US futures

Dow futures +0.6% at 34825

S&P futures +0.6% at 4486

Nasdaq futures +0.54% at 15527

In Europe

FTSE +0.7% at 7082

Dax +1.08% at 15772

Euro Stoxx +0.9% at 4207

Learn more about trading indices

Rising oil prices & falling covid cases boost stocks

US stocks are set to open higher on Monday after booking heavy losses across the previous week. Rising energy prices, hopes of a watered down tax hike from the US Democrats and falling covid cases are lifting stocks overshadowing further crackdowns in China and the Democrats fleshing out their tax plans.

New daily covid cases have fallen from 157,000 at the end of August to 136,000, raisIng hopes that the peak of this latest wave could be passing. Whilst it is clearly to early to sing victory, after last week’s overdone selloff even the slightest bit of good news is seemingly lift stocks.

Separately President Biden’s $3.5 trillion tax and spending plans faces tough opposition. There is a good chance that the proposed tax hikes will get watered down in order to boost the prospects of the bill being passed.

There is no high impacting US economic data today. Investors will be looking ahead to tomorrow’s CPI print as inflation sits at 13 year highs. Expectations of the Fed moving to taper before the end of the year are rising, giving the reflation trade fresh legs.

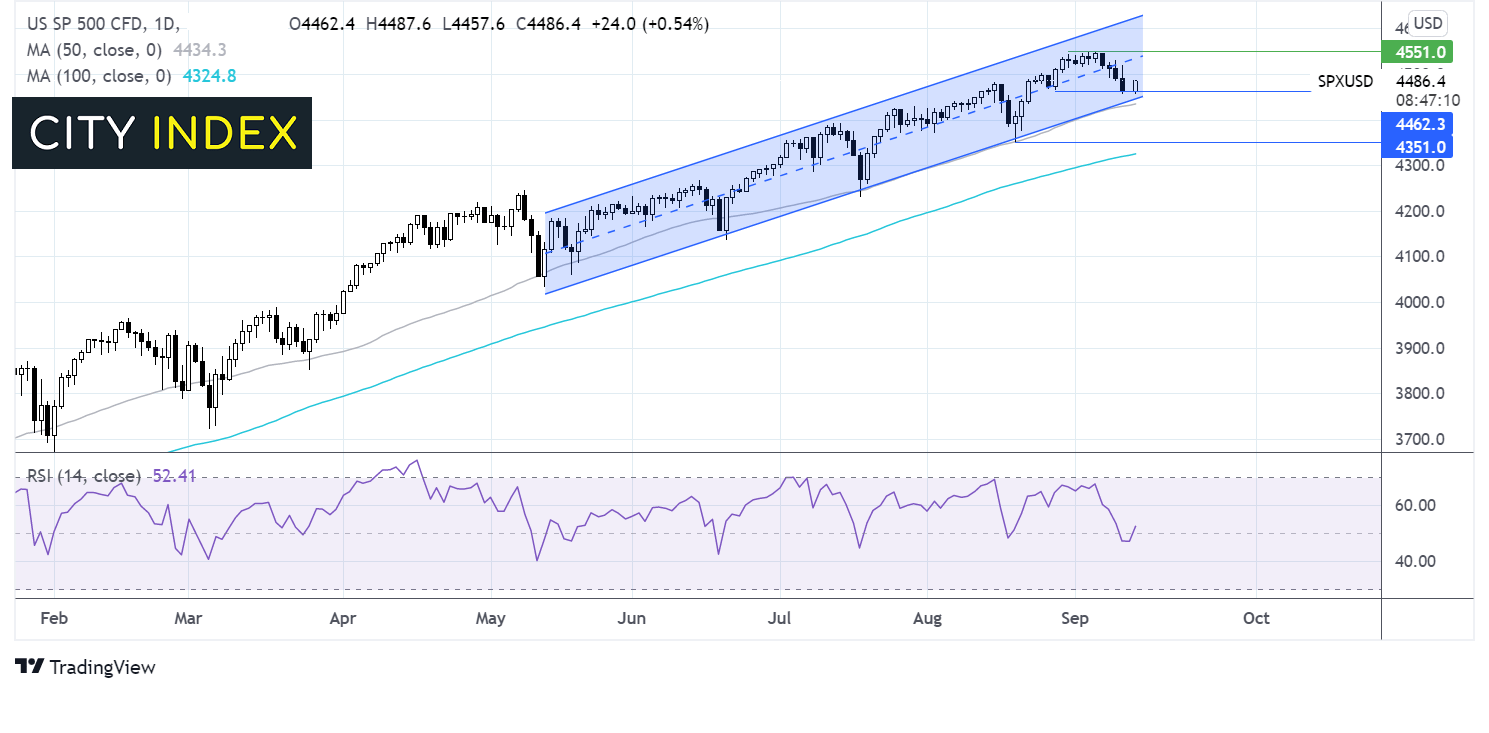

Where next for the S&P500?

The S&P is extending Friday’s rebound after falling for much of last week. The Index has once again found support around the 50 sma, a level which has proved to be a key support across the year and is now looking back towards 4500. It would take a move below the 50 sma at 4434 for the bears to change the bias.

FX – USD extends gains on hawkish Fed commentary

The US Dollar is advancing on the back of rising expectations that the Federal Reserve will taper its monthly bond purchases sooner rather than later. Philadelphia Fed President Patrick Harker became the latest to join a growing number of Fed officials who are in favour of the central bank tapering support before the end of the year. His comments come ahead of the Federal Reserve monetary policy meeting next week and CPI inflation data tomorrow.

EUR/USD is coming under pressure amid a quiet economic calendar and growing concerns over the upcoming German elections.

GBP/USD -0.05% at 1.3825

EUR/USD -0.31% at 1.1772

Oil rises on US output concerns

Oil prices are pushing higher as concerns over supply un the US continue to underpin the price. Hurricane Ida was almost two weeks ago and yet oil supply in the Gulf of Mexico is still only running at fraction of its usual level. 75% of output remains offline for now.

However, it is also worth noting that US production in the US is picking up with the Baker Hughes report on Friday revealing an increase in the number of rigs in operation. This means that US output is likely to rise in the coming weeks.

US crude trades +0.5% at $69.80

Brent trades +0.3% at $72.95

Learn more about trading oil here.

The complete guide to trading oil markets

Looking ahead

N/A

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels

- Place the trade.

Latest market news

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Yesterday 08:15 AM

Latest Crude Oil articles

April 22, 2024 04:00 PM

April 19, 2024 03:35 AM

April 17, 2024 05:00 PM

April 17, 2024 03:02 AM