Update who will hike first the BOE or the Fed

We produced a piece of research a few weeks ago that showed how the market expects the Fed to start hiking interest rates ahead of […]

We produced a piece of research a few weeks ago that showed how the market expects the Fed to start hiking interest rates ahead of […]

We produced a piece of research a few weeks ago that showed how the market expects the Fed to start hiking interest rates ahead of the BOE. With this week’s Fed meeting and UK and US GDP reports we thought it was wise to go back over market expectations and see if expectations have shifted in recent days.

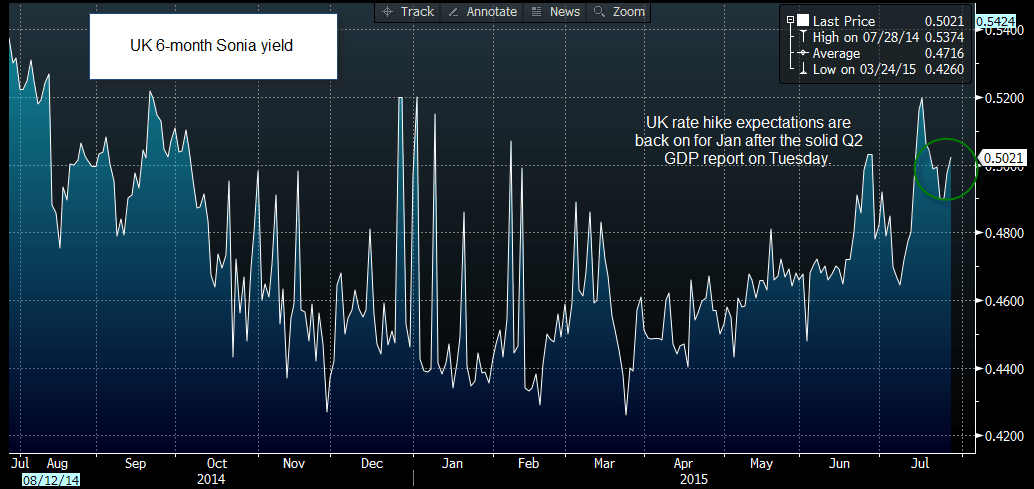

Figure 1 and figure 2 below show current market expectations for the Dec 2015 Fed Funds rate and the 6-month Sonia rate (a good proxy for UK rate expectations), respectively. Right now there is only a month in it, with the market expecting the first hike from the Fed in December, and the BOE only a month behind with its first hike expected in January 2016.

Figure 1:

Source: City Index, Data: Bloomberg

Figure 2:

Source: City Index, Data: Bloomberg

Don’t bank on the Fed moving first…

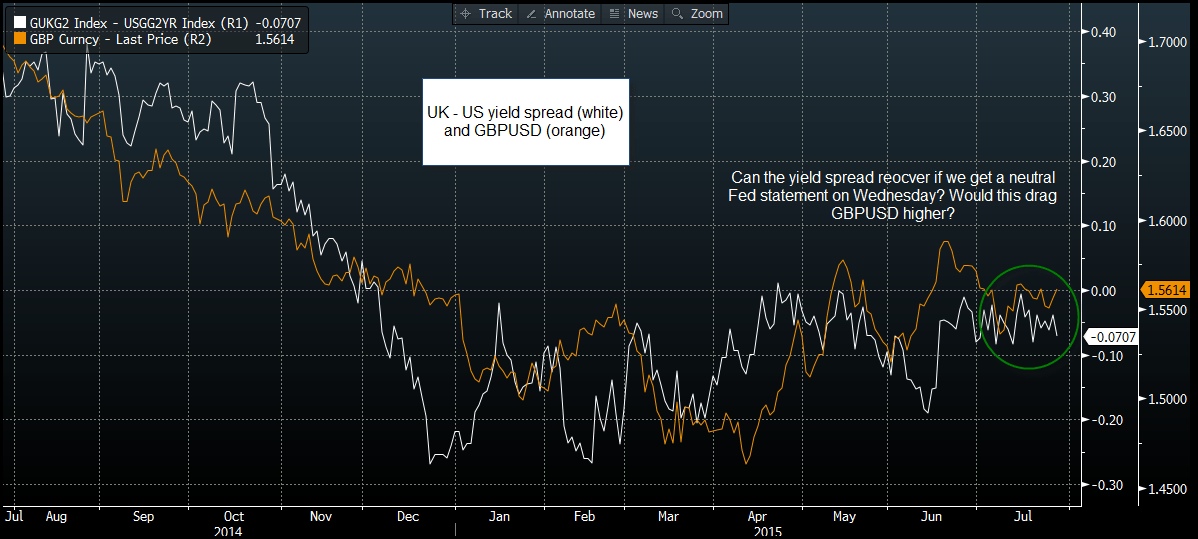

When expectations are this close, any shift in tone from the Fed at this week’s meeting could have major implications for interest rate expectations and, in turn, for the FX market. Figure 3 shows the 2-year US and UK government bond yield spread, which is also considered a good way to detect relative market expectations for the UK and the US. As you can see, US yields are higher than UK yields, however, the UK-US yield spread has recovered and is only -6 basis points, after falling to as low as -20 basis points in June. Thus, if the Fed sticks to a neutral to dovish tone in its post-meeting statement on Wednesday then we could see US yields fall causing this spread to recover, and maybe move back into positive territory. As you can see, the spread moves closely with the GBPUSD rate, so if the spread recovers then we could see GBPUSD gain some traction to the upside.

From a technical perspective, a dovish or neutral Fed statement that might confirm that a September hike is off the cards could trigger some GBPUSD strength. Key resistance lies at: 1.5684 – the high from 15th July, then 1.5881 – the 50% retracement of the July 2014 peak to the April 2015 low.

Figure 3:

Source: City Index, Data: Bloomberg

Takeaway: