US futures

Dow futures +0.25% at 34654

S&P futures +0.25% at 4203

Nasdaq futures +0.1% at 13550

In Europe

FTSE -0.45% at 7040

Dax -0.16% at 15630

Euro Stoxx -0.1% at 4075

Learn more about trading indices

Stocks rise on weak NFP report

US futures are pushing higher rebounding from earlier weakness after a mixed non farm payroll report. The closely watch US jobs report revealed that 559k new jobs were created in May, a rise fro April but this was short of the 650k that analysts had penciled in. This is the second straight month that the headline NFP report missed expectations as companies faced difficulties hiring.

Either childcare challenges as most school districts have not returned to full time in person learning or a lack of motivation thanks to the stimulus checks have meant filling vacancies is proving more challenging than usual for companies. Whilst this is driving up average hourly wages, the market it more focused on the fact that the headline NFP wasn’t a blowout number.

The data has helped calm those fears that dominated yesterday that the Fed could start to taper support sooner. The tech heavy Nasdaq which was hardest hit on Thursday is outperforming its peers today.

Investors don’t consider that NFP could also push the Fed to taper support more quickly than the market had expected. As a result, the US Dollar is declining whilst stocks are heading northwards.

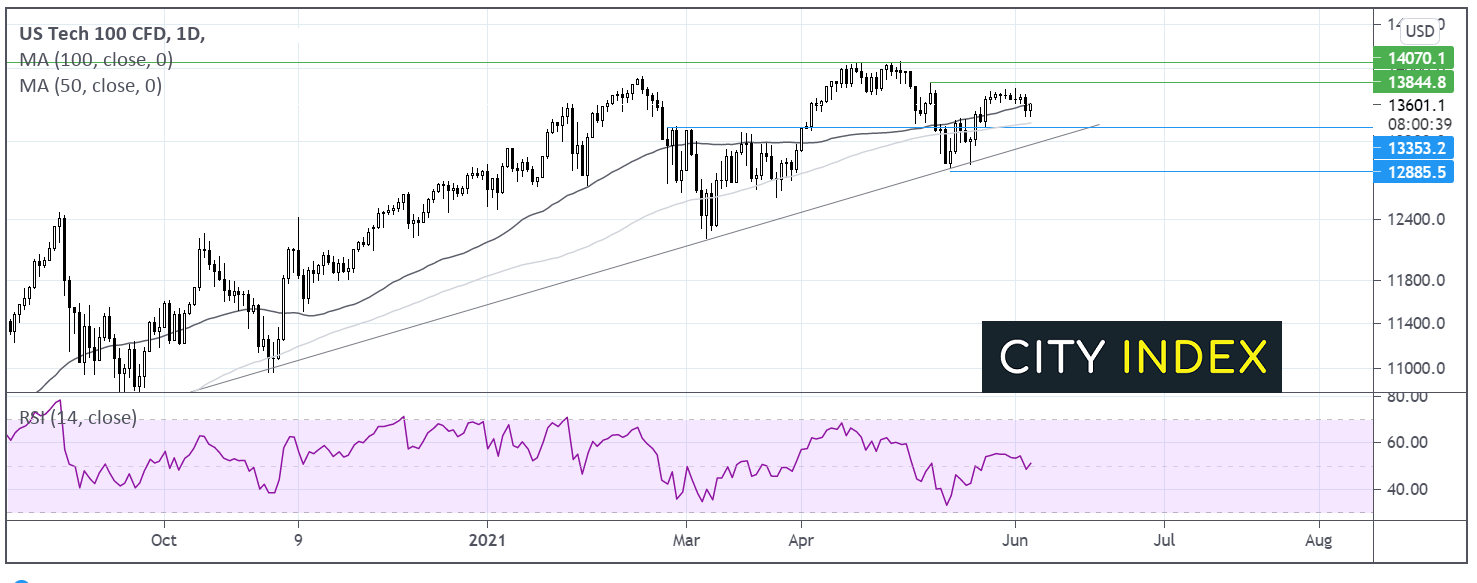

Where next for the Nasdaq?

Despite yesterday’s 1% decline the Nasdaq remains above its multi- month ascending trend line. It trades above its 100 day ma but below its 50 ma. The RSI is neutral at 50. The Nasdaq looks relatively range bound for now. It would take a move below 13400 the 100 sma and horizontal support for the sellers to gain traction. Buyers could be looking for a move above 13840 to confirm a bullish outlook.

Equities

The so-called meme stocks are likely to remain volatile again on Friday with AMC Entertainment seen opening lower after the cinema chain raised funds late on Thursday and closed 18% lower. The company has still doubled in value this week and jumped 450% this month as the new darling of retail of retail investors.

Docusign trades 5% high pre-market after beating in Q1 earnings.

Lululemon Athletica trades +0.9% pre-market after reporting an 88% jump in Q1 sales.

FX – USD drops, EUR sees disappointing retail sales

The US Dollar was trading on the front foot ahead of the ADP payroll release and extended those gains following the data.

EUR/USD is trading lower after Eurozone retail sales disappointed. Retail sales fell by -3.1% MoM in April, more than the -1.2% decline expected. This comes after a 3.3% MoM increase in March. Parts of the Euro area lockdown in April as the third wave of covid hit the continent.

GBP/USD +0.14% at 1.4125

EUR/USD -0.11% at 1.2114

Oil set for strong weekly gains

Oil prices are pushing higher on Friday and are looking to book gains of over 4.5% across the week driven by a strong demand outlook. Demand is expected to continue rising in the US, China and Europe outstripping supply in the second part of the year and overshadowing weakness in Asia.

EIA inventory data revealed a bigger than anticipated draw in crude inventory of 5 million barrels versus 2.4m draw forecast.

Attention will turn towards the Baker Hughes rig count to see whether crude oil trading at its highest level since October 2018 is attracting more rigs to reopen.

US crude trades +0.22% at $68.88

Brent trades +0.12% at $71.32

Learn more about trading oil here.

The complete guide to trading oil markets

Looking ahead

15:00 US Factory orders

18:00 Baker Hughes rig count

Latest market news

Yesterday 10:40 PM

Yesterday 04:00 PM

Latest Crude Oil articles

Yesterday 04:00 PM

April 19, 2024 03:35 AM

April 17, 2024 05:00 PM

April 17, 2024 03:02 AM