US futures

Dow futures +0.4% at 34340

S&P futures +0.15% at 4273

Nasdaq futures +0.16% at 14387

In Europe

FTSE +0.3% at 7134

Dax -0.04% at 15580

Euro Stoxx -0.1% at 4115

Learn more about trading indices

Fresh record highs?

Wall Street is pointing to a stronger open, with fresh all time highs in sight following Biden’s $600 infrastructure deal and weaker than forecast PCE data.

PCE – the Fed’s preferred gauge of inflation rose in May to 3.9% YoY, up from 3.6% in April. However, this was less than the 4% forecast. On a monthly basis, PCE rose 0.5%, down from the 0.7% forecast and below the 0.6% expected.

The weaker than forecast data is being cheered by investors as it supports the Fed’s belief that the spike in inflation is transitory. The data isn’t as bad as some were fearing in light of the Fed’s hawkish shift. Fed Powel’s prediction that the Fed is in no rush to tighten policy is gaining conviction.

The softer data comes following a string oof marginally weaker numbers this week from the US economy.

Biden’s infrastructure deal

Biden’s $600 billion bipartisan infrastructure deal which paves the way for further investment into bridges, roads and broadband helped lift stocks to a record high on Thursday with the upbeat mood carrying through until today.

The deal is slightly smaller than initial expectations which could have helped tame concerns over the economy running too hot.

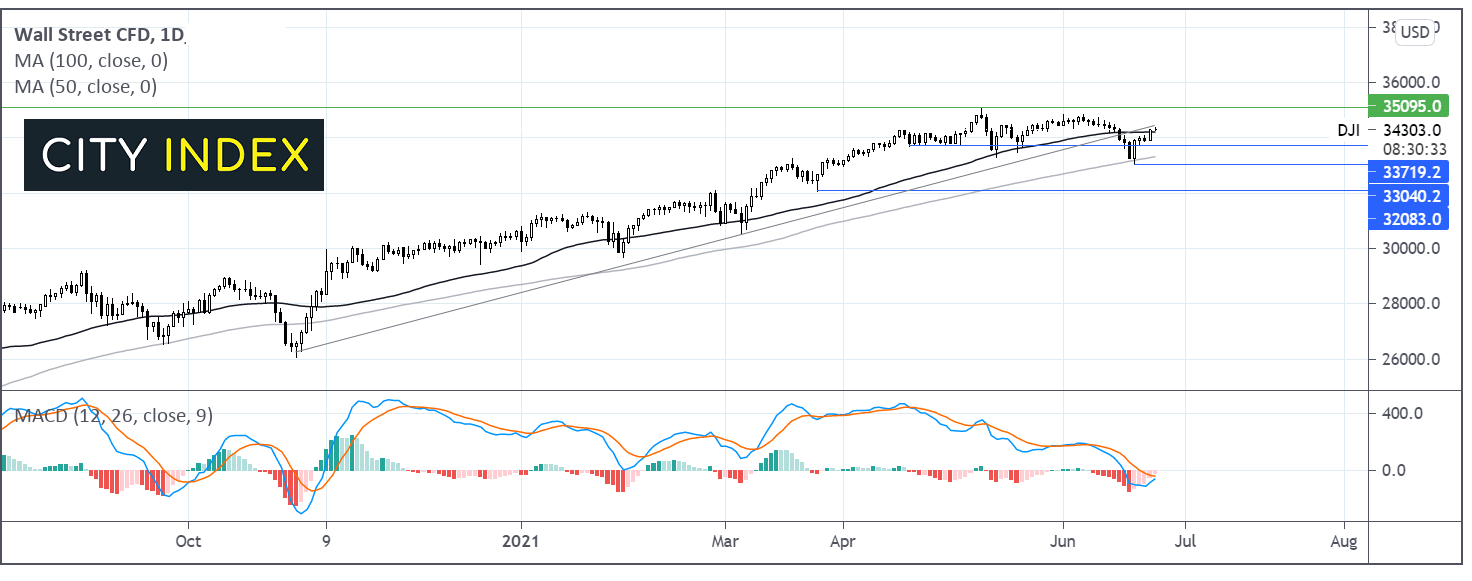

Where next for the Dow Jones?

The Dow Jones is attempting to break back above the ascending trendline that it breached last week. The price is encountering strong resistance at 34250/300 the 50 day ma and the ascending trendline support turned resistance. A move back over this level could see a fresh attach on the all time high at 35000. A receding bearish bias on the MACD supports further upside. A move below 33700 could negate the near term bullish bias. A move below 33000 could see the sellers gains traction.

FX – USD slips, EUR rises on strong German data

The US Dollar is edging and looks to end the week with mild losses snapping 4 straight weeks of gains.

EUR/USD is pushing higher following upbeat German GFK data which came in at -3 for July, up from -7 in June. Consumer confidence is set to rise as covid cases fall and the economy reopens. The data comes following strong German business sentiment data in the previous session and upbeat PMI data earlier in the week.

GBP/USD -0.17% at 1.3900

EUR/USD +0.11% at 1.1940

Oil steadies as OPEC+ meeting comes into focus

Oil prices are edging marginally lower after both benchmarks settled at a fresh two year high in the previous session. Even so, oil is set to gain over 2% this week in its fifth consecutive week of gains. Demand has clearly been outstripping supply as economies reopen, fuel demand surges and inventories are drained.

Attention will now be turning towards the OPEC+ meeting next week. There is a growing expectation that OPEC will look to gradually ramp up production across the second half of the year in order to meet soaring demand.

Baker Hughes rig count is due later.

US crude trades -0.25% at $73.11

Brent trades -0.14% at $74.75

Learn more about trading oil here.

The complete guide to trading oil markets

Looking ahead

15:00 US Michigan Consumer Confidence

18:00 Fed Rosengren speaks

18:00 Baker Hughes Oil Rig Count

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels

- Place the trade.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Latest Crude Oil articles

April 22, 2024 04:00 PM

April 19, 2024 03:35 AM

April 17, 2024 05:00 PM

April 17, 2024 03:02 AM