US CPI explodes higher in June: Can Powell placate policymakers?

This morning’s data just made Jerome Powell’s week much more difficult.

The Chairman of the Federal Reserve, along with his colleagues, has consistently argued that any elevated inflation readings coming out of the COVID recession would be merely “transitory” as supply chains and shortages worked their way through the system. And while technically he could still be right, it doesn’t mean this week’s testimony to an uneasy Congress will be any easier.

Both the headline and “core” (excluding food and energy) CPI reports for June showed consumer prices rose at 0.9% m/m, crushing expectations of a 0.5% and 0.4% m/m rise respectively. Following this morning’s release, the year-over-year headline US inflation rate is now 5.4%, the highest reading in nearly 13 years; meanwhile, the core CPI reading is up 4.5% y/y, its highest reading in 30 years!

Digging into the numbers, we’re seeing the same theme driving prices higher: Sectors that were particularly influenced by the shutdown – including used car prices, air fares and transportation costs – are driving the bulk of the move. Indeed, used car and truck prices surged another 10.5% accounting for more than a third of the overall rise in the CPI index.

As automakers finally start to secure new chips and ramp up production, the supply of vehicles on the market should start to ease, and other industries should eventually be able to work through their own disruptions as well. However, the risk is that rising prices become psychologically entrenched among US consumers, encouraging them to spend more aggressively and exacerbating the very inflationary prices they’re concerned about in the first place. To wit, according to a New York Fed survey released Monday, consumers see prices overall up 4.8% in the next 12 months, among the higher readings in decades.

Market reaction:

Markets are still digesting the data as we go to press, but the biggest moves so far suggest traders are preparing for potentially earlier and more aggressive rate hikes from the Fed. The short-term 2-year Treasury yield shot up a quick 3bps to 0.26%, near its highest level since the COVID recession, and the US dollar has rallied 40-50 pips against all of its major rivals as well. Not surprisingly, commodities that are priced in US dollars, including gold and oil, are seeing a kneejerk reaction lower.

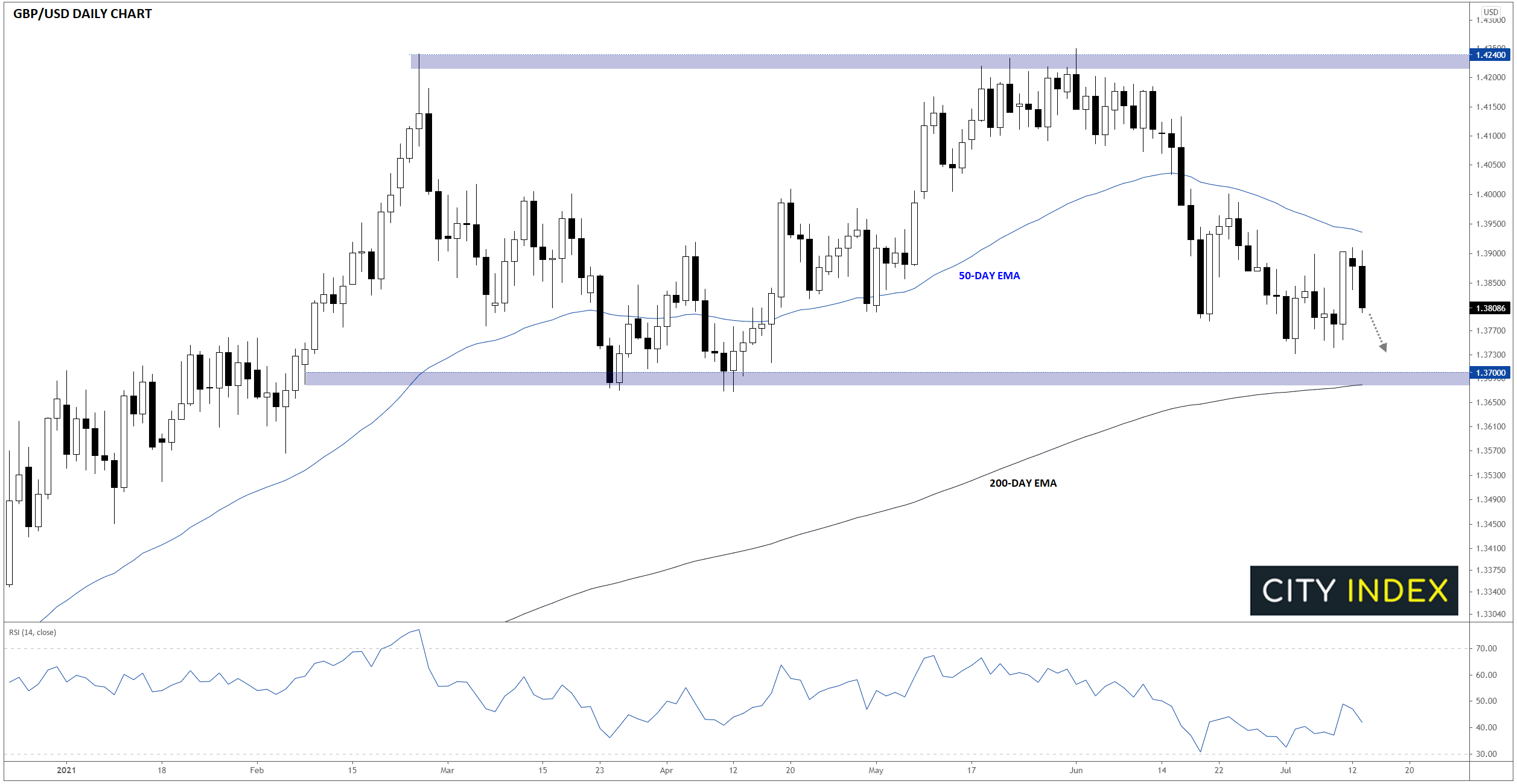

Looking at GBP/USD, rates have rolled over after approaching the 50-day EMA near 1.3900 yesterday. With US inflationary pressures still accelerating, bearish traders may look to push the pair down toward last week’s lows in the mid-1.3700s or even the six-month lows (and 200-day EMA) near 1.3700 as the week proceeds:

Source: StoneX, TradingView

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Latest GBP articles

April 3, 2024 02:49 AM

March 29, 2024 10:00 PM

March 9, 2024 04:00 PM

October 24, 2023 02:20 AM