US Dollar Multi year high in Core CPI revives Fed rate hike expectations

After getting clobbered in the first two weeks of February, last week’s recovery in the US dollar was hardly surprising. What was more surprising though […]

After getting clobbered in the first two weeks of February, last week’s recovery in the US dollar was hardly surprising. What was more surprising though […]

After getting clobbered in the first two weeks of February, last week’s recovery in the US dollar was hardly surprising. What was more surprising though was the fact that it was actually driven by decent US economic data.

Last week, we noted the stronger-than-expected January US Retail Sales report, noting that the report represented, “just the most recent evidence that the US economy is, at worst, continued to muddle through,” and that “it’s hard to square the decent economic data with the sharp declines in investor sentiment.” Today’s consumer price index report represents another solid report in the same vein.

Consumer prices were flat (0.0%) m/m on a headline basis, which was actually a tick better than the -0.1% reading expected, but the more impressive reading by far was the “Core” CPI. Consumer prices excluding volatile food and energy components actually rose 0.3% m/m, driving the year-over-year rate to 2.2%, the highest reading since 2012.

While the Fed prefers to focus on an alternative measure of consumer prices called Core Personal Consumption Expenditures (PCE), the historically close correlation between the two, not to mention the strong gains in average hourly earnings in last month’s jobs report, suggests that price pressures may finally be starting to rise meaningfully in the US. Fed Funds futures traders are only pricing in about a 40% chance of another Fed rate hike at all this year, but if inflation continues to rise, expectations and the dollar itself should rise in sync.

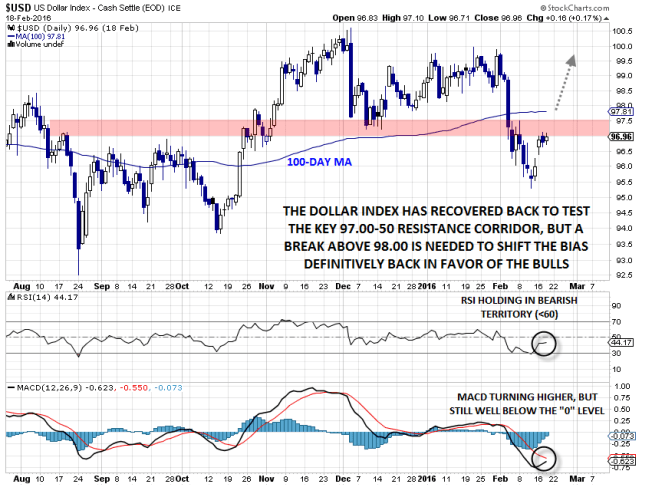

Technical view: Dollar Index

On a technical basis, the US dollar index did bounce back this week, but the move is still viewed as an oversold bounce after the early-February collapse. As of writing on Friday afternoon, the dollar index is trading near the 97.00 level, testing the critical 97.00-50 range that has served as both support and resistance over the last few months.

The secondary indicators are predictably subdued, with both the RSI and the MACD holding in bearish territory, so bulls will need to see those improve before growing confident that dollar recovery is meaningful. On a price basis, a move back above 98.00 would shift the bias back in favor of the bulls for a potential continuation up toward 100.00 next.