US futures

Dow futures +0.01% at 33815

S&P futures +0.2% at 4143

Nasdaq futures +0.24% at 13797

In Europe

FTSE -0.5% at 6900

Dax -0.6% at 15218

Euro Stoxx -0.5% at 3994

Learn more about trading indices

US stocks point mildly higher as tax nerves ease

US stocks are seen edging higher after a steep selloff in the previous session, with investors still nervous of a steep tax hike.

All three major indices ended Thursday almost 1% lower on reports that President Biden is set to propose a hike in capital gains tax to 0.4% for those earning over $1 million, almost double what it is now.

The markets feared that wealthy Americans could sell their stocks cashing in order to avoid a huge tax bill.

However, today nerves have calmed as they proposal could face significant challenges and plenty of opposition.

Earnings season continues with companies mainly managing to beat forecasts. Today sees numbers from Schlumberger, Kimberly-Klark and Intel.

On the data from PMI figures are due from both the manufacturing and the service sector. Both are expected to show a continuation of the recovery in both sectors. Similar figures from Europe were must stronger than forecast.

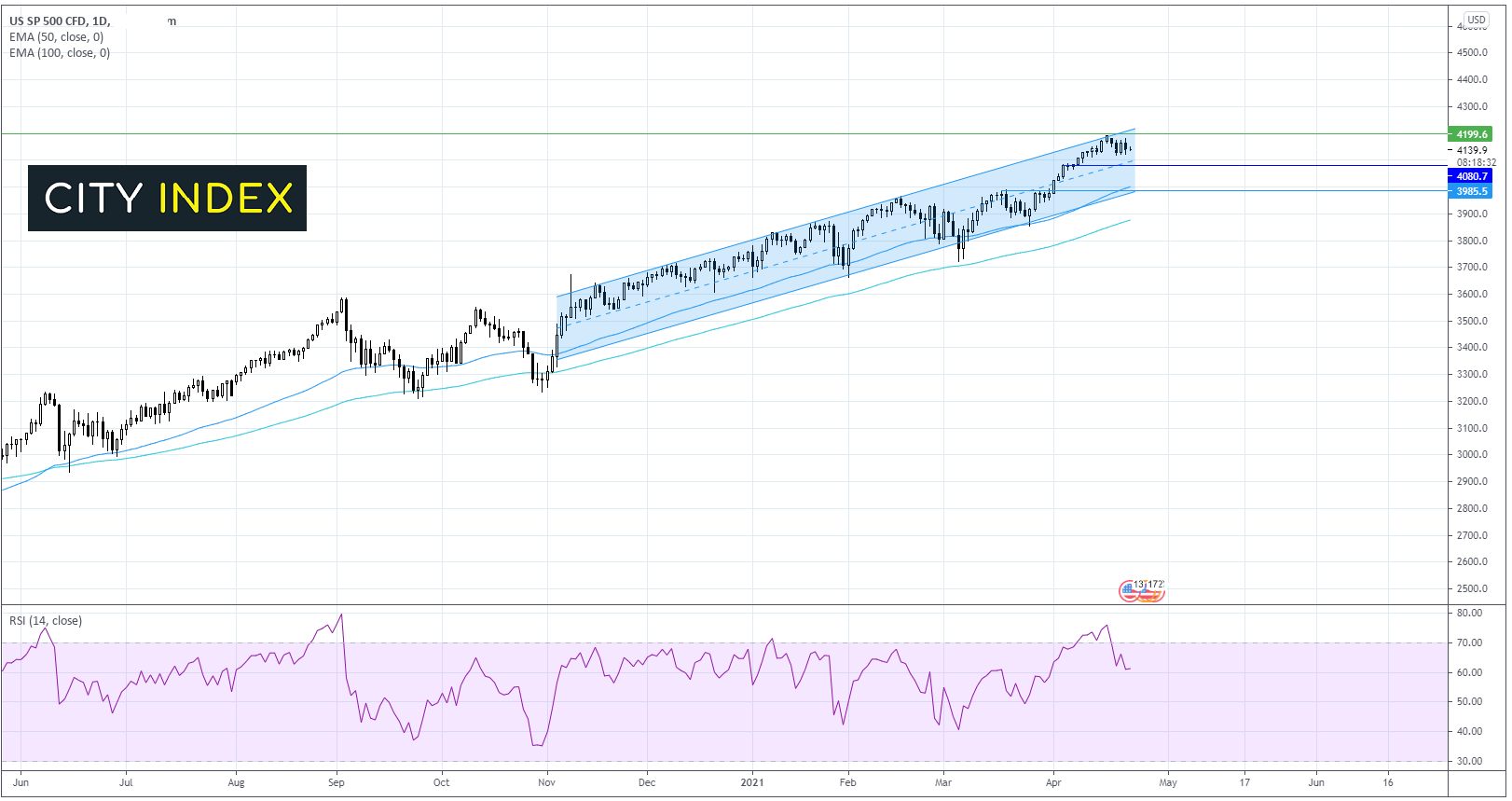

Where next for the S&P?

Despite yesterday’s fall lower, the upward trend remains intact with the US index looking towards its all-time high of 4187. It would take a move below 4000 the 50 EMA on the daily chart to negate the upward trend and there are few signs of such a move currently.

FX – PMIs outperform, UK retail sales surge

The Pound and the Euro are capitalising on the weaker USD.

GBP/USD trades on the front foot following impressive PMI data. The manufacturing PMI rose to 60.7 in April, up from 58.9 and ahead of forecasts of 59. Meanwhile the service sector PMI jumped to 60.1 up from 56.3 in March. This is the first insight as to how the UK economy is performing as it flung open its doors earlier this month.

UK retail sales for March jumped 5.4% month on month, well ahead of the 1.5% increase forecast. Consumers preparing to venture out after months of being locked down helped sales surge, even before non-essential retailers opened their doors.

EUR/USD trades higher on encouraging signs from the economy. The preliminary April composite PMI rose to 53.7 a 9 month high, up from 53.2 in March. The data points to underlying strength in the Eurozone economy and a thriving manufacturing sector. The bloc’s economy is teetering on the brink of a strong recovery.

GBP/USD +0.3% at 1.3891

EUR/USD +0.4% at 1.2063

Oil rises but looks to a weekly loss

Oil prices clawing higher on Friday, lifted reopening optimism in the US and Europe. However, soaring covid cases in India and lockdown restrictions in parts of Japan are keeping gains limited.

The markets are looking past the build in crude inventories reported earlier in the week and surging covid cases in India. An improvement in gasoline demand is helping underpin the price. In Europe, France is set to reopen schools, marking an important step forwards towards reopening the economy.

Despite the move higher today, oil prices are still on track for over 2% losses across the week. Gains could be limited until India in particular, but also Japan, the third and fourth largest consumers of oil turn a corner in their fight against covid.

US crude trades +0.45% at $61.70

Brent trades +0.15% at $65.03

Learn more about trading oil here.

The complete guide to trading oil markets

Looking ahead

14:45 US Manufacturing & services PMI

15:00 US New home sales

Latest market news

Today 08:28 AM

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Yesterday 08:15 AM

Latest Crude Oil articles

April 22, 2024 04:00 PM

April 19, 2024 03:35 AM

April 17, 2024 05:00 PM

April 17, 2024 03:02 AM