US futures

Dow futures -0.46% at 34190

S&P futures -0.45% at 4337

Nasdaq futures -0.55% at 14693

In Europe

FTSE +0.07% at 7047

Dax -0.5% at 15153

Euro Stoxx -0.31% at 4020

Learn more about trading indicesStagflation fears persist

US stocks are set to start the week in the red as the post pandemic recovery appears to be stumbling. Supply shortages and a worsening energy crunch mean prices are rising and elevated inflation may not be as transitory as the Fed initially thought. Stagflation fears come at a time when the US central bank is expected to start tapering bond purchases in the coming months. Questions surrounding the US debt ceiling and spending bills are adding to are clouding sentiment further.

The S&P 500 shed almost 2% last week as stagflation fears stemming from higher energy prices, supply chain disruptions and labour shortages hit risk sentiment.

In corporate news, Tesla is driving higher pre-market on blowout deliveries. The firm defies the chip shortage hitting the rest of the sector and reported a record 73% jump in deliveries in the third quarter.

Looking ahead US factory orders will be in focus today, in addition to Fed speakers across the session. However, Friday’s non-farm payroll report is likely to be the data which cements the Fed’s next move. Expectations are for almost 500,000 new jobs to have been added in September.

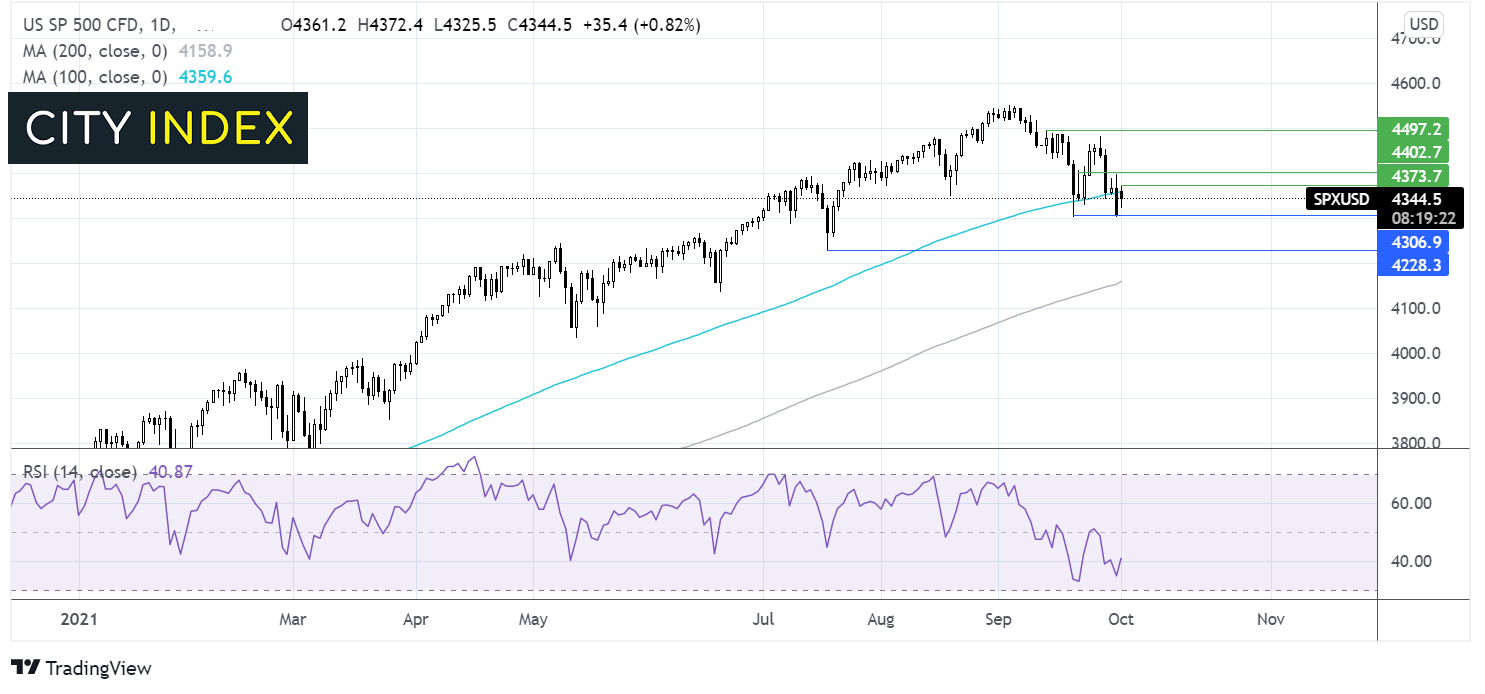

Where next for the S&P500?

The S&P trades below the 100 sma but the sell off has so far stopped short of support at 4300 last week’s low. It would take a break below this level for the sellers to gain traction and target 4220. It would take a move over 4272 today’s high to negate the near term bearish view and to bring 4400 back into play.

FX – USD eases, GBP extends recovery

The US Dollar is on the backfoot for a third consecutive session, falling below the key 94.00. The US Dollar is falling despite the risk off mood in the market and expectations that he Fed could start tapering later this year. US factory orders are in focus today. However, the focus across the week IS US non-farm payrolls on Friday.

GBP/USD is extending its recovery into a third straight session, outperforming peers. Fears over stagflation which sent sterling tumbling early last week have eased. GBP/USD retaking 1.36, shrugging off the latest Brexit developments which suggest that the UK’s chief Brexit negotiator could adopt a tougher stance on the Northern Ireland protocol.

GBP/USD +0.4% at 1.36

EUR/USD +0.3% at 1.1630

GBP/USD +0.4% at 1.36

EUR/USD +0.3% at 1.1630

Oil looks to OPEC+meeting

Oil prices are holding steady as investors await news from the latest OPEC+ supply policy meeting. The meeting is likely to see members decide whether to increase output further amid supply side shocks and as reopening demand remains strong. The meeting comes after the group agreed in July to raise production by 400,000 barrels per day from November.

So far at least three sources have said that the group are unlikely to raise output further given uncertainty surrounding a fourth wave of covid. Demand is expected to outstrip supply for the coming 6 months.

WTI crude trades +0.34% at $75.81

Brent trades +0.27% at $79.33

Learn more about trading oil here.

Looking ahead

15:00 US factory orders

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels

- Place the trade.

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM

Latest Indices articles

April 18, 2024 04:46 PM

April 17, 2024 11:00 AM

April 16, 2024 08:00 PM

April 16, 2024 04:54 PM