US futures

Dow futures -0.4% at 33900

S&P futures -0.5% at 4186

Nasdaq futures -0.7% at 13860

In Europe

FTSE +0.35% at 6988

Dax +0.34% at 15207

Euro Stoxx -0.02% at 3992

Learn more about trading indices

US stock point lower today but set to end the week flat

US stocks are heading for a weaker start on the open as investors look to book profits after a strong week of earnings and as inflation ramps up in March.

The three main indices closed higher in the previous session. Yet across this week indices have traded relatively flat, especially when considering the amount of information that has hit the markets this week.

Earnings

Amazon will be in focus on the open after reporting blowout numbers after the close on Thursday to round off a strong earnings season from the big tech. Amazon reported a 44% surge in sales, buoyed by the pandemic. EPS came in at $15.79 against forecasts of $9.54 on revenue of $108.52 billion, against $104.47 expected.

Twitter shares are plunging 12% pre-market after beating forecasts on revenue and profits but warning on slowing growth and outlook.

PCE inflation

The Fed’s favorite gauge of inflation Personal Consumption Expenditure came in well above expectations. PCE rose 2.3% YoY in March, up sharply from February’s 1.5% and well ahead of 1.6% forecast. On a monthly basis PCE jumped 0.5%, up from 0.2% and ahead of the 0.3% forecast.

Personal income soared by the most on record powered by the third round of stimulus checks from the federal government.

The Fed has repeatedly said that it considers any rise in near term inflation to be short term. It would need to see a sustained rise over 2% inflation in order to consider raising interest rates.

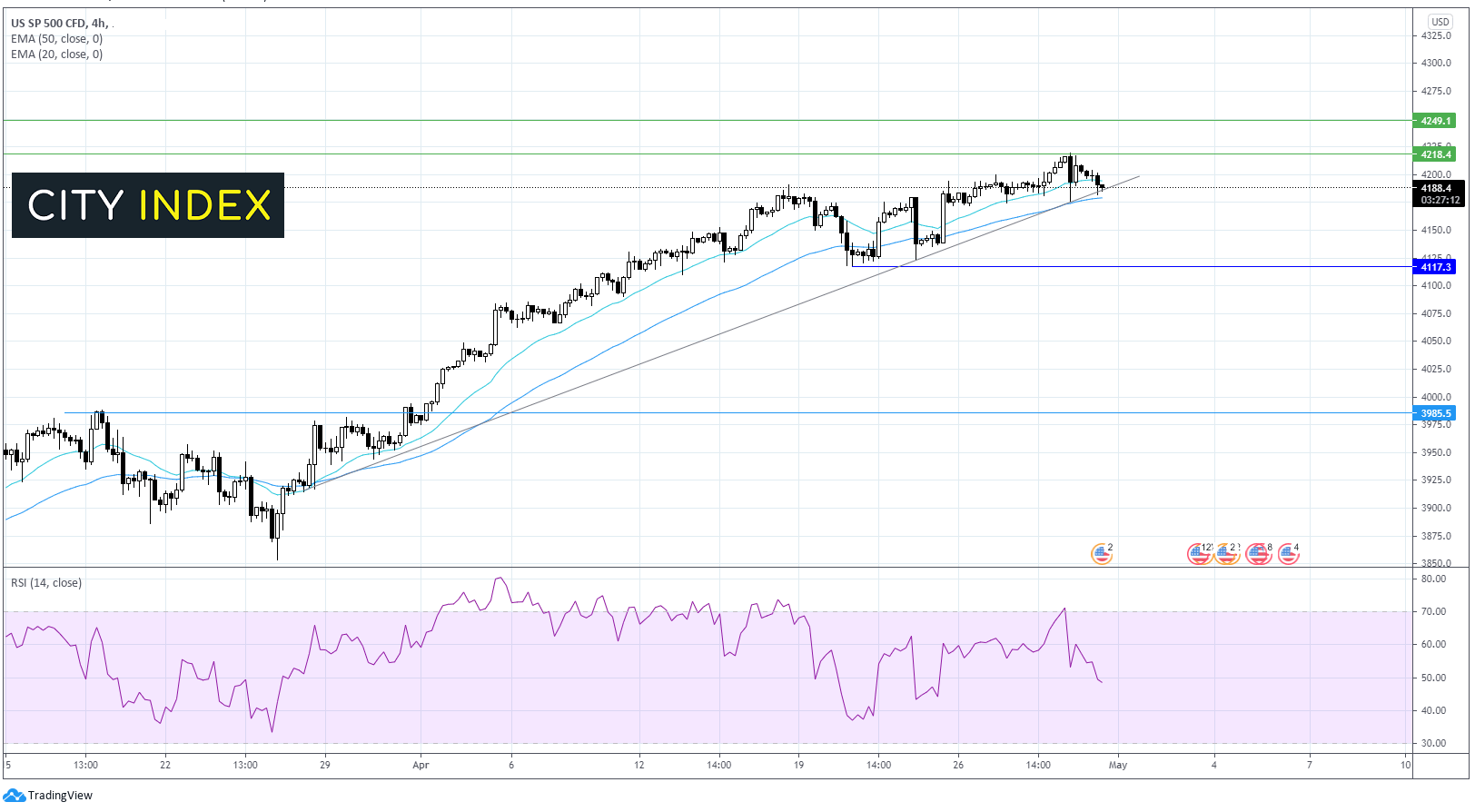

Where next for the S&P?

The S&P trades above its 2 week ascending trendline on the 4 hour chart. It struggled to push beyond resistance at 4200 the all time high and his since edged lower. Having fallen through the 20 sma, the price is currently testing the ascending trendline support and 50 sma around 4185. A move below here could negate the near term bullish trend. However, it would take a move below 4100 for the bears to gain traction.

FX – US Dollar extends gains, EZ enters recession

The US Dollar is rising after yesterday’s GDP beat. US Q1 GDP printed at 6.4% on an annualized basis, up from 4.3% in the previous quarter. PCE data could drive the USD later today.

EUR/USD is under-performing after the Eurozone entered a technical recession. The Eurozone economy contracted by -0.6% QoQ in Q1 2021. This was a slight improvement from the -0.7% contraction in Q4 2020 and better than the -0.8% contraction forecast. However, Germany was a larger concern with GDP contracting -1.7% QoQ as covid cases remain elevated and the country in lockdown.

GBP/USD -0.15% at 1.3919

EUR/USD 0.26% at 1.2087

Oil slips off star off two month high

Oil is edging lower after hitting a two month high in the previous session. Even so, oil is still on for solid 4% gains across the week and hefty 9% gains across the month of April.

Rising demand optimism has been lifting the price. Strong than expected GDP data from the US, the world’s largest consumer of oil fueled that optimism further.

The covid crisis in India continues to escalate with another record number of daily cases recorded. India the largest importer of oil recorded over 380,000 new daily cases suggesting that the peak still hasn’t been reached. Lockdown extensions could hurt the demand outlook.

US crude trades -1.7% at $63.84

Brent trades -1.5% at $67.77

Learn more about trading oil here.

The complete guide to trading oil markets

Looking ahead

15:00 University of Michigan confidence

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest Crude Oil articles

April 22, 2024 04:00 PM

April 19, 2024 03:35 AM

April 17, 2024 05:00 PM

April 17, 2024 03:02 AM