US futures

Dow futures +0.1% at 35380

S&P futures +0.03% at 4487

Nasdaq futures +0.1% at 15336

In Europe

FTSE +0.33% at 7139

Dax -0.17% at 15882

Euro Stoxx +0.13% at 4180

Learn more about trading indices

Risk off dominates

US stocks are set to open flat struggling to build on record highs reached in the previous session. Caution is creeping in with investors wary of taking out big positions ahead of the Jackson Hole Symposium which kicks off tomorrow.

The focus all week has been on the Jackson Hole Economic Forum. Investors have been flip flopping over whether the Fed will make a taper announcement. The ball has fallen over the other side of the fence to where it was in the lead up to this week with investors broadly expecting the Fed to delay any taper announcement until later in the Autumn, given rising covid cases.

US durable goods orders were mixed. The headline orders figure came in better than forecast contracting -0.1% MoM in July, versus -0.3% decline forecast and a 0.8% rise in the previous month. Orders ex Defense registered at -1.2% below forecasts of 0.4% rise. Futures have inched higher following the release suggesting that the market is taking the data as re-enforcing expectations that the Fed will delay taper talk.

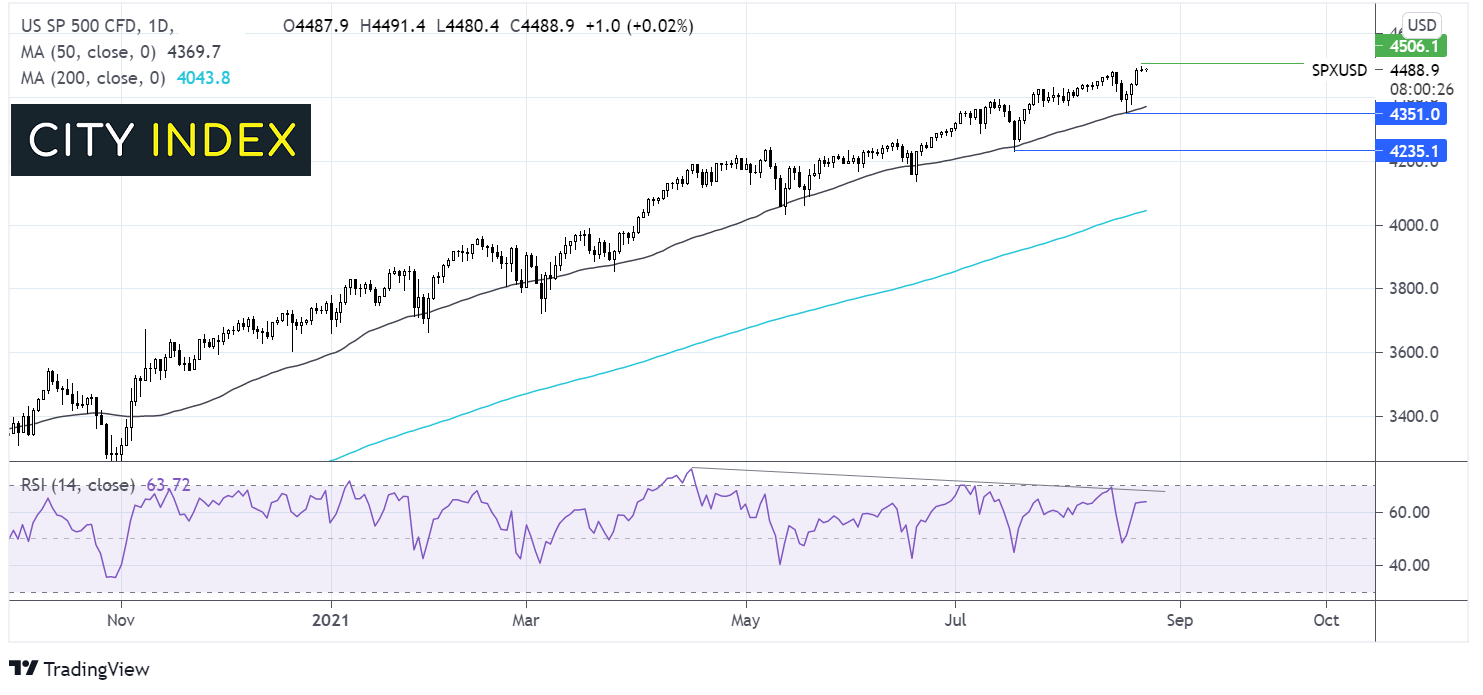

Where next for the S&P500?

The S&P 500 extended its rebound of the 50 sma firmly, reaching a fresh all time at 4486, bringing 4500 round number into sight. The RSI shows a bearish divergence suggesting that momentum is slowing. A move below the 50 sma on the daily chart at 4360 and the low August 19 at 4350 could spark further selling to 4235 the July low.

FX – USD rises after 3 days of losses

The US Dollar is edging higher as it recovers from a three day sell off as Fed Powell is expected to refrain from hinting at tapering the Fed’s $120 billion /month bond purchases.

EUR/USD under pressure after disappointing German IFO business climate index data. The index fell by more than expected to 99.4 in August, its second straight monthly decline. Concerns over rising covid delta cases and the ongoing supply bottlenecks are putting a strain on the economy.

GBP/USD -0.1% at 1.3712

EUR/USD -0.16% at 1.1737

Oil extends gains on vaccine optimism

Oil prices are extending gains for a third straight day, although the run higher appears to be running out of steam. Oil started the day lower after API data revealed that stock piles declined by a less than expected 1.6 million barrels. Expectations were for a draw of 2.7 million.

Oil prices have rallied over 8% so far this week erasing 5% losses from the previous week. A falling US Dollar and China singing victory against its latest covid wave on Monday and news of Mexican oil supply falling owing to a platform fire on Tuesday have overshadowed concerns of rising covid cases globally.

EIA crude oil inventory data is due later today.

US crude trades +0.3% at $67.67

Brent trades +0.38% at $70.73

Learn more about trading oil here.

The complete guide to trading oil markets

Looking ahead

15:30 EIA Crude Oil Stock Change

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels

- Place the trade.

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Latest Crude Oil articles

April 22, 2024 04:00 PM

April 19, 2024 03:35 AM

April 17, 2024 05:00 PM

April 17, 2024 03:02 AM