US futures

Dow futures -0.23% at 35170

S&P futures -0.51% at 4461

Nasdaq futures -0.8% at 14730

In Europe

FTSE -1.5% at 7482

Dax -2.23% at 15540

Euro Stoxx -2.0% at 4210

Learn more about trading indices

Netflix drops -20% pre-market

US stocks are set to fall again on the open with the tech heavy Nasdaq once again taking the hardest hit after a disappointing outlook from Netflix.

The streaming giant trades around 20% lower pre-market despite beating on top and bottom lines in Q4. Subscriber numbers were a touch under forecasts at 8.3 million but were still a good showing. The problem lay in the guidance for just 2.5 million new subscribers in Q1 2022.

The selloff has spread across the industry with the likes of Disney, Viacom and Roku, which have all invested heavily in steaming.

Peloton, another stock which outperformed in the pandemic fell over 23% yesterday on reports that it is cutting production of its bikes and treadmills on reduced demand.

The start to earnings season, for tech stocks has not been what tech bulls were looking for. Given the backdrop of higher interest rates across 2022, which is bad news for high growth stocks investors are looking to tech earning to provide a reason to back into tech. Netflix hasn’t provided that so far.

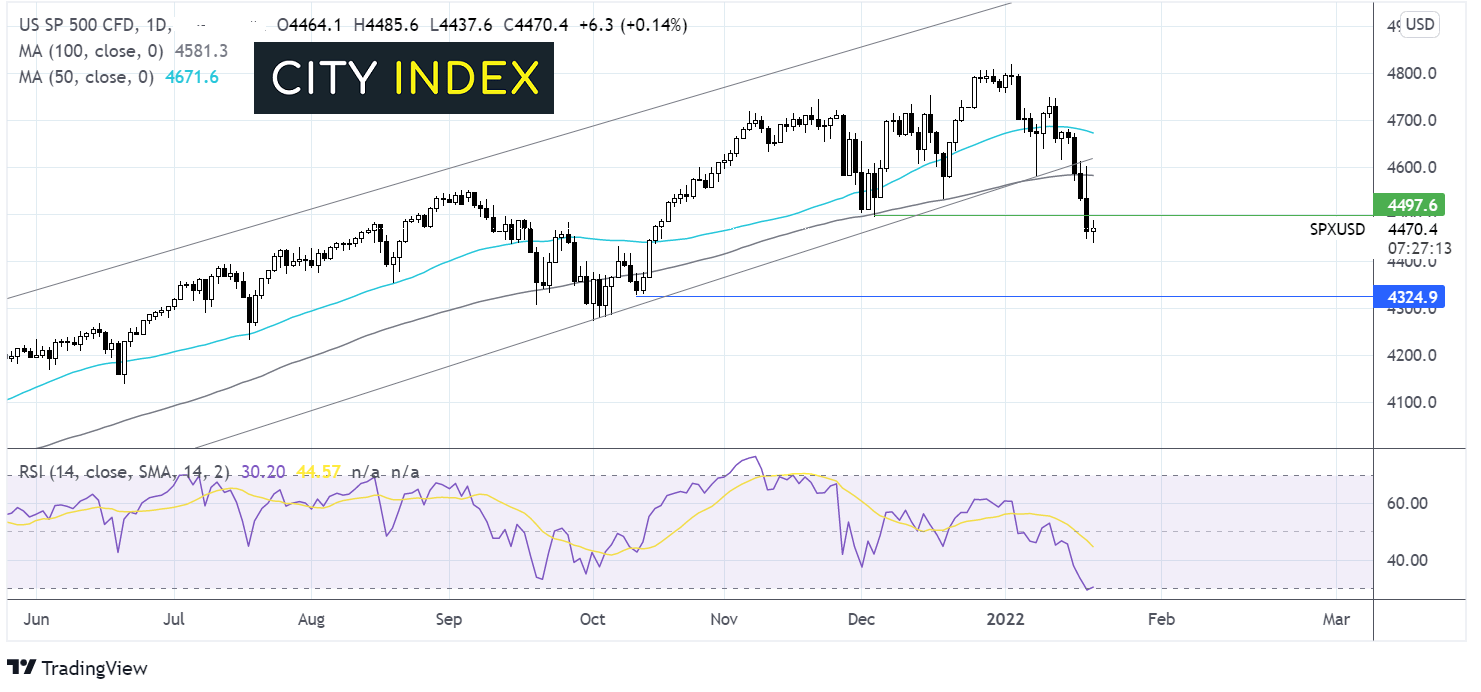

Where next for the S&P?

The S&P500 rallied higher, running into resistance at 4817 all time high. The price rebounded lower falling below the 100 & 50 sma and falling out of its multi-month ascending channel. The RSI has tipped into oversold territory so some consolidation or a move higher could be on the cards before further declines. Buyers will look for a move back over 4585 to negate the near term down trend whilst a move over 4670 could see buyers gain traction. Sellers could look to target 4325 October 12 low.

FX markets USD falls, GBP falls on dismal retail sales

The USD is edging a few points lower tracing bonds yields southwards. The risk off mood is driving demand for bonds.

GBP/USD trades under pressure after disappointing UK retail sales which fell -3.7% MoM in December as Omicron cases surged.

GBP/USD -0.19% at 1.3573

EUR/USD +0.33% at 1.1350

Oil eases from 7 year high, as oil inventories build

Oil prices are have fallen over 3% from the 7 year high reach earlier in the week. Even so, oil is still set to book a very mild weekly gain, markiNg a 5th straight week of gains.

Oil prices have run up 10% so far in 2022 on geopolitical and supply concerns. However, an unexpected increase in crude oil stockpiles sparked a bout of profit taking, sending oil sharply lower.

Crude oil inventories rose 515k. Meanwhile gasoline inventories jumped sharply higher.

WTI crude trades -1.4% at $84.76

Brent trades -1.44% at $86.90

Learn more about trading oil here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels

- Place the trade.

Latest market news

Today 08:15 AM

Latest USD articles

Yesterday 11:09 PM

Yesterday 11:01 PM

Yesterday 01:15 PM