US futures

Dow futures +0.24% at 36123

S&P futures +0.17% at 4656

Nasdaq futures +0.17% at 16059

In Europe

FTSE -0.50% at 7350

Dax +0.11% at 16104

Euro Stoxx +0.12% at 4362

Learn more about trading indices

US sentiment & jobs data in focus

US stocks are pointing to a higher start after a mixed close in the previous session. Even so, indices on Wall Street are still on track for over 1% losses after 5 weeks of gains.

Concerns over surging inflation have hurt investor sentiment this week, after CPI crossed the 6% threshold rising to the highest level in 30 years.

Attention will now turn to consumer sentiment data. The Michigan consumer sentiment report has fallen for the past three months as higher prices have weighed on morale. However, expectations are for an improvement in sentiment.

JOLTS job openings are also expected to be closely monitored given the emphasis that the Fed is putting on the labour market recovery for clues of when to move on lifting interest rates. Expectations are for around 10 million vaccines in September, once again raising more questions than answers as just 312k payrolls were added the same month.

In corporate news Johnson & Johnson has announced plans to split into two companies, dividing its consumer healthcare business from its pharmaceutical business.

Rivian is likely to remain in focus after its extremely successful IPO.

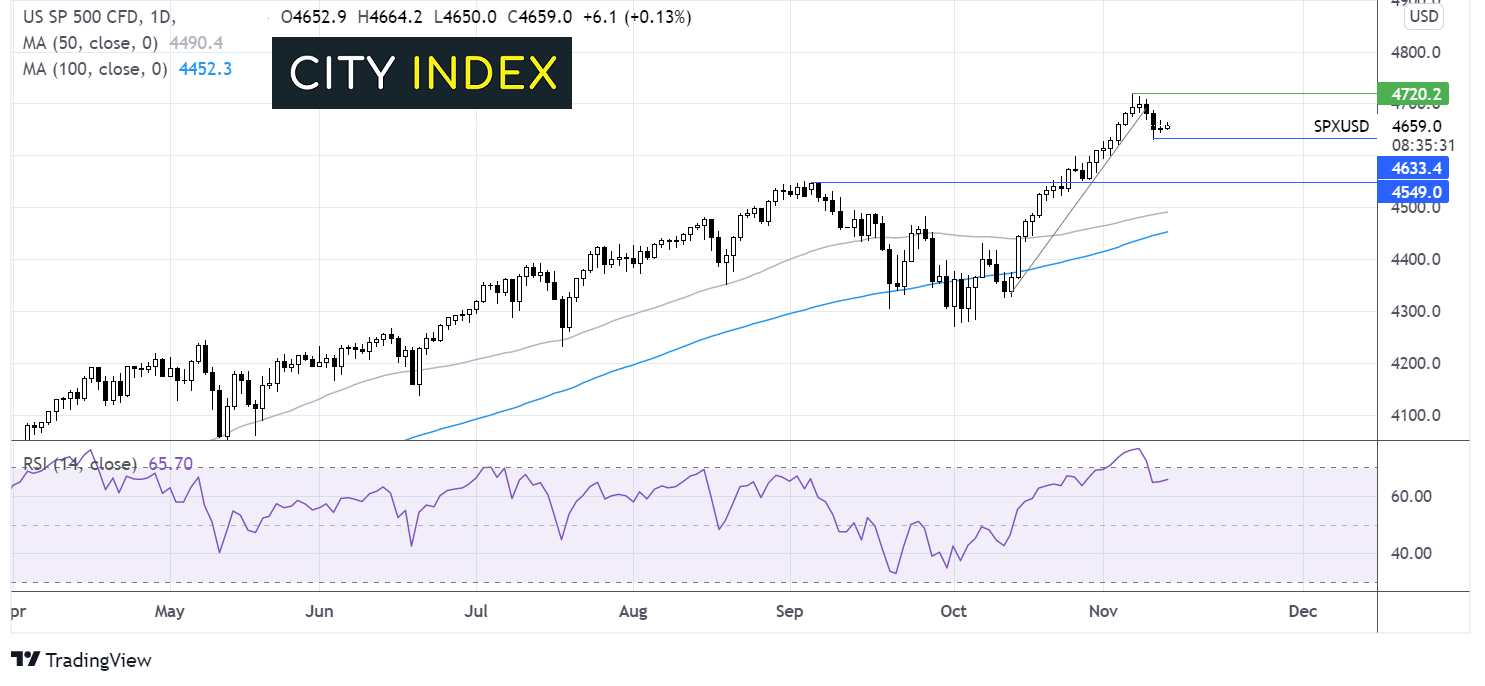

Where next for S&P 500?

The S&P has been extending a rebound from 4270 struck on October 1, hitting resistance at 4720 before easing lower and bringing the RSI out of overbought territory. The price is consolidating after a strong rally. A move below 4630 the weekly low is needed to open the door to 4550. Only below here is the uptrend negated. Meanwhile a move over 4720 would lead to fresh all time highs.

FX – USD extends gains, EUR steadies

US Dollar is edging lower but still remains near 16-month highs as investors bet that the Fed will be forced to move earlier to raise interest rates. Data later today could drive the greenback higher.

EUR/USD has stabilized around 1.1450 following the release of industrial production data. Factory output dipped by less than analysts had forecast in September, falling by -0.2% MoM whilst rising 5.2% year on year. Estimates had been for a 0.5% decline & 4.1% increase annually.

GBP/USD +0.16% at 1.3394

EUR/USD -0.01% at 1.1447

Oil set for weekly decline

Oil prices are heading lower and are set for a weekly decline, the third straight weekly decline as headwinds build. First, a stronger USD has knocked the wind out of oil’s sales following the recent jump in inflation. Furthermore, concerns that the Biden administration could release strategic reserves is adding pressure to oil prices. Finally, OPEC downwardly revised its Q3 demand outlook for oil. The oil cartel fears that a supply glut could be on the cards next year.

OPEC+ agreed to stick to the 400,000 barrel a day increase in output and has defied calls from leaders to hike output more.

WTI crude trades -0.8% at $79.50

Brent trades -0.7% at $81.50

Learn more about trading oil here.

Looking ahead

14:00 BoE Haskel

15:00 Michigan Consumer Sentiment

15:00 JOLTS Job Openings

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels

- Place the trade.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Latest Indices articles

Yesterday 03:00 PM

April 24, 2024 03:30 PM

April 18, 2024 04:46 PM