US Jobs Good Enough for Accommodative Tapering

July non-farm payrolls disappointed with a rise of 162K jobs, undershooting expectations for 195K. On the positive side, the unemployment rate fell to 7.4%, the […]

July non-farm payrolls disappointed with a rise of 162K jobs, undershooting expectations for 195K. On the positive side, the unemployment rate fell to 7.4%, the […]

July non-farm payrolls disappointed with a rise of 162K jobs, undershooting expectations for 195K. On the positive side, the unemployment rate fell to 7.4%, the lowest level since December 2008. The 162K rise in NFP was accompanied by a net increase of 47K jobs in retail sector (the highest monthly increase since November), 6K rise in manufacturing and 36K rise in services industries.

Will the hawks and the doves at the Fed give more weight to the Establishment survey’s NFP figure or be swayed by the headline friendly unemployment rate, prepared by the household survey? Despite the miss in NFP, today’s release is the 13th consecutive monthly figure of above 100K, the longest such streak in over 13 years. Meanwhile, the underemployment rate (rate of those employed at jobs/salaries below their standards) fell to 14.0%, nearing the 5-year low attained in May.

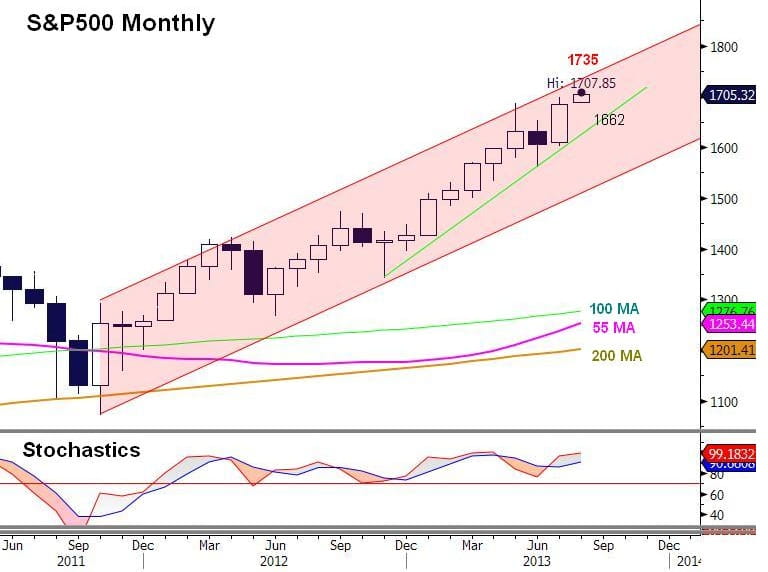

The market reaction maybe just what the Fed needed; 10-year yields fell 15-bps off their 2.75% resistance—marking the downward trendline from the 7-year high. This avoids an excessive rise in borrowing costs for now while consumer-related metrics and corporate valuations are allowed more time to improve with a lower discounting factor.

The doves at the Fed focusing on disinflationary risks, could point to the slowdown in y/y average hourly earnings to 1.9% from 2.1%. They could also refer to this week’s FOMC statement indicating the condition for the “the outlook for the labor market [to have had] improved substantially in a context of price stability”.

Accommodative Tapering

Combining the overall developments in today’s jobs report and the jobless claims having hit their lowest level since January 2008, it is without a doubt that labour markets have indeed improved, albeit not “substantially”. The figures are justifiable for keeping everyone happy: taper the asset purchases by $10bn or $15bn, while the balance sheet continues to expand, accommodation remains in place, and the Fed could reiterates forward guidance for rates to remain low until 2015.

Such accommodation avoids the dollar entering another aggressive rally, especially as the Bank of England, European Central Bank and Bank of Japan grow issue more forceful guidance aimed at battling rising yields.