UPDATE Facebook rally cools as delayed virtual reality sets in

Updated 1210am GMT 5th November 2015 Facebook shares had a late-night relief rally after it said its closely watched revenues jumped toward their recent 40%-plus growth average […]

Updated 1210am GMT 5th November 2015 Facebook shares had a late-night relief rally after it said its closely watched revenues jumped toward their recent 40%-plus growth average […]

Updated 1210am GMT 5th November 2015

Facebook shares had a late-night relief rally after it said its closely watched revenues jumped toward their recent 40%-plus growth average in Q3.

Facebook stock marked a new all-time high in ‘after-hours’ on Wednesday as sales had been expected to be about 36% higher year-on-year.

That would have been well below Q2’S 39% rise, news of which triggered a sell-off.

Q3 earnings, gauged by the non-GAAP EPS measure Wall St. tends to focus on for tech-company earnings, also beat expectations.

These were $0.57 per share, compared with 53 cents widely expected.

Facebook’s user numbers officially reached and passed an important 1.5 billion milestone in Q3, it confirmed.

But the 1.55 billion Monthly Active Users (MAU) logged also topped expectations.

The total compares to 1.49 billion in the second quarter and Wall Street forecasts of a 1.53 billion tally.

Increasingly higher-value mobile users provided the lion’s share of growth because these rose 23% to 1.39 billion for a total rise in Facebook MAUs of 14%.

There was also a favourable increase in bias towards mobile in FB’s main revenue earner, advertising sales.

Ad rev grew 45.4% to $4.3bn, with mobile ads accounting for 78% of the total versus 66% in the same quarter last year.

Average price per ad was 61% higher in Q3 than the same period in 2014.

Another source of relief for investors was that Facebook’s delta of spending was nowhere near as eye watering as in Q2—this time the rise was ‘just’ 68% to $3.042bn.

(Total costs and expenses rose 82% year-on-year in Q2).

FB officials also confirmed in the post-earnings conference call that one of the goals behind much of the recent soaring spending had been reached.

It said the first consumer version of its GEAR VR virtual reality system would be available in time for this year’s winter holiday season.

However, in one of the few disappointments of the call, FB also noted that its flagship virtual reality product, the Oculus VR headset, would not ship until early in 2016.

Elsewhere on the negative side, the social media giant noted that the strengthening dollar continued to hamper its revenues, whilst total ad impressions declined 10% year-over-year, even if average price per ad rose 61%.

Whilst the broad reaction to these results was favourable there was a clear weakening of sentiment in the after-hours session.

The stock initially soared 5% higher after closing in main market trading a little over 1% higher.

However the extended session rise slipped back to just 2% eventually.

This slackening off may hamper any FB rally in Thursday’s full market.

Late in October, Ireland’s High Court ordered an investigation into Facebook’s transfer of European Union users’ data to the United States.

Whilst Internet user privacy is not a superficial issue, on a bad news scale of 1 to 10, this barely moved the dial for Facebook.

There’s been little materially negative news on the firm at least since the start of its third quarter.

Scarce negative news is important on the eve of Facebook’s third-quarter earnings because it underlines FB’s months-long ‘plain sailing’.

That has perhaps unsurprisingly, been reflected in FB stock.

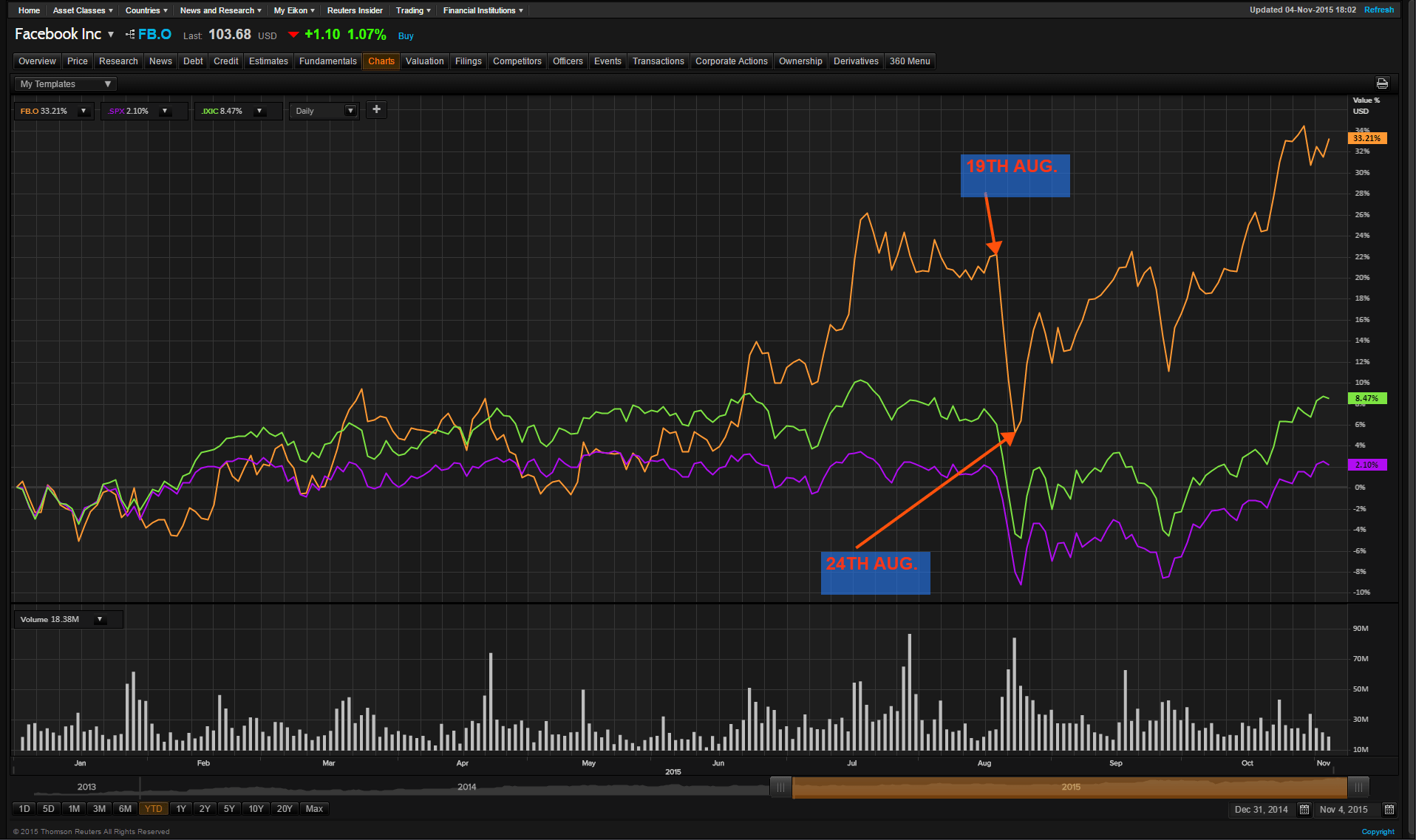

FB lost a good 10 percentage points in the ‘China stock market scare’ spanning mid-to-late August.

But the stock is still sitting on YTD gains of about 33%.

By contrast, the tech-heavy Nasdaq Composite has barely recovered losses.

And the broad S&P 500 is just 2% higher in 2015.

Please click image to enlarge

Key:

Yellow: FB

Green: NASDAQ Composite

Purple: S&P 500.

Despite its above-sector recovery from the market’s late-summer tumble, Facebook may be relatively undervalued against other US Internet Giants.

FB’s forward price/earnings ratio is at 39 times 2016 earnings.

Struggling Twitter remains higher despite being pared back to 51 times, and LinkedIn is rated at 70 times.

The comparison could provide a fundamental underpinning for a strong Facebook rally if its earnings are well-received.

Beneficent sentiment has been buoyed by generally favourable analyst coverage: 48 out of 52 analysts covering the stock had ‘buy’ or ‘strong buy’ recommendations at last count, according to Thomson Reuters.

This helped FB shares to their latest all-time high just days ago, on Thursday 29th October.

A binary view therefore makes particular sense ahead of FB’s Q3 results later on Wednesday with a view to market expectations.

Especially given the 5% fall by FB stock on the night off its Q2 results that failed to impress, even though most metrics beat expectations.

Option trade pricing on Facebook stock on Wednesday suggests higher-than-normal pre-earnings volatility.

Bearish and bullish bets are fairly balanced.

The cost of ‘at the money’ straddles suggests traders see a 6.1% move in either direction by Friday.

FB stock has tended to move 4.4%, on average, on the day after its last eight earnings reports.

The negative share price reaction to FB’s last set of earnings suggests investors still need to come to terms with the fact that Facebook faces similar challenges to other groups that are exposed to softening global advertising and marketing trends.

The problem is investors have become used to quarterly revenue growth well above 40% year-on-year.

But FB’s sales growth during the last few quarters suggests that era may have passed.

The other major input to sentiment, monthly active user (MAU), may also need a recalibrated norm.

With FB logging its 1.5 billionth user in third quarter, quarterly rises of more than 12%-13% seen over the last few years will be less common.

If revenue and MAU results are not liked but deemed fair enough, FB’s rampant penchant for spending might still tip the balance for its stock.

FB has warned of a 2015 splurge that’s as much as 60% higher on the year, as it tools up its fastest growing apps, Instagram, Messenger and WhatsApp, with state-of-the-art advertising and data platforms and creates new virtual reality frontiers with Occulus Rift.

Expenses rose 82% in Q2 alone.

The Street seems to be expecting total spending to have risen about 36% in Q3—our assessment suggests 30%.

Here are up-to-the-minute financial forecasts according to Thomson Reuters data.

It’s worth pointing out that expectations appear to have been upgraded in the last few days.

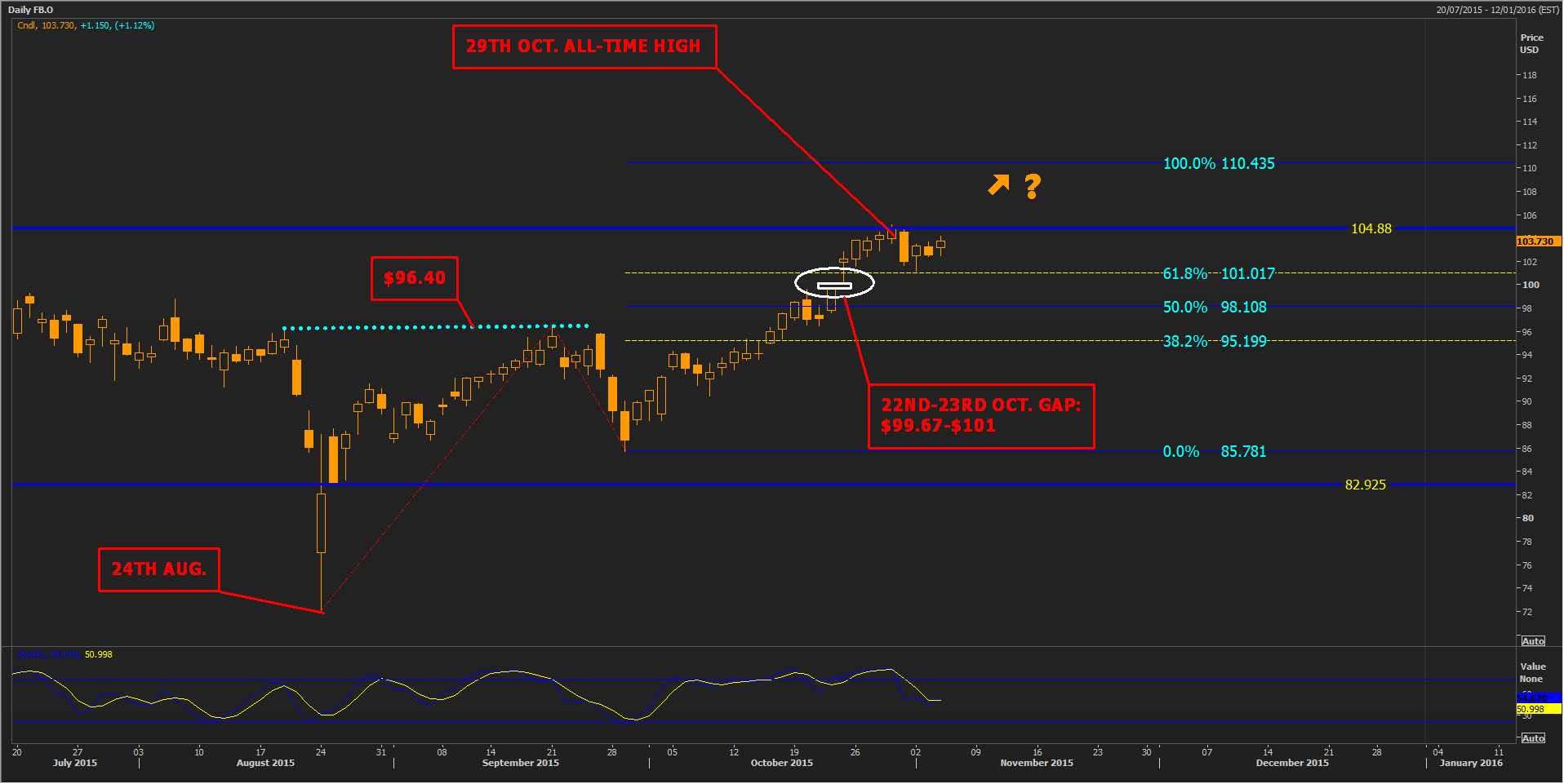

With that said, we note FB stock began to wilt from all-time highs this week.

It appears supported by an important retracement mark (61.8%: $101) of its latest up-leg since the end of September.

The 100% extension based on FB’s bounce since 24th August would be reached at $110–a potential target in the event of a sudden rise.

Should earnings, advertising revenues, or user growth disappoint, and support break, attention might shift to a small gap on 22nd-23rd October.

Upset sentiment could push the shares quickly into the space between $99.67 and $101.91, representing unfulfilled orders during a rush to buy on 23rd October.

Former resistance at $96 could provide support lower down, but a descent towards $85 might have better odds.

Please click image to enlarge

(This article will be updated after Facebook’s Q3 results are released.)