US futures

Dow futures -0.55% at 34425

S&P futures -0.65% at 4181

Nasdaq futures -1% at 13547

In Europe

FTSE -0.95% at 7031

Dax -0.3% at 15546

Euro Stoxx -0.5% at 4067

Learn more about trading indices

Stocks drop on Fed tightening fears

US futures are tumbling lower following the US data deluge. The impressively strong figures from the labour market are fueling bets that the Fed will be forced to tighten monetary policy sooner.

The ADP payroll report revealed that 942k new jobs were created in the private sector in May, this is up firmly from 742k recorded in April and defies expectations of a slight decline to 642k.

US jobless claims also fell to a fresh pandemic low of 385k last week, down from a downwardly revised 405k before that. 390K initial claims had been forecast.

The US economy is roaring back to life amid a successful vaccine programme and the reopening of businesses as pandemic restrictions are lifted. These data points bode well for tomorrow’s non-farm payroll which will be key in deciding the Fed’s next steps

Expectations of an earlier move by the Fed is being reflected in a stronger US Dollar and falling futures, particularly high growth tech stocks which are more sensitive to interest rate expectations.

The Nasdaq is set to underperform its peers with futures trading down over 1% whilst the Dow which is more closely tied to value stocks sees its futures trade down 0.6%. The Fed’s ultra-lose monetary policy has been the stock markets best friend across the pandemic; a relationship which could weaken and quickly.

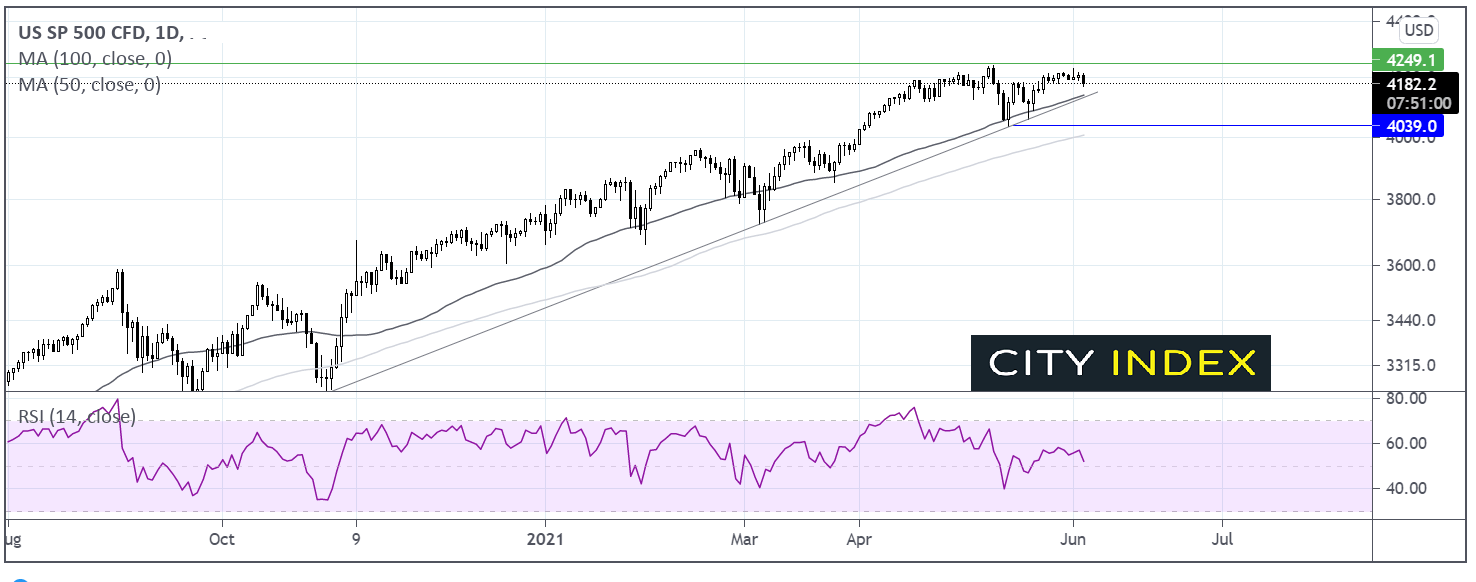

Where next for the S&P 500?

The S&P 500 is trading lower as it continues to hover around all time highs. The index lacks the oomph needed to break above resistance at 4250 currently. However, today’s fall lower is not enough to negate the current up trend. A move below 4150 the multi month ascending trendline support and the 50 sma could open the door to 4050. A move below 40509 is needed to create a lower low. Meanwhile buyers will look to retake 4250.

FX – USD jumps, GBP remains resilient after strong services PMI

The US Dollar was trading on the front foot ahead of the ADP payroll release and extended those gains following the data.

GBP/USD is holding its ground versus the US Dollar after impressive service sector PMI data. Services PMI rose to 62.9 in May, as the sector expanded at the quickest pace in 24 years as lockdown restrictions eased and bars, restaurants and pubs re-opened inside hospitality.

GBP/USD -0.04% at 1.4175

EUR/USD -0.25% at 1.2182

Oil pauses for breath ahead of EIA data

After 3 straight days of gains oil bulls are pausing for breath. Oil prices have been charging higher as rising demand expectations in the second half of this year overshadow the decision by OPEC+ to stick with the plan to continue easing production cuts.

UK fuel demand has reached pre-pandemic levels. China is also seeing demand rise and the US, the worlds’ largest consumer of oil is expected to see a strong US driving season. The broad expectation is that demand will out strip supply in the second half of the year, supporting prices at these levels.

EIA crude stockpile data is due later. Expectations are for a decline in inventory.

US crude trades -0.12% at $68.67

Brent trades -0.02% at $71.24

Learn more about trading oil here.

The complete guide to trading oil markets

Looking ahead

15:00 ISM non-manufacturing PMI

15:30 EIA crude stock pile data

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM

Latest Crude Oil articles

April 17, 2024 05:00 PM

April 17, 2024 03:02 AM

April 10, 2024 06:07 AM