US futures

Dow futures +0.15% at 34758

S&P futures +0.2% at 4370

Nasdaq futures +0.3% at 14844

In Europe

FTSE +0.11% at 7023

Dax 0% at 15624

Euro Stoxx -0.1% at 4050

Learn more about trading indices

A positive end to a choppy week

US futures are pushing higher on the open. Investors are brushing off news that the Biden administration will warn businesses over rising risks of doing business in Hong Kong and instead are focusing on better than forecast retail sales and a relatively upbeat start to earnings season.

The US banks have kicked off earnings season, most beat forecast on both earnings and revenue thanks in part to a surge in deal making. The low interest rate environment combined with businesses eager to reorganize and digitalise has sent deal making to record levels.

Retail sales rose by a better than expected 1.3% MoM in June, up from an upwardly revised -0.9% decline in May and well ahead of the -0.4% drop expected. Retail sales are notoriously volatile and this year this is particularly the case. As a result, its proving difficult to draw any strong trends for the data. The fact that it rose and firmly is a good sign for now. Jerome Powell said that the recovery still had a way to go. This is movement in the right direction.

Looking ahead Michigan consumer confidence data will be in focus.

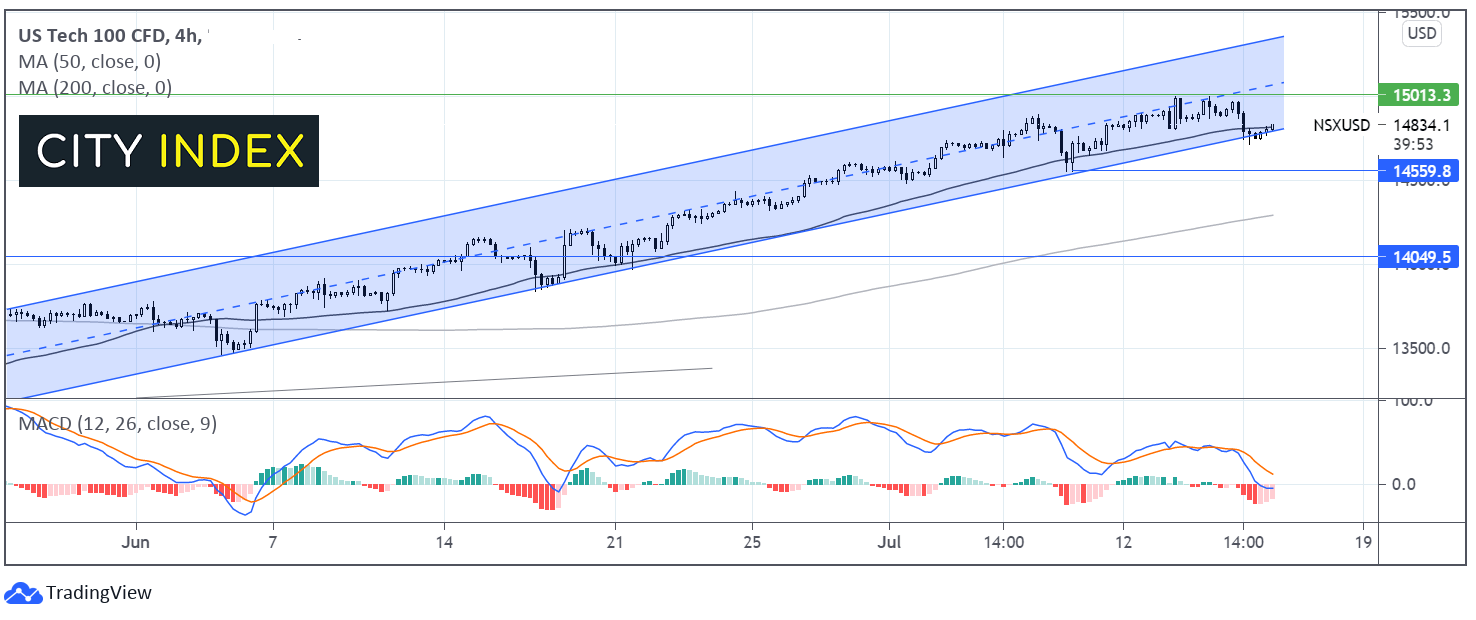

Where next for the Nasdaq?

The Nasdaq refreshed its all time high earlier in the week before easing lower. Yesterday’s selloff took the index through its 50 sma on the 4 hour chart. The price is rebounding after finding support on the ascending trendline dating back to mid May. The MACD’s receding bearish bias is supportive of a move back over the 50 sma and back towards 15000. A break out of the ascending channel could prompt a deeper selloff to 14550.

.

FX – USD rises, EUR shrugs off inline inflation

The US Dollar is moving higher, extending gains from the previous session. The US Dollar is set to gain over 0.5% this week its strongest weekly gains in over a month, boosted by safe haven flows as delta cases rise and elevated inflation prompts speculation of the Fed tightening policy.

EUR/USD hovers around 1.18. Final Eurozone CPI came in as expected at 1.9% YoY in June, down from 2% in May. Concerns over the spread of the Delta variant are also dragging on sentiment for the common currency,

GBP/USD -0.14% at 1.3810

EUR/USD -0.28% at 1.1795

Oil set for 4% losses across the week

Oil prices are edging higher but are set for steep weekly declines. Both benchmarks are looking at losses of over 4% across the week. A compromise at OPEC paves the way for output increases to match surging demand as economies reopen.

Concerns over a rise in fuel inventories is also capping gains, particularly given that the driving season should be ramping up in the US around 4th July holiday.

US crude trades +0.25% at $71.59

Brent trades +0.13% at $73.14

Learn more about trading oil here.

The complete guide to trading oil markets

Looking ahead

14:00 Fed Williams Speaks

15:00 Michigan Consumer Confidence

18:00 Baker Hughes Oil Rig Count

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels

- Place the trade.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Crude Oil articles

April 22, 2024 04:00 PM

April 19, 2024 03:35 AM

April 17, 2024 05:00 PM

April 17, 2024 03:02 AM