US futures

Dow futures +0.66% at 34812

S&P futures +0.3% at 4550

Nasdaq futures -0.3% at 15668

In Europe

FTSE +1.2% at 7196

Dax +0.9% at 15260

Euro Stoxx +0.8% at 4110

Learn more about trading indices

Nasdaq underperforms

US stocks are set for a mixed start with the high tech Nasdaq under performing as treasury yields rise. Easing Omicron fears are making way for investors to position for a more hawkish Fed.

The markets are dialing back on the potential economic damage that Omicron could cause as initial reports suggest that the new COVID variant is less severe. US medical advisor Anthony Fauci said that the early signs suggest that Omicron doesn’t have a great degree of severity. His comments came as Omicron spread to around one-third of US states.

There is no high impacting economic data due today. Looking out across the week US CPI inflation data on Friday is expected to be the main focus. Particularly after the Fed’s removal of the word “transitory” for inflation last week.

In corporate news:

Kohls trades up 4% pre-market after reports that an activist investor is prompting the department store to sell or separate from its faster growing e-commerce business.

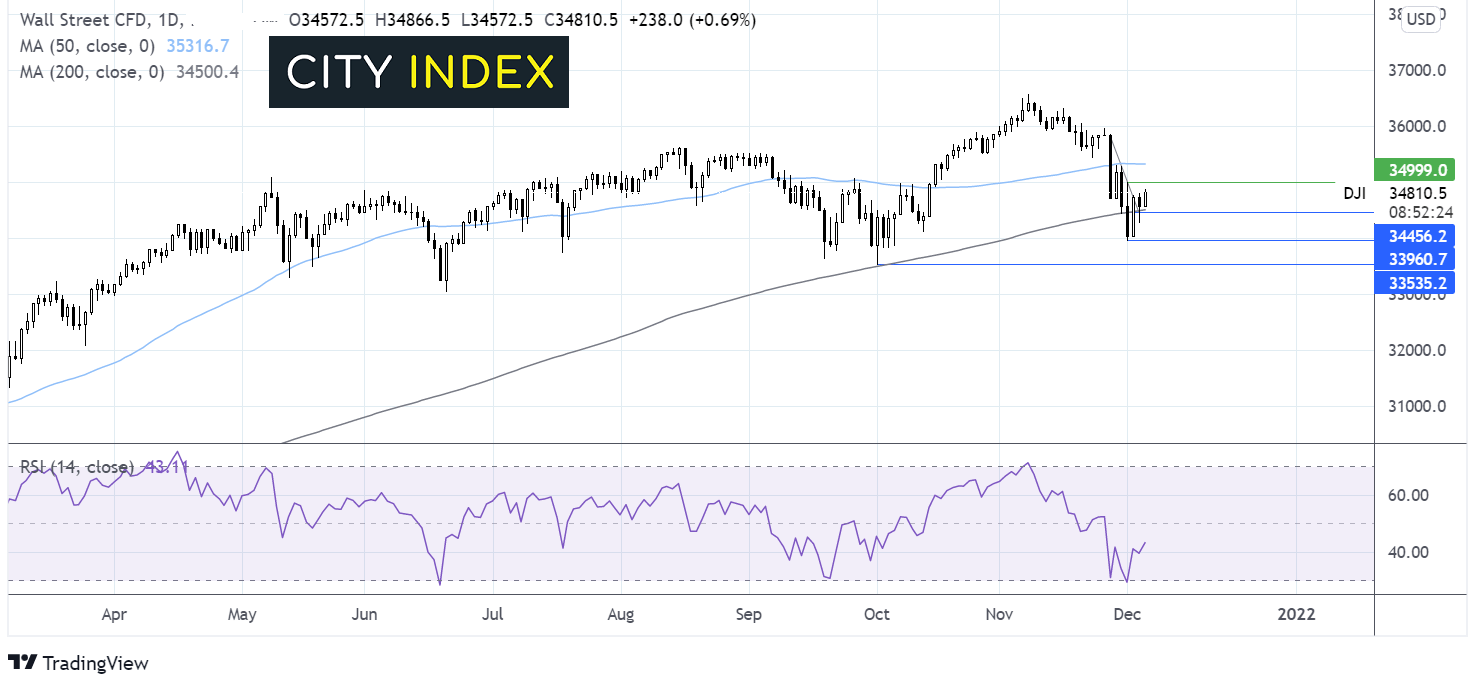

Where next for the Dow Jones?

The Dow Jones is extending its rebound from 3395 reached last week, re-taking the 200 sma at 34450 whilst heading towards 35000 key psychological level. However, the RSI remain firmly below 50. Buyers will want to see a move over 35000 to expose the 50 sma at 35300 and to signal tht the near term bear trend is over. Meanwhile a break below 34500 the 200 sma and 33995 would be significant for sellers.

FX – USD rises with treasury yields, EUR struggles below 1.13

The USD is heading higher, tracing treasury yields northwards after reassuring news surrounding Omicron boosted bets that the Fed will be able to tighten monetary policy at a faster pace. Riskier currencies such as the AUD is on the rise, whilst safe havens such as the Japanese yen are coming under pressure.

EUR/USD trades low after German factory orders collapsed in October. Factory orders slumped -6.9%, in October, following a 1.3% increase in September. The sector is being hit by supply chain bottlenecks, surging prices and more recently rising COVID cases. This could slow economic growth in the Eurozone’s largest economy, which is still below its pre-pandemic level.

GBP/USD +0.31% at 1.3271

EUR/USD -0.14% at 1.1295

Oil jumps 3%

Oil prices are on the rise, clawing back losses from last week. Optimism that the new COVID strain Omicron, may not be as severe and could have a less damaging impact on the economic is helping boost the oil demand outlook.

Also boosting the price of oil is news that Saudi Arabia, the world’s largest oil exporter, increased its selling price by 80 cents per barrel compared to the previous month.

Finally, in-direct talks between the US and Iran over the nuclear agreement have stalled, again, reducing the prospect of restrictions on Iranian oil being lifted.

WTI crude trades +3% at $68.30

Brent trades +2.85% at $71.90

Learn more about trading oil here.

Looking ahead

N/A

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels

- Place the trade.

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM

Latest USD articles

Yesterday 01:23 PM

April 18, 2024 11:27 PM

April 18, 2024 01:06 PM

April 18, 2024 06:20 AM