US Dollar What s behind the world reserve currency s disappointing performance

It was another disappointing week for risk asset bulls. After showing signs of stabilizing early in the week, global stocks (led by Chinese equities) dropped […]

It was another disappointing week for risk asset bulls. After showing signs of stabilizing early in the week, global stocks (led by Chinese equities) dropped […]

It was another disappointing week for risk asset bulls. After showing signs of stabilizing early in the week, global stocks (led by Chinese equities) dropped off the map on Friday as concerns about the oil market once again spooked traders. Some of the world’s most important equity markets, including the S&P 500, FTSE, DAX, Nikkei, and Shaghai Composite, are all testing key medium-term support levels as of writing, so a bounce is certainly possible in the coming week. Regardless of what global equities do though, the bigger story might be that the world’s reserve currency has dropped the ball in what should have been a perfect environment for the US dollar rally.

As we go to press, the “safe haven” US dollar index is trading near 98.60, essentially unchanged from last week’s close of 98.40. With market volatility shooting through the roof and global economic concerns elevated, why haven’t traders rushed to the perceived safe haven of the greenback? This week’s US data was hardly inspiring, but the real reason why the dollar couldn’t catch a bid is that its position on the “risk spectrum” has evolved over the last few months.

With the Fed embarking on what it suggests could be a prolonged rate hike cycle, long-term traders bought the greenback in anticipation of increasing carry in the future. In other words, the dollar had evolved, at least to some extent, into a trade where traders sought a return on their capital, rather than just the return of their capital. With sentiment souring at the start of the year, a portion of the traders have chosen to cash out of US dollar longs in favor of the ultra-low-yielding Japanese yen, which has surged more than 600 pips against the US dollar in the last month alone.

So what’s next for the greenback?

Despite this week’s lackluster performance, the dollar could still be a big beneficiary moving forward. If fears about China, oil, and a potential global slowdown continue to dominate, the dollar should eventually regain its safe haven status; after all, the US economy is still the proverbial “best house in a bad global neighborhood”, backed by the world’s most liquid markets and most powerful military.

Conversely, the dollar may also catch a bid if the current market swoon turns out to be an overreaction, as the Fed remains the most hawkish of the major central banks. While the median Fed member’s expectation of raising interest rates four times this year is looking increasingly fanciful, traders are now fully pricing in only a single rate hike this year, with an implied 27% chance of no rate hike at all in 2016, according to the CME’s FedWatch tool. That pessimistic assumption could shift dramatically in favor of dollar bulls if we see some optimistic signs out of China in the coming week.

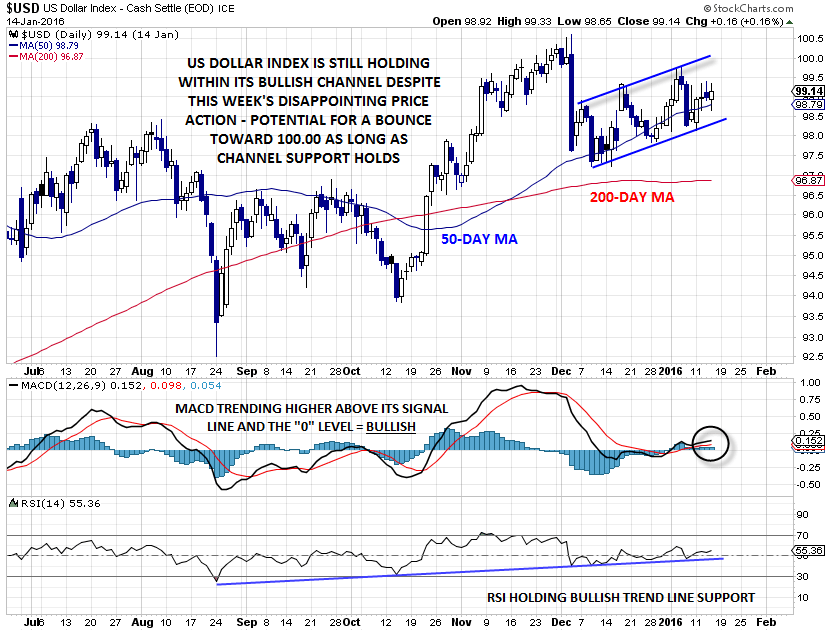

Technical view: Dollar Index

On a technical basis, the dollar index is trading between 98.00 and 99.00, essentially in the middle of its six-week range. Over the last couple of weeks, the weighted index has at least been able to put in a series of higher highs and higher lows, creating a near-term bullish channel in the process (see chart below). Meanwhile, the MACD is trending higher above both its signal line and the “0” level, showing bullish momentum, while the RSI indicator is holding above a multi-month bullish trend line of its own. Moving forward, a rally toward the 100.00 level on the dollar index will be favored as long as bullish channel support at 98.25 holds.