US futures

Dow futures +0.49% at 35431

S&P futures +0.5% at 4508

Nasdaq futures +0.43% at 15365

In Europe

FTSE +0.05% at 7208

Dax +0.09% at 15494

Euro Stoxx +0.23% at 4160

Stocks rise, Netflix to report after the close

US stocks are pointing to a stronger start as the spotlight falls on earnings. Upbeat numbers from Johnson & Johnson come following impressive figures from the banks last week and are helping to set a positive tone for the session.

US indices have recovered well from the blip that sent them lower testing the 200 day moving average at the end of last month. The rebound has the S&P just over 1% shy of its all time high again. Another week of upbeat results could be the boost that bulls are after to recapture those record levels. However, it is worth noting that banks aren’t particularly exposed to supply chain constraints which have been hampering the economic recovery.

Netflix is due to release earnings after the bell and will almost certainly focus attention on the tech giants as they prepare to dish out their numbers next week.

Separately energy stocks are on the rise, tracing oil prices higher as the energy crunch shows no signs of letting up.

Significantly weaker than expected housing data was also brushed aside no doubt to return to haunt the market at a later date.

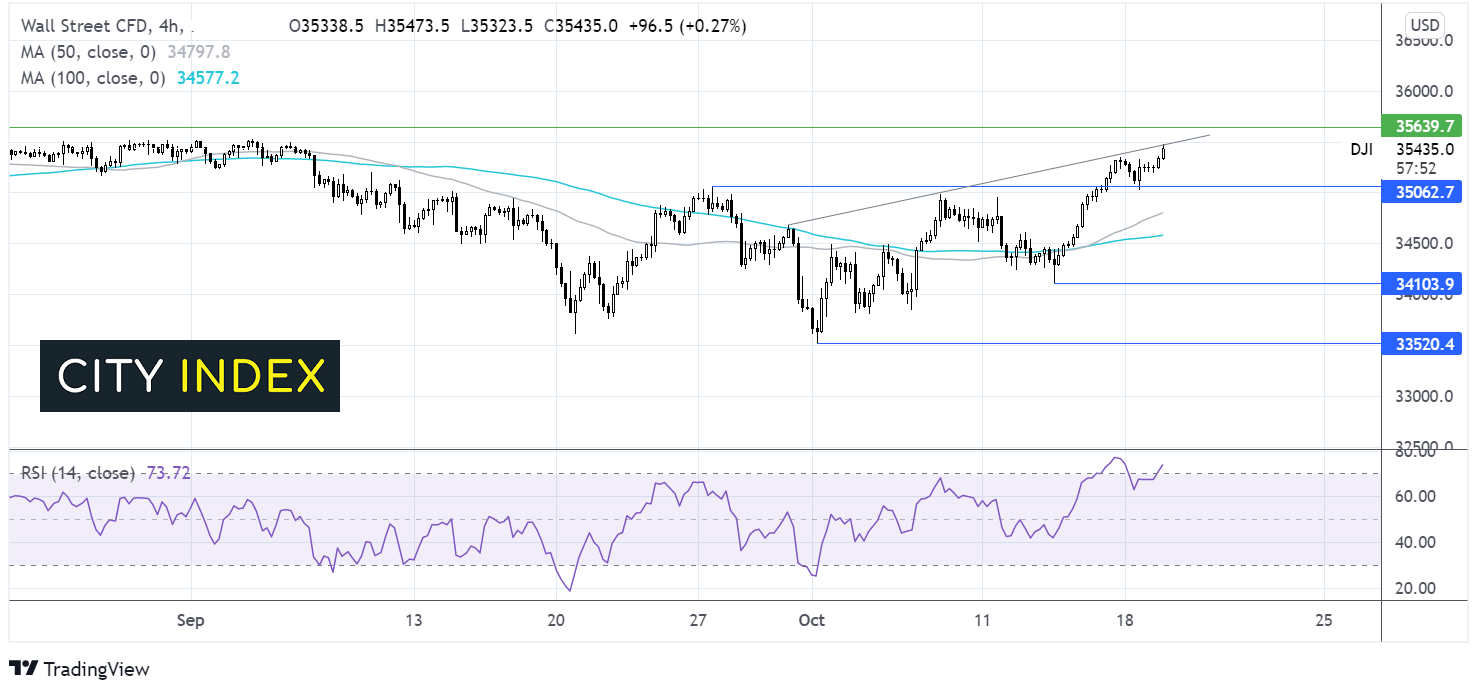

Where next for the Dow Jones?

The Dow Jones is extending the rebound from 34100 hit last week pushing through the 50 & 200 sma on the 4-hour chart. The Dow has also broken above the 34064 horizontal resistance keeping buyer optimistic and setting their sights on 35600 and fresh all-time highs. The RSI is in overbought territory so some consolidation, or a pull back could be on the cards. Watch for trendline resistance at 35475.

FX – USD drops, GBP rallies on BoE expectations

The US Dollar is falling sharply lower amid expectations that other major central banks could start tightening monetary policy begore the Federal Reserve. Fed speakers are in focus in an otherwise quiet economic calendar.

GBP/USD is charging higher as bets rise that the Bank of England could start hiking rates as soon as this year. UK CPI data is due tomorrow. So far the Pound is ignoring the fact that covid cases are rising sharply, just shy of 50,000 new daily cases.

GBP/USD +0.73% at 1.3826

EUR/USD +0.4% at 1.1661

Oil gains ground

Oil prices are extending gains on Tuesday as the ongoing energy crisis shows few signs of easing. The crunch in natural gas, coal and electricity continues whilst temperatures fall in China the world’s second largest economy fueling fears of shortages and boosting the appeal of oil as a comparatively cheap alternative. Coal futures in China rose 7.8%. As the northern hemisphere moves towards the colder months, the situation is only going to deteriorate, as colder temperatures boost heating demand.

API inventory data is due later today.

WTI crude trades +1.8% at $82.64

Brent trades +0.84% at $84.57

Looking ahead

15:00 ECB Lane speaks

16:00 Fed Daly speaks

19:50 Fed Bostic speaks

21:30 API crude oil inventories

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels

- Place the trade.

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest Indices articles

Yesterday 03:30 PM

April 18, 2024 04:46 PM