US futures

Dow futures +0.1% at 34099

S&P futures +0.04% at 4180

Nasdaq futures -0.02% at 13929

In Europe

FTSE +0.4% at 6960

Dax -0.06% at 15286

Euro Stoxx +0.1% at 4019

Learn more about trading indices

US stocks point to a mixed open

US futures are pointing to a relatively quiet open ahead of a very busy week, which sees a slew of earning releases and the Fed’s rate decision.

The Nasdaq is just coming under a bit of pressure heading towards the open as treasury yields tick slightly higher, undermining growth stocks and supporting the cyclicals on the Dow.

Europe to allow US tourists

Covid news has been a little more upbeat with EC President Ursula von der Leyen saying that fully vaccinated Americans will be allowed into Europe this summer. European travel stocks have rallied on the back od the news, with a similar reaction expected in the US market.

Commodities in focus

Commodity prices are surging higher. Copper hit its highest level in a decade. Copper prices have been on the rise in recent weeks, not just on the back of reopening optimism but also in anticipation of strong demand from the car industry, amid an acceleration towards electric vehicles. Furthermore the front runner in the Peruvian elections is threatening to nationalise mining.

Tesla to report

Tesla is due to report after the close. Tesla is expected to report EPS od $0.77c on revenue of $10.42 billion, up 66% from a year ago. The earnings come after the stock surged 740% in 2020 but is up just 3% so far this year amid a series of PR issues in both China and Texas and as competition from other automobile firms heats up.

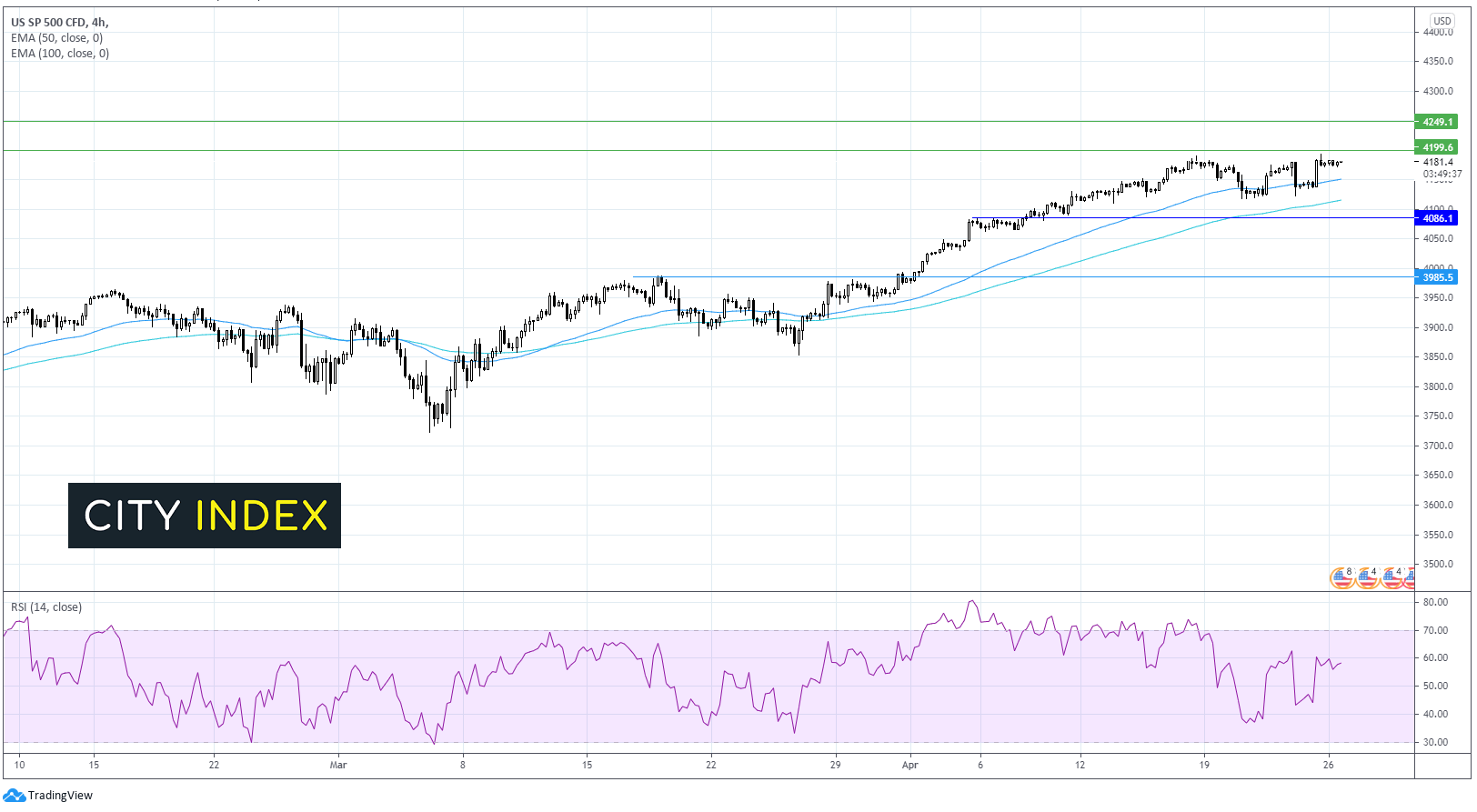

Where next for the S&P 500?

After briefly touching a fresh all time high time high on Friday the S&P 500 eased back. It trades marginally higher on the open. The technical picture remains bullish for the index with the 4200 potentially being hit in the near term, ahead of 4250. Support can be seen at 4150 the 50 EMA.

FX – Euro stumbles on weaker German IFO data

The greenback trades under 91.00 at around an 8-week low ahead of the FOMC later this week.

GBP/USD is capitalising on the weaker US Dollar, edging higher amid hopes of a vaccine led recovery. BoE policymakers’ optimism is adding to the upbeat mood surrounding the sterling.

EUR/USD trades lower after disappointing German IFO business sentiment data with 96.8. This was a slight improvement from March’s 96.6 but was short of the 97.8 forecast. Business morale slipped amid the resurgence of covid and supply issues of industrial components.

GBP/USD +0.05% at 1.3880

EUR/USD -0.1% at 1.2083

Oil extends last week’s losses on covid fears

Both oil benchmarks lost ground in the previous week and are seen extending declines on Monday amid a worsening covid crisis in India and Japan. The world’s third and fourth largest importers of oil have both seen lockdown restrictions tighten which is softening the demand outlook for oil.

On Sunday, Japan announced a state of emergency in Tokyo, Osaka and two other regions. India recorded surging covid numbers, which reached record levels for a fifth straight day. Covid cases hit 350,000 and the lockdown in New Delhi has been extended. Oil buyers will want to see some floor under the covid crisis in order to move meaningfully higher.

US crude trades -1.3% at $61.32

Brent trades -1.4% at $64.58

Learn more about trading oil here.

The complete guide to trading oil markets

Looking ahead

14:00 ECB’s Lane speech

15:30 US Dallas Fed manufacturing business index

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

Latest Crude Oil articles

April 17, 2024 05:00 PM

April 17, 2024 03:02 AM

April 10, 2024 06:07 AM