US futures

Dow futures +0.2% at 34100

S&P futures +0.5% at 4177

Nasdaq futures +0.85% at 14053

In Europe

FTSE +0.4% at 7023

Dax +0.18% at 15422

Euro Stoxx +0.3% at 4021

Learn more about trading indices

US stocks charge higher

After the S&P and Dow Jones struck an all time high in the previous session, futures are looking to break even higher on Friday.

Strong economic data from the US and an encouraging start to earnings season, in addition to upbeat Chinese GDP data overnight are lifting the mood in the market.

Morgan Stanley reported solid results, beating forecasts for both EPS and revenue and round off a week which has seen blowout earnings for the likes of Citigroup, Bank of America, and JP Morgan.

Chinese GDP records record growth

Overnight data revealed that China’s economy expanded by 18.3% YoY. This was slightly short of the 19% expected but was still the strongest growth ever recorded, albeit from a low base in the pandemic.

The data has come following extremely strong US retail sales data in the previous session. Sales surged 9.8%, against expectations of 5.9% amid improved weather conditions and as households received stimulus checks. Jobless claims also declined by 200k to the lowest level since the start of the pandemic.

Data is pointing to strong economic recoveries in the world’s two largest economy. This bodes well for the global economic recovery and is boosting risk sentiment.

FX – US Dollar traces treasury yields lower.

US Dollar is trading lower versus its major peers, as investors shun the safe haven currency in favour of riskier currencies. A broad upbeat mood in the market is keeping the US Dollar depressed around 4 week lows, even as yields edge higher.

EUR/USD is advancing and trades higher across the week. Despite lockdown restrictions remaining in the region. Germany says that it expects 20% of the population to be vaccinated by then of April.

Eurozone CPI March confirmed preliminary reading of 1.7% YoY, this is up from 1.3% in February.

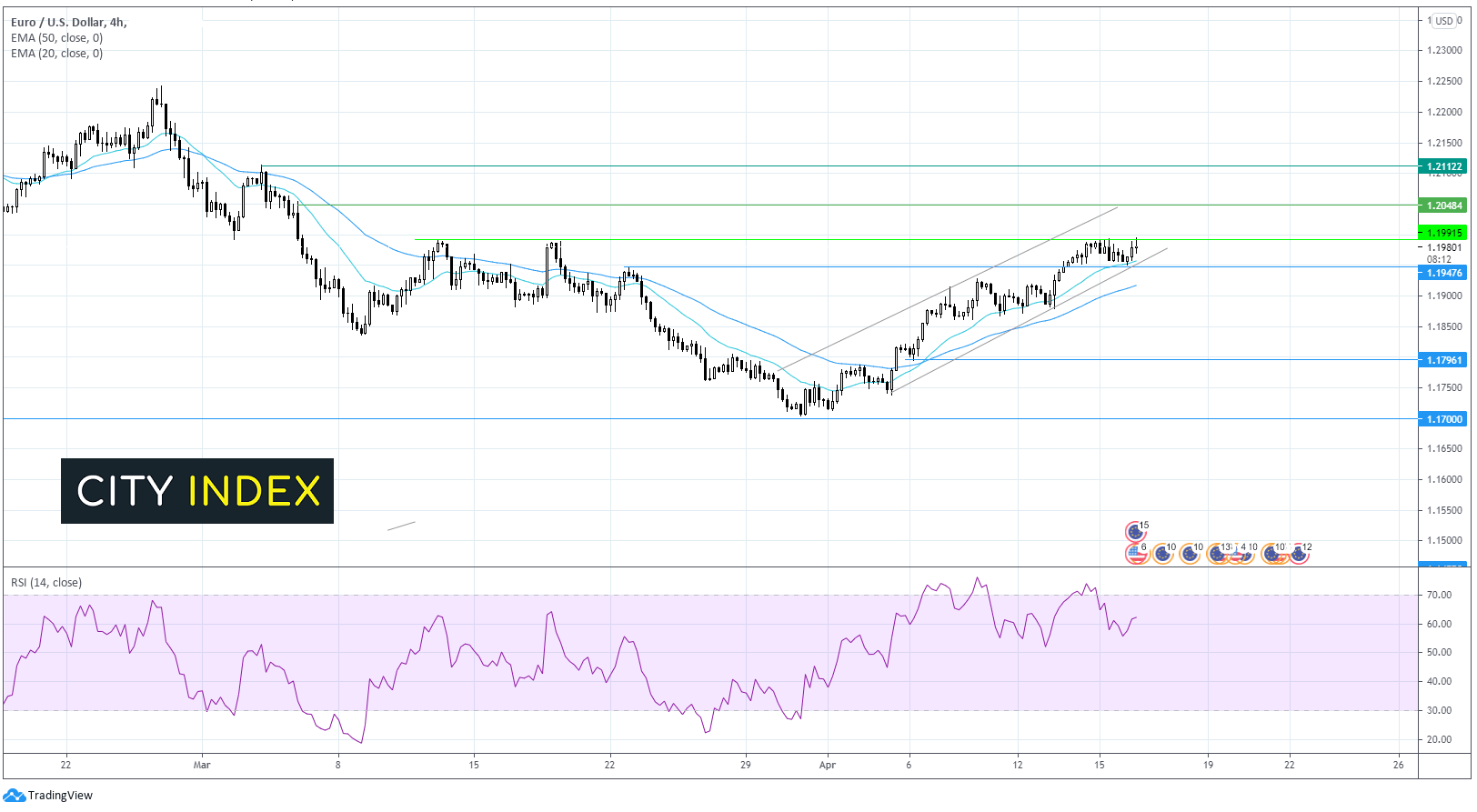

EUR/USD looks to 1.20

EUR/USD has traded within an ascending channel across the month. It trades above its 20 & 50 EMA pointing to bullish trend with upside momentum. The RSI has also fallen out of overbought territory allowing for more upside.

A move above 1.20 the key level is needed in order for the bulls to look towards 1.2050.

Support can be seen at 1.1950 20 EMA and ascending trendline a fall below here could negate the current uptrend.

GBP/USD +0.1% at 1.38

EUR/USD +0.1% at 1.1982

Oil consolidates after strong rally

Oil is consolidating around monthly highs and are on track to gain over 6% across week. Impressive macro data from the US plus record quarterly GDP growth in China points to improving demand prospects. The EIA and OPEC both upgraded oil outlook guidance for 2021.

In addition to upbeat macro data, the US department of transport (DoT) has revealed that traffic levels are on the rise in various states amid the reopening of the economy. Miles driven on US highways are now higher than at the same time in 2019, which bodes well for robust petrol demand in the driving season.

US crude trades +0.03% at $63.50

Brent trades +0.1% at $66.67

Learn more about trading oil here.

The complete guide to trading oil markets

Looking ahead

15:00 Michigan consumer confidence

18:00 Baker Hughes US oil rig count

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest DJIA articles

April 14, 2024 04:00 AM

April 12, 2024 05:46 PM

April 11, 2024 01:11 PM