UPDATE Royal Mail shares zip higher on cost cuts

Published 19th November at 1025 GMT Royal Mail shares had their best morning in 7 months after it said full-year operating costs would be at least 1% […]

Published 19th November at 1025 GMT Royal Mail shares had their best morning in 7 months after it said full-year operating costs would be at least 1% […]

Published 19th November at 1025 GMT

Royal Mail shares had their best morning in 7 months after it said full-year operating costs would be at least 1% lower.

The company had already said costs would fall 1%, so its addition of “at least” in the reiteration on Thursday, suggested additional cuts.

Given that margins, especially in RMG’s core parcels business, remain challenged—see our article below, published yesterday—perhaps it’s not surprising shareholders have seized on modest cost improvements.

Squeezing out the maximum benefits from the tightest expenses represents Royal Mail’s best hope for the foreseeable future.

Elsewhere in the group, the story is much the same as it’s been for at least a year.

Parcel revenue growth remained at its recent snail’s pace of 1%, with volumes up 4% after +3% in Q1.

Sales from RMG’s Europe-focused General Logistics and Systems business were also outstanding, by coming in flat, again largely due to cost savings.

Earnings were also better than expected on the margin: with operating profit at £348m, about 3% higher than the average market expectation.

However, closer to the bottom line, results were a better reflection of the considerable hurdles RMG still faces.

Adjusted H1 pre-tax profit fell 16% to £240m, missing an already lowered consensus forecast by about £11m.

However, as CEO Moya Greene told reporters on Thursday morning “Everything that can be operationally, we have done … At Christmas, we know it’s our time to shine”.

There is undoubtedly some merit in a seasonally-driven boost for Royal Mail and its stock, and there’s no getting away from the advantages of reduced costs.

However, our article below strongly suggested the stock was likely to correct lower in the near term, and that remains our over-arching view, for the reasons we gave on Wednesday.

Published 18th November

Parcels are heavy

UK Mail Group’s parcels delivery business was partly responsible for its stock tumbling as much as 17% on Wednesday, after it said first-half profit more than halved.

Whilst UKMG is a relative minnow in the fiercely contested consumer mail sector, its results were uncomfortable reading for investors in still dominant Royal Mail, which will release full-year results on Thursday.

Inefficiencies in UKMG’s new automated hub accounted for some of the 56% collapse in pre-tax profit to £4.9m.

But with sector investors sensitised to threats from low-cost operators, European incursions and, of course, Amazon’s ‘Pass my Parcel’ service, launched last year, focus was on margin erosion at UKMG’s parcels unit.

Whilst daily average volumes at the unit rose 9%, helped by a jump in online shopping, operating margins fell to 6.3% from 10.7% in H1 2014.

Parcels account for more than 50% of annual sales at UKMG, which has a stock market value around £200m.

For Royal Mail, whose capitalisation clocks in at £4.5bn, its core UK Parcels, International & Letters unit pulled in 80% of revenues.

Royal Mail in May reported a 1% uplift in package revenues in its last full year, despite relentless pricing competition and margin pressure from its own modernisation drives.

Parcel volumes were up 3%.

But there was little compelling reason to expect a medium-term recovery to earlier run-rate sales growth of 4%-5%, after 2H 2014’s 1% fall.

Nothing much has changed since.

In January, RMG warned that “conditions of overcapacity and too many players chasing traffic (would)…continue to put pressure on prices for the next couple of years”.

With Royal Mail showing little inclination to stop reaching for pricing measures to defend the delivery business, c.6 percentage points of earnings per share probably equates to every 100 basis points of parcels margin.

On that basis, it’s difficult to have high hopes about RMG’s final 2015 earnings, despite parcel revenues rising 2% and volume up another 3% in Q1.

Total quarterly revenue still came in flat because letter volumes fell a sharp 5% and letter revenues slid 4%.

So the main question for investors is whether RMG can at least keep volume and growth at least flat, especially in parcels.

For RMG’s current fiscal 2015/16 year, we struggle to see parcels volume rising more than 2.3%, and expect revenues to fall as much as 2.2%.

That argues for an outcome that’s comes out about flat year-on-year in Thursday’s H1 results.

Additionally, RMG has also raised a flag over its Europe-focused General Logistics and Systems business.

Despite a better-than-expected Q1 performance, the group said it still expected GLS margins to “be impacted by around 50-100 basis points this year”.

On a more positive note, RMG’s comprehensive cost control programme has buttressed operating earnings (AKA, EBIT) and this ought to have continued.

Especially if the pension situation throws up no further negative surprises: a c. £300m shortfall was scheduled to be funded by surplus at least until 2018.

The other main headwind is the outcome of the effective collapse in April of Whistl, RMG’s biggest threat at the time.

A subsidiary of Netherlands-based PostNL, it suspended door-to-door deliveries with thousands of jobs at risk, after talks with a private equity backer over UK expansion failed.

RMG’s relief was short-lived though, when Ofcom said in June it would review competition in the UK mail market.

The regulator has made it clear it still seeks full ‘end-to-end’ competition.

In a preliminary statement in July, the watchdog said: “Royal Mail breached competition law by engaging in conduct that amounted to unlawful discrimination against postal operators competing with Royal Mail in delivery”.

Whistl management bought the firm off its Dutch parent in the same month.

Ofcom will release a fully revised regulatory framework next year.

It’s not clear if it will continue to represent direct competition to RMG in consumer deliveries.

With no comment from Royal Mail so far, its next best opportunity to give its views will be on Thursday.

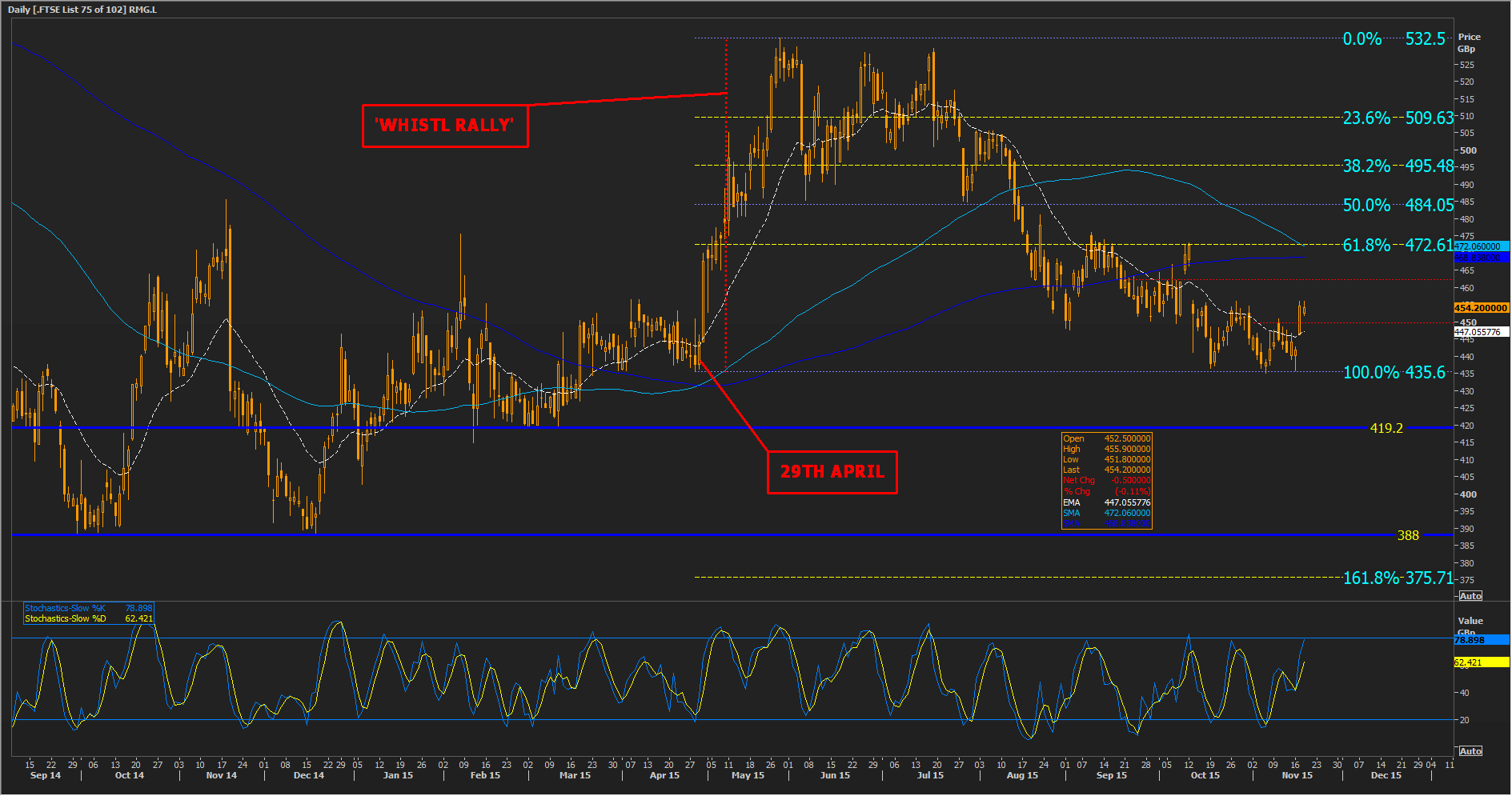

From a technical perspective, Royal Mail shares look to have formed their most promising base for months, bang on the launching point in April, when Whistl’s demise still seemed like a net positive for RMG.

That upswing set new all-time highs at 532p in May and almost again in July.

But latterly, RMG has only managed a maximum of 61.8% of the April-to-May (472.6p) advance.

The top of September’s consolidation zone (462p) might be the limit in the event of a weaker jump.

Further negative news flow would probably set the shares up for a re-test of the aforementioned base at 435p.

In the event of moderate selling, recent resistance-turned support and 21-day exponential moving average between 447p-449p could hold.

However, we know that 5% falls, or more are not uncommon for Royal Mail stock, should its shareholders be dissatisfied.

One of these slides on Thursday could take RMG slightly beyond its new ‘floor’.

If so, 419p would be eyed; it was support in February and March, and 1 penny below Royal Mail’s IPO price.

388p has been this stock’s all-time low, so far.

Please click image to enlarge

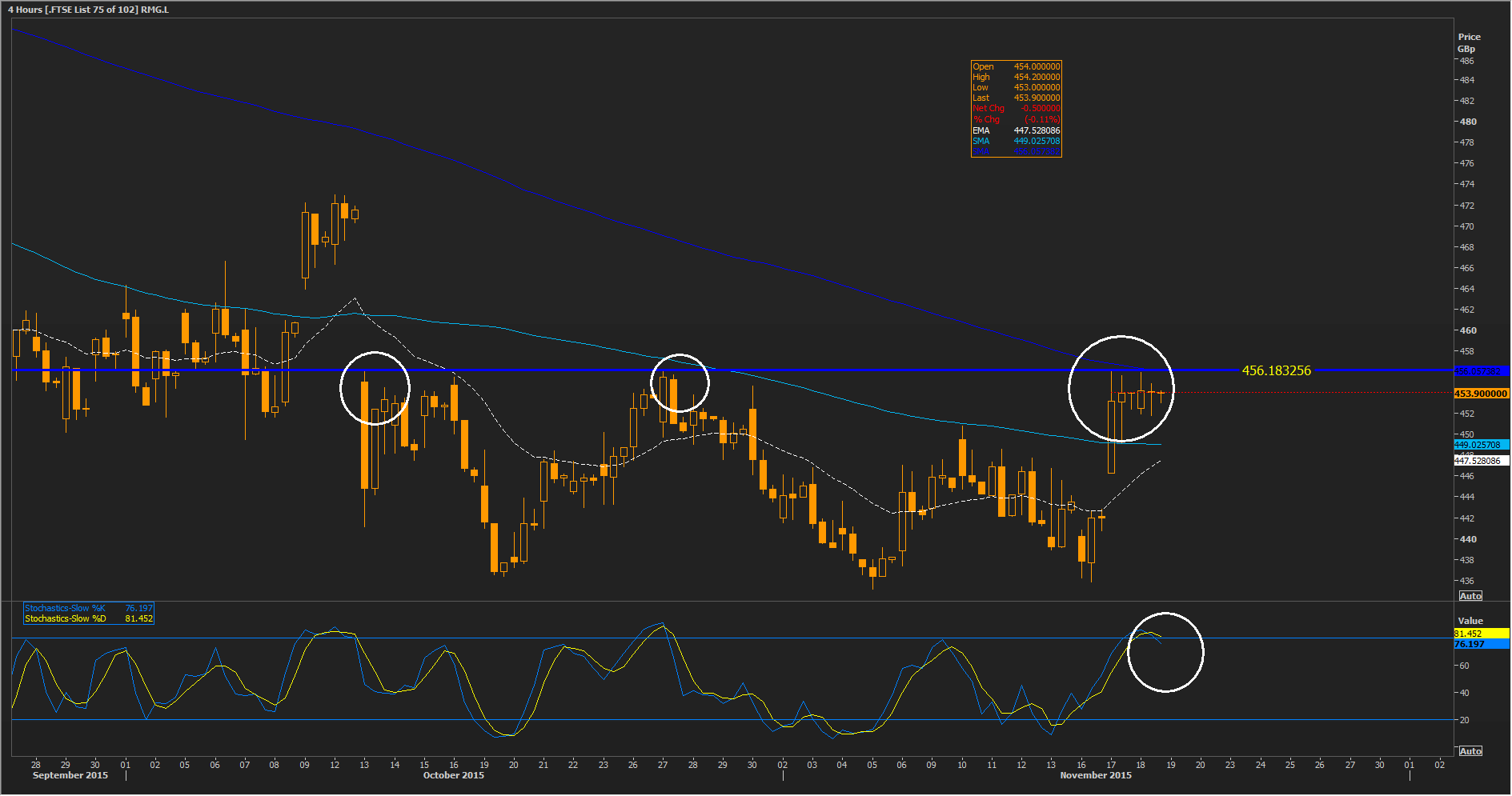

Either way, RMG’s four-hourly chart suggests a near-term slide could be imminent regardless of Thursday’s results.

Proven, persistent resistance at 456p is overhead.

The Slow Stochastic indicator recently inverted whilst overbought.

Please click image to enlarge