September 3, 2019 12:12 PM

US ISM Manufacturing PMI Disappoints

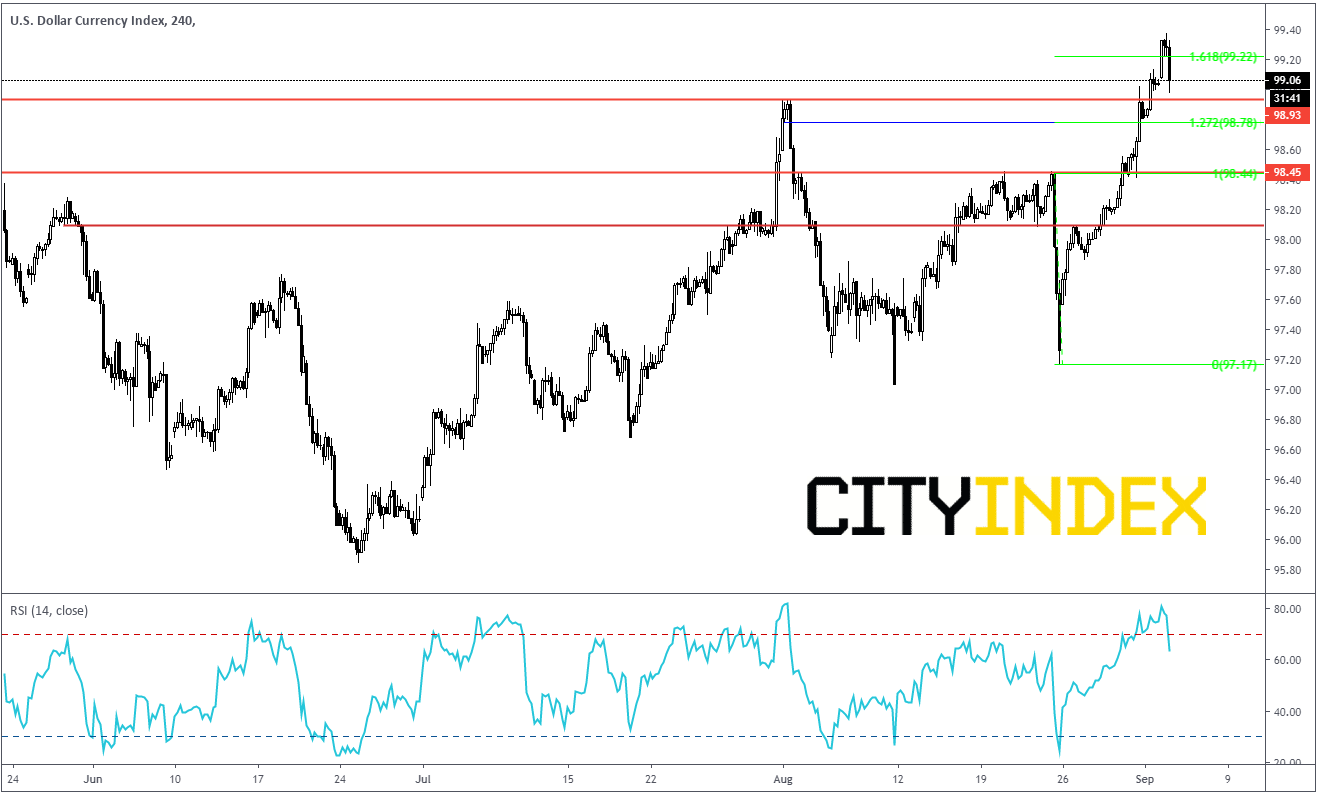

US ISM Manufacturing PMI for August came in at 49.1 vs 51.1 expected and 51.2 last. A reading below 50 generally signals a contraction in the economy. With the reading below 50, the US now joins much of the world in a manufacturing slowdown. Upon release of the data, the DXY immediately traded from 99.25, just about the 161% extension of the August 23rd highs to lows, to below 99.00. Immediate support is previous highs (which now acts as support) from August 1st at 98.93. On this move lower, RSI has also unwound from previously O/B conditions. Next support level is horizontal support at near 98.10.

Source: Tradingview, City Index

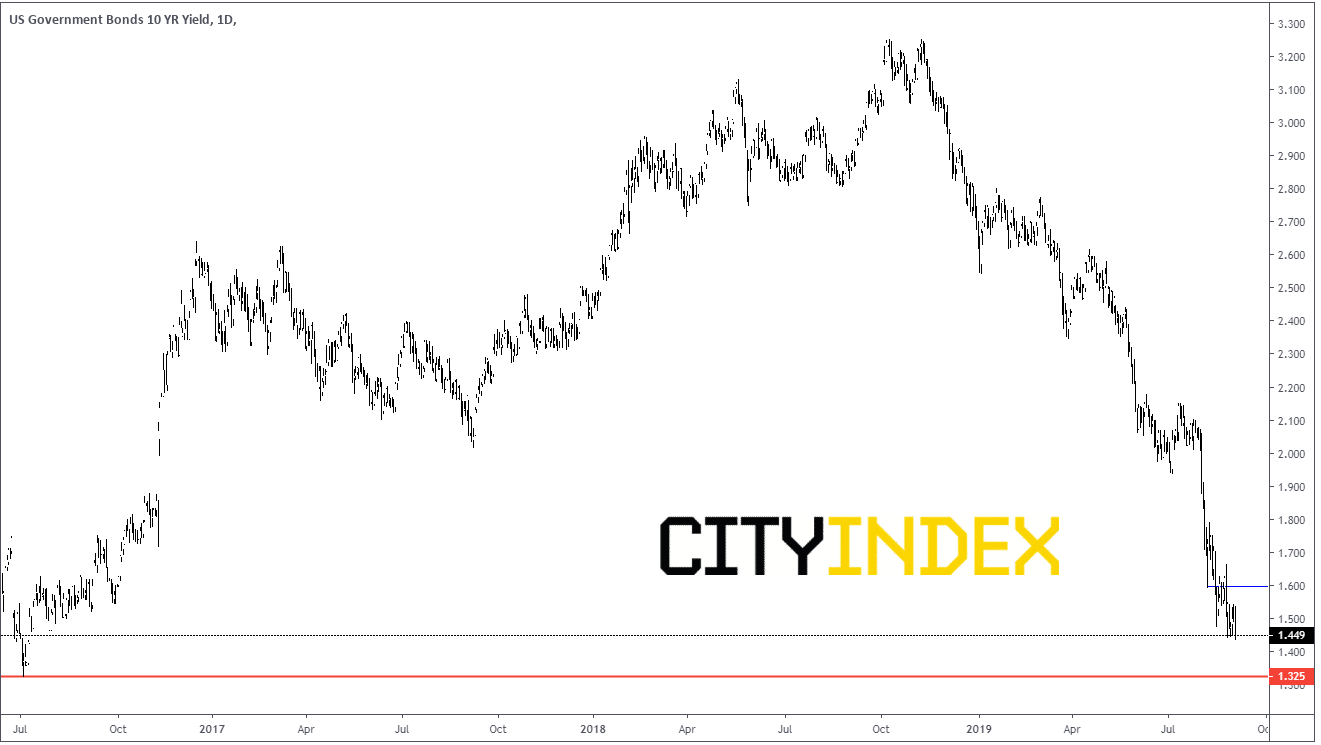

At the same time, US 10 Year Yields moved from above 1.50 to below 1.44. Next level of support comes in at the July 2016 lows near 1.325. Good resistance doesn’t come into play until far above near 1.60.

Source: Tradingview, City Index

The market had already priced in a 100% chance of a rate cut at the September 18th FOMC meeting before the data release. However, now odds for a 50bps hike have increased slightly. Next important piece of data to watch is non-farm payrolls on Friday. Currently expectations are for 150,000 private jobs created in June vs 148.000 in July.

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest Bonds articles

April 23, 2024 11:09 PM

April 22, 2024 03:42 AM

April 18, 2024 06:20 AM

April 10, 2024 01:09 AM