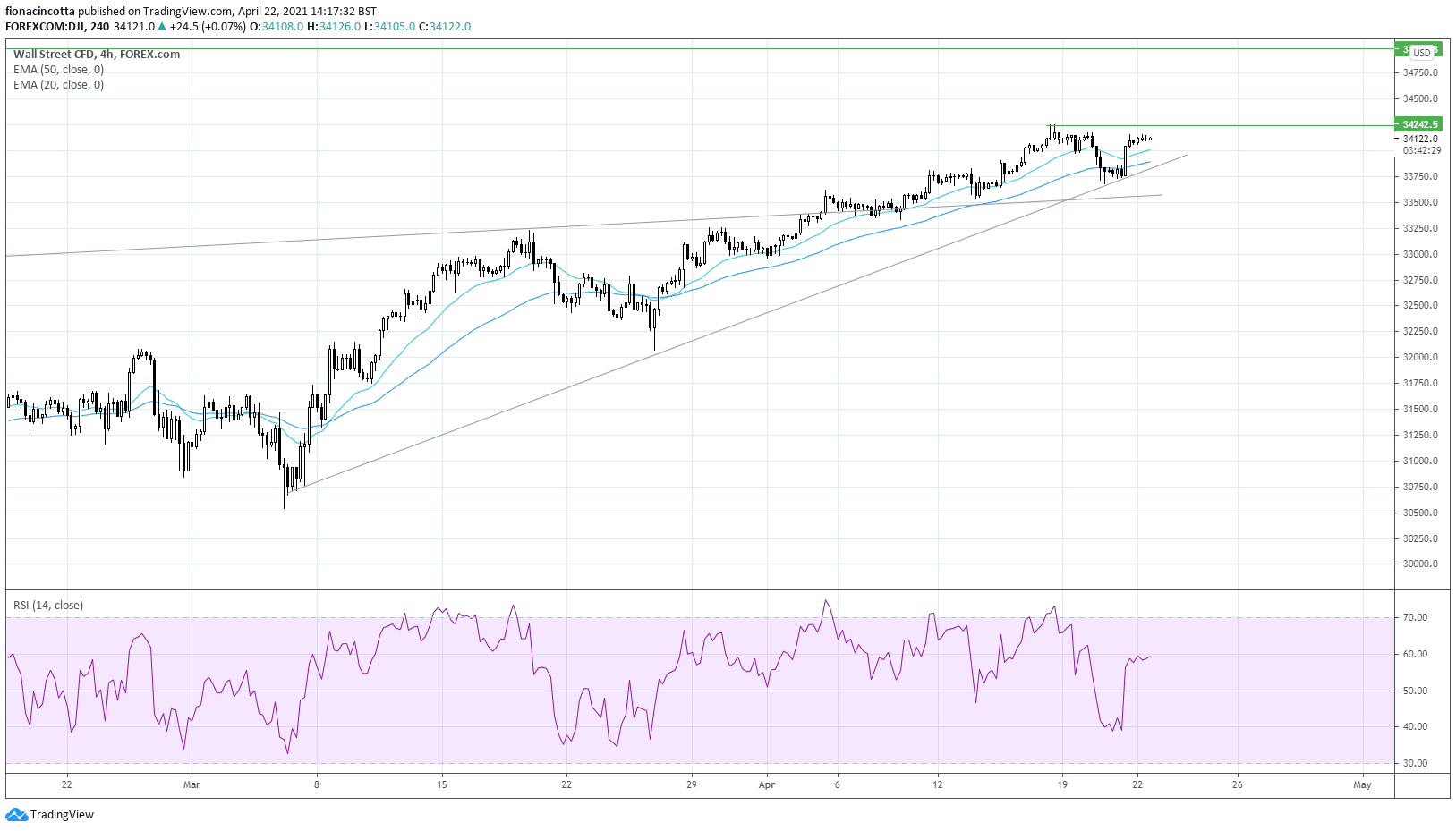

Where next for the Dow Jones?

The Dow Jones trades above its ascending trend line dating back to early March. It trades above its 20 & 50 EMA on the 4 hour chart and it hovering around its all time high.

The 20 EMA & 50 EMA are both pointing marginally higher as is the RSI suggesting that a move higher could be the path of least resistance.

Immediate resistance sits at 342248 the all time high, a move beyond here is needed to move towards 35000 round number.

Support can be seen at 34000 the 20 EMA and round number ahead of 33900 the 50 EMA. A break below 33800 the ascending trendline could sellers gain traction.

FX – ECB keeps policy unchanged, as expected

As expected, the ECB left rates and the PEPP unchanged as expected. With no new economic projections due until June, the ECB announcement has turned into a bit of a non-event.

Attention will now turn to the post meeting press conference with ECB President Christine Lagarde. With the vaccine rollout picking up and business sentiment improving we could hear a slightly more upbeat tone from the central bank President

GBP/USD -0.3% at 1.3885

EUR/USD +0.08% at 1.2043

Oil extends losses

Oil prices are falling for a third straight session amid an unexpected build in crude stockpiles and as covid cases soar in India and Japan.

EIA data revealed that US crude stockpiles unexpectedly rose in the week April 16, confirming API data from Tuesday.

At the same time covid cases are soaring in India and Japan, the world’s third and fourth largest consumers of oil respectively. More states in India are implementing lockdowns and Tokyo & Osaka are both on the brink of imposing curbs. As a result, the demand outlook for oil has softened hitting sentiment for oil.

US crude trades -0.5% at $61.00

Brent trades -0.5% at $64.43

Learn more about trading oil here.

The complete guide to trading oil markets

Looking ahead

15:00 Existing home sales

15:00 EUR consumer confidence

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

Latest Crude Oil articles

April 22, 2024 04:00 PM

April 19, 2024 03:35 AM

April 17, 2024 05:00 PM

April 17, 2024 03:02 AM