US Q2 earnings could be some of the most eagerly awaited reports in recent memory. Whilst Q1 earnings were a big deal, they only included a few short weeks of the coronavirus crisis, furthermore January and February were solid months.

The second quarter bore the brunt of the crisis, including lockdown. As a result, bank earnings are expected to be down around 70% compared to the previous year.

Revenue

Revenue is expected to take a bigger hit in Q2 compared to Q1. The Fed dropped interest rates to 0% in March meaning net interest income will be squeezed. M&A and IPO activity also dried up in the quarter amid lockdown restrictions.

On a positive note, mortgage activity could be a positive as refinancing surged as 10 year treasuries dropped to historic lows. Purchase mortgage activity is also showing signs of picking up as states reopen and this could be reflected in Q2 results.

Another plus point is expected to be impressive trading revenue amid high volatility owing to the coronavirus crises. However, there is a good chance that rising trading revenues will be offset by high bad loan provisions.

Bad loans

As companies’ default on borrowing or defer payments bad loans are expected to increase. Provisions for bad loans were eye watering n the first quarter, for some banks the amount that they need to set aside for bad loans has increased further in the second quarter. These bad loan provisions cut directly into profits. With no V-shaped recovery in sight and a long rocky road to recovery bad loans could continue to drag on bank’s profits for some time to come.

Guidance

Most banks withdrew their guidance for the year given the extreme levels of uncertainty. Since then, there has been a lot more data released, and banks will also have more data on their customers as well. The big question is whether banks will provide guidance for the remainder of the year? The outlook is still very uncertain. However, the banks could well have seen an improvement in the last few weeks of the quarter as lock down measure ease and this could give them confidence to provide some type of outlook across the coming quarters.

Chart thoughts

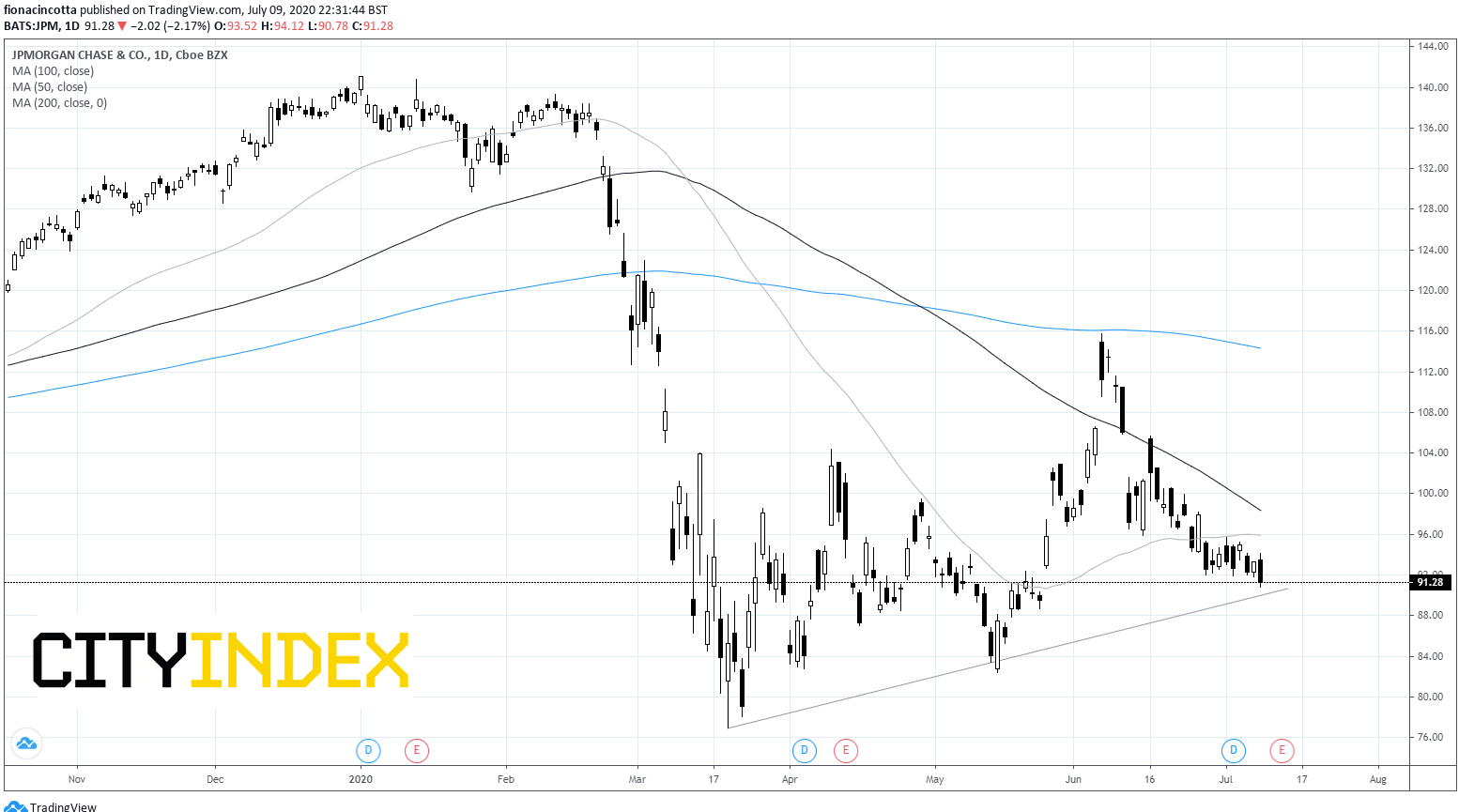

JP Morgan - Reports 14th July

The stock trades -20% YTD, under performing the broader market. Whilst the ascending trendline is just about holding, JP Morgan trades below its 50, 100 & 200 daily moving averages. $90 has proved to be an important level for the stock over the past 6 months. Should $90 hold as support the share price could look to attack $96.00 (50 sma). A break below $90.00 could open the door to support at $88.00.

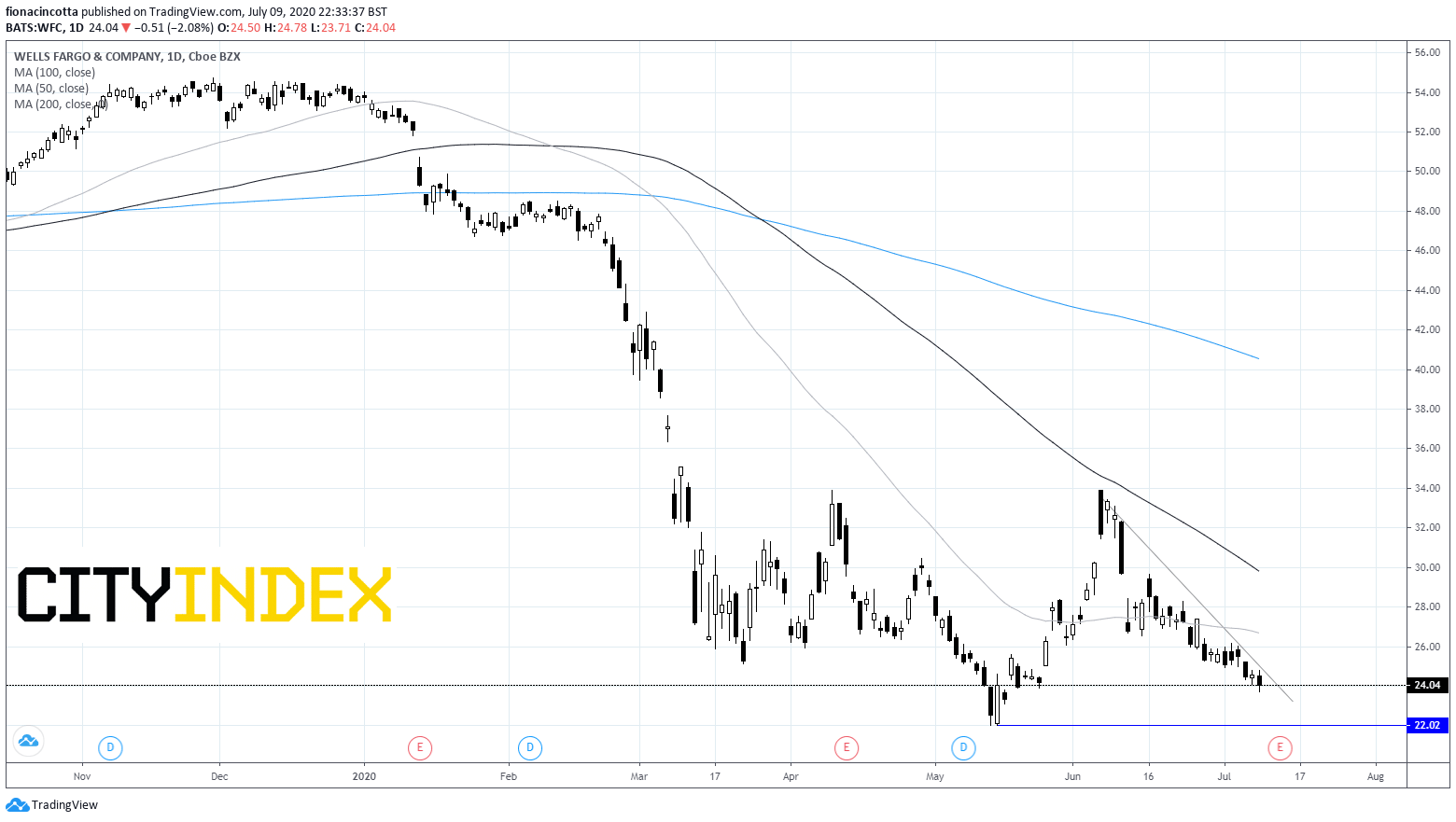

Wells Fargo - Reports 14th July

Wells Fargo is the only bank which has failed to pick up from March lows, instead the stock tanked further towards a May nadir. The stock trades below its 50, 100 &200 daily moving average and below its descending trendline, targeting the May low of $22.00. A break above 50 sma at $27 could see more upside to come.

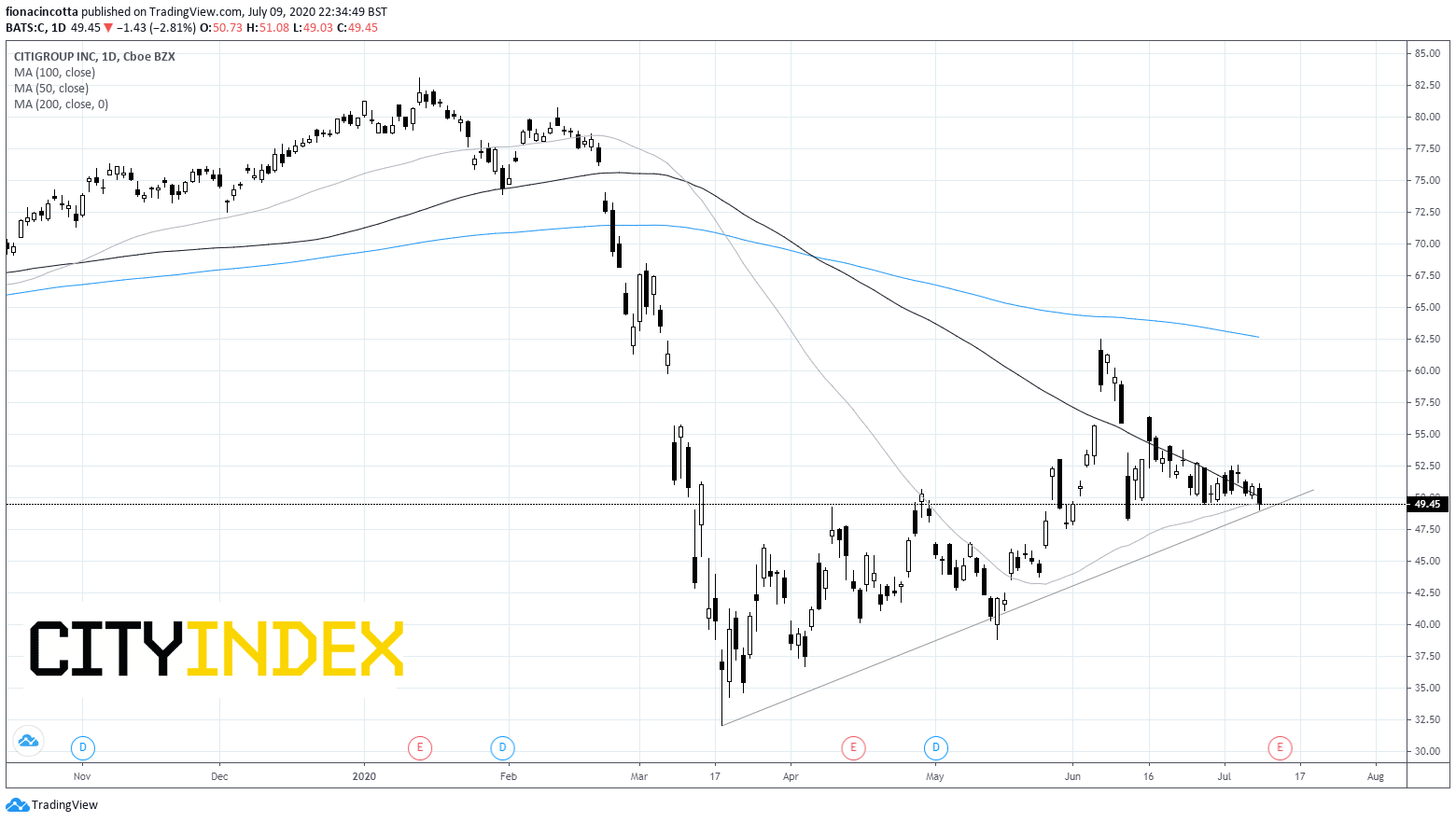

Citigroup - Reports 14th July

Up an impressive 66% from March lows, Citi has so far outperformed its peers in the recovery. However, the stock is still down 30% YTD, significantly more than Goldman Sachs which is now just down -4% YTD.

Citigroup sits at a crucial point $49.5/ $50.00 on the chart, testing its 50 and 100 sma and its ascending trendline.

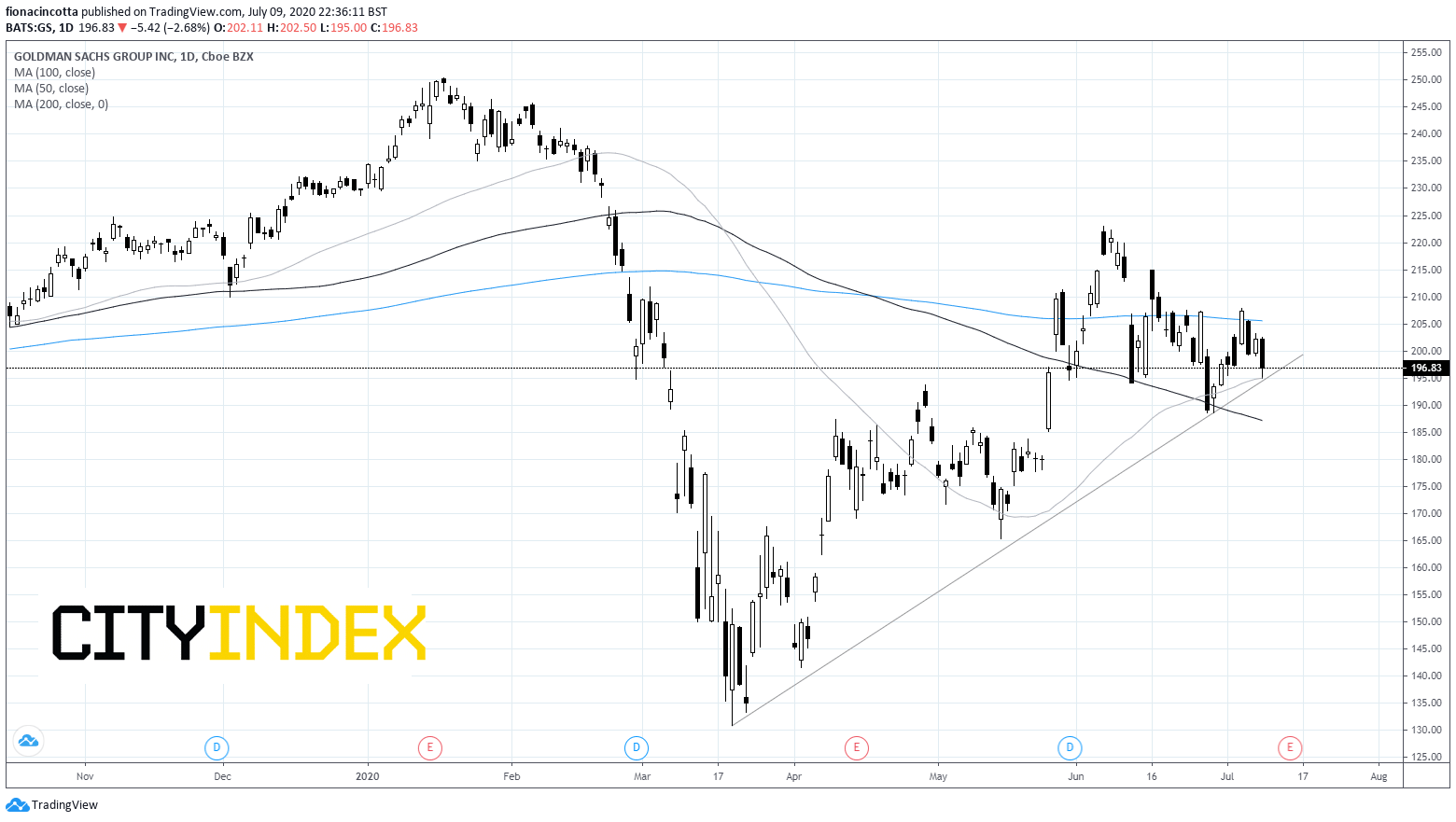

Goldman Sachs - Reports 15th July

Goldman Sachs has seen an impressive run from March lows in the region of 50% from Thursday’s close. The price trades above its 100 daily moving average and the 50 ma is holding, offering support at $294, Thursday’s low. The ascending trendline also holds around that same 194.00 level. A breath through here could negate the current uptrend and open the door to the 100 ma at $187.00.

Should the trend line and 50 ma hold, Goldman’s could look to attach the 200 ma at $205.00 prior to $220.00.

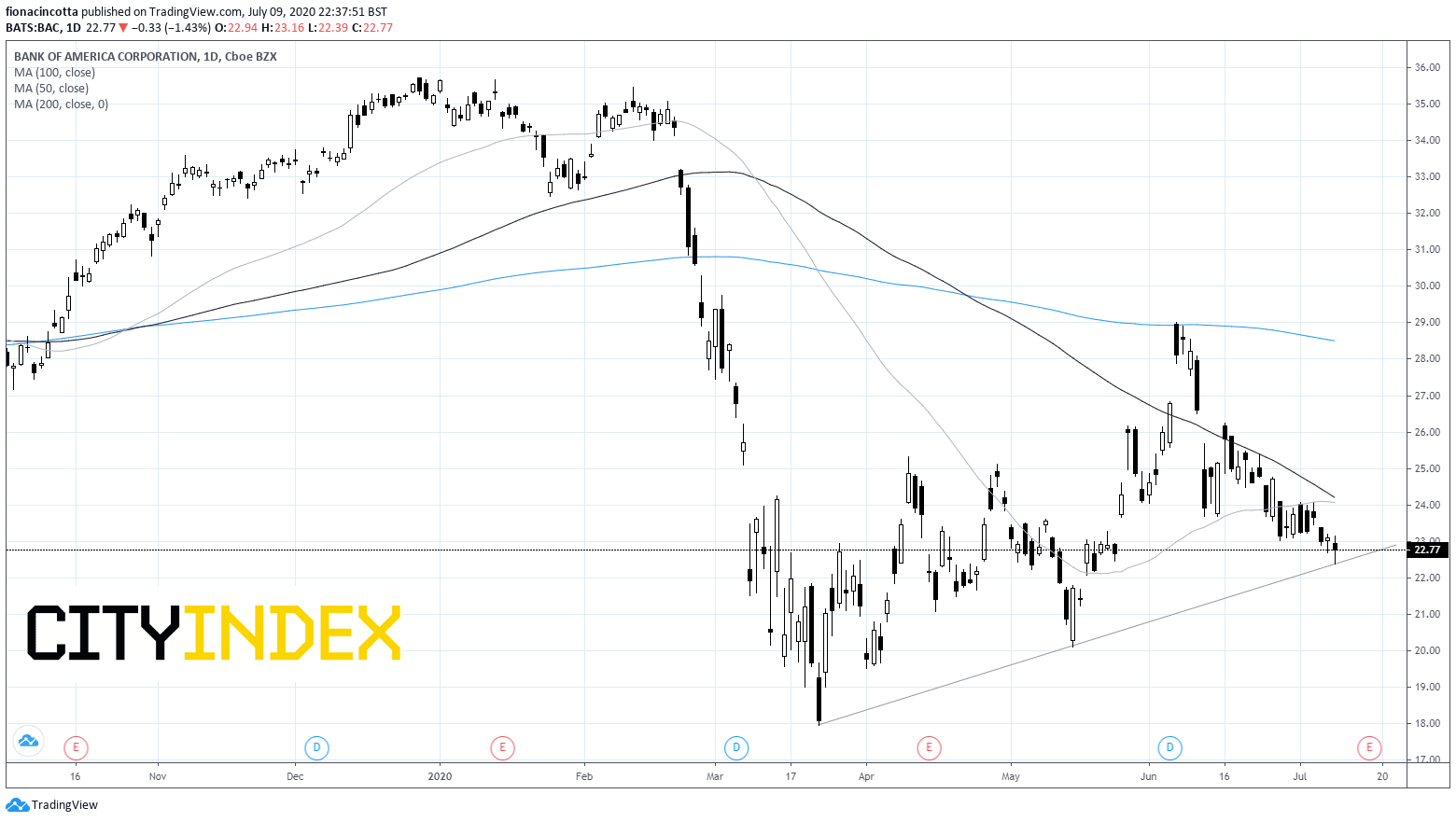

Bank of America - Reports 16th July

BoA trades below it 50, 100 & 200 daily moving average although the rising trend line from the march low is just about holding, for now. A close below trend line support at $22.5 could see more bears jump in and push the share price towards support at $20.00. A break above the 50& 100 sma around $24.00 could see fresh legs on the rally.

Latest market news

Latest Bank Stocks articles

October 10, 2023 09:31 AM

October 6, 2023 02:28 PM

July 17, 2023 04:03 PM

July 11, 2023 02:28 PM