UPDATE Apple shares in a bind ahead of earnings

Updated 1610 GMT, 27th October 2015 PART II Shares signal balanced chances for a rally tonight Apple shares bruised by disappointing results, China […]

Updated 1610 GMT, 27th October 2015 PART II Shares signal balanced chances for a rally tonight Apple shares bruised by disappointing results, China […]

Updated 1610 GMT, 27th October 2015

Apple’s shares edged higher on Tuesday as the market weighed bearish and bullish chances ahead of its hotly anticipated earnings.

The stock closed well ‘in character’ for the year on Monday night though—with a slide of more than 3%, setting losses since late April at 14%.

As noted in the first half of this article below (posted on Monday) AAPL is underperforming the broader market, after failing to meet tough market expectations in Q3.

The market is no less demanding going into Apple’s Q4, and we detail what investors want in Part 1.

In this update, we stake out the main watch points for the stock.

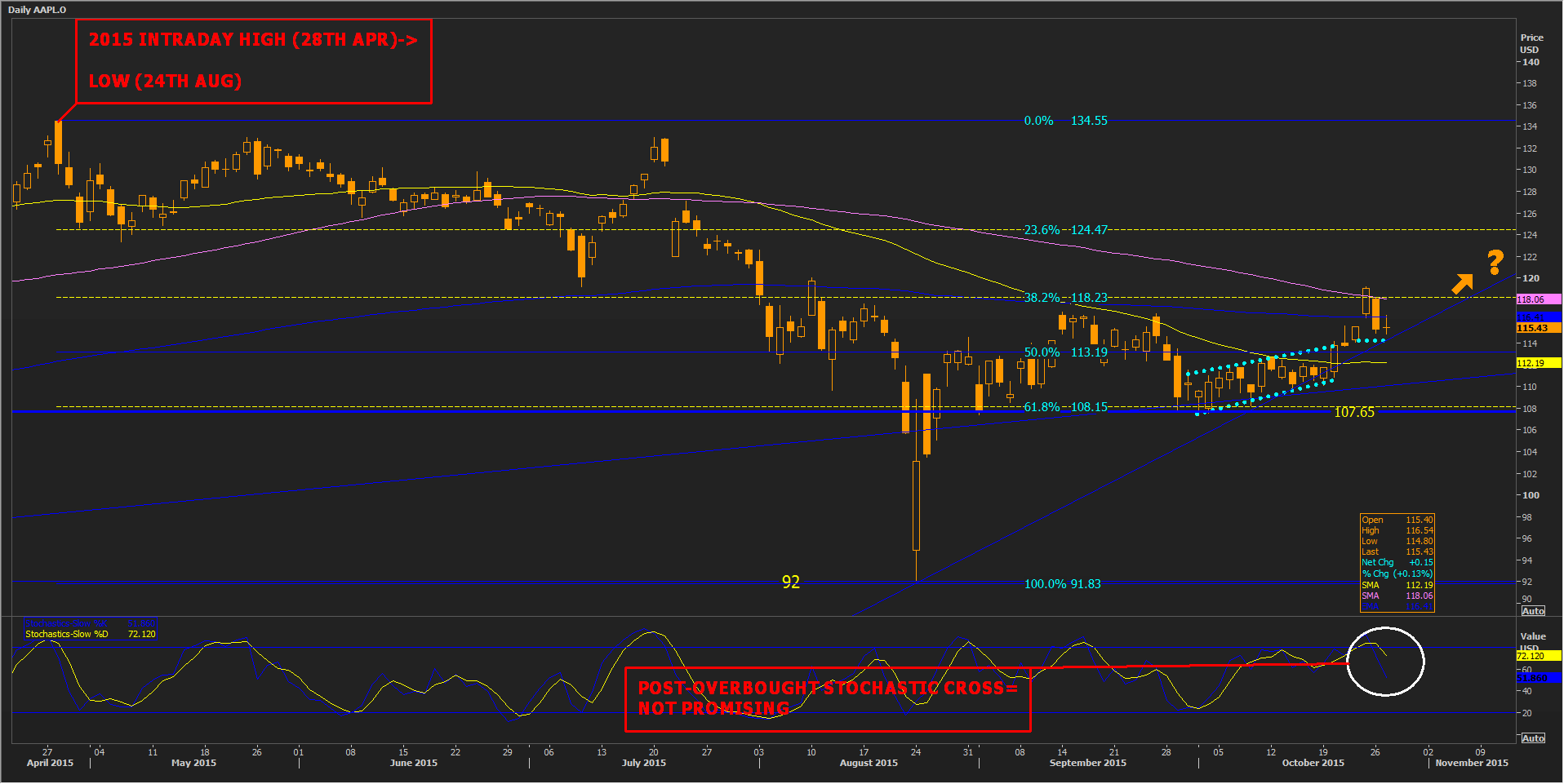

Like the largest constituents of benchmarks like DJIA and S&P 500, Apple had its clearest bounce of the year in late August.

It was a reflex from a sharp global sell-off triggered in China’s stock market.

In a three week advance, Apple shares retraced 38.2% of their fall from intraday highs marked in April.

However, that closely watched interval, combined with the 100-day moving average (MA) then forced a short-term retreat.

The stock was waiting beneath its 200-day MA—widely seen as among the most important—at online time.

An imperfect, yet potentially bearish flag pattern between 1st and 20th October might also be showing a delayed reaction.

However, even if valid, its effect will likely be weak given the lack of a proper ‘flagpole’.

Still, failure to retake ground above the 200-DMA (AAPL fell below it in August) would argue against a near-term revival of its bull case.

An inverted Slow Stochastic momentum gauge which was recently overbought doesn’t augur well either.

Should the retracement hold on to recent lows—say c. $115 from last Thursday, the nearer-term price outlook could still be quite good, though sooner or later that 200-day challenge has to be faced.

If skimped—perhaps in the event that tonight’s earnings are poorly-received, expect a quick fill of the above consolidation zone.

Eyes will then turn to proven support around $107, just 50 cents from the major 61.8% $108.15.

A steep collapse back to year lows is the main risk after that.

If, on the other hand, Apple turns back into SuperApple™ tonight its stock could certainly break all of the barriers overhead.

A resumed long-term uptrend could be the prize.

Please click image to enlarge

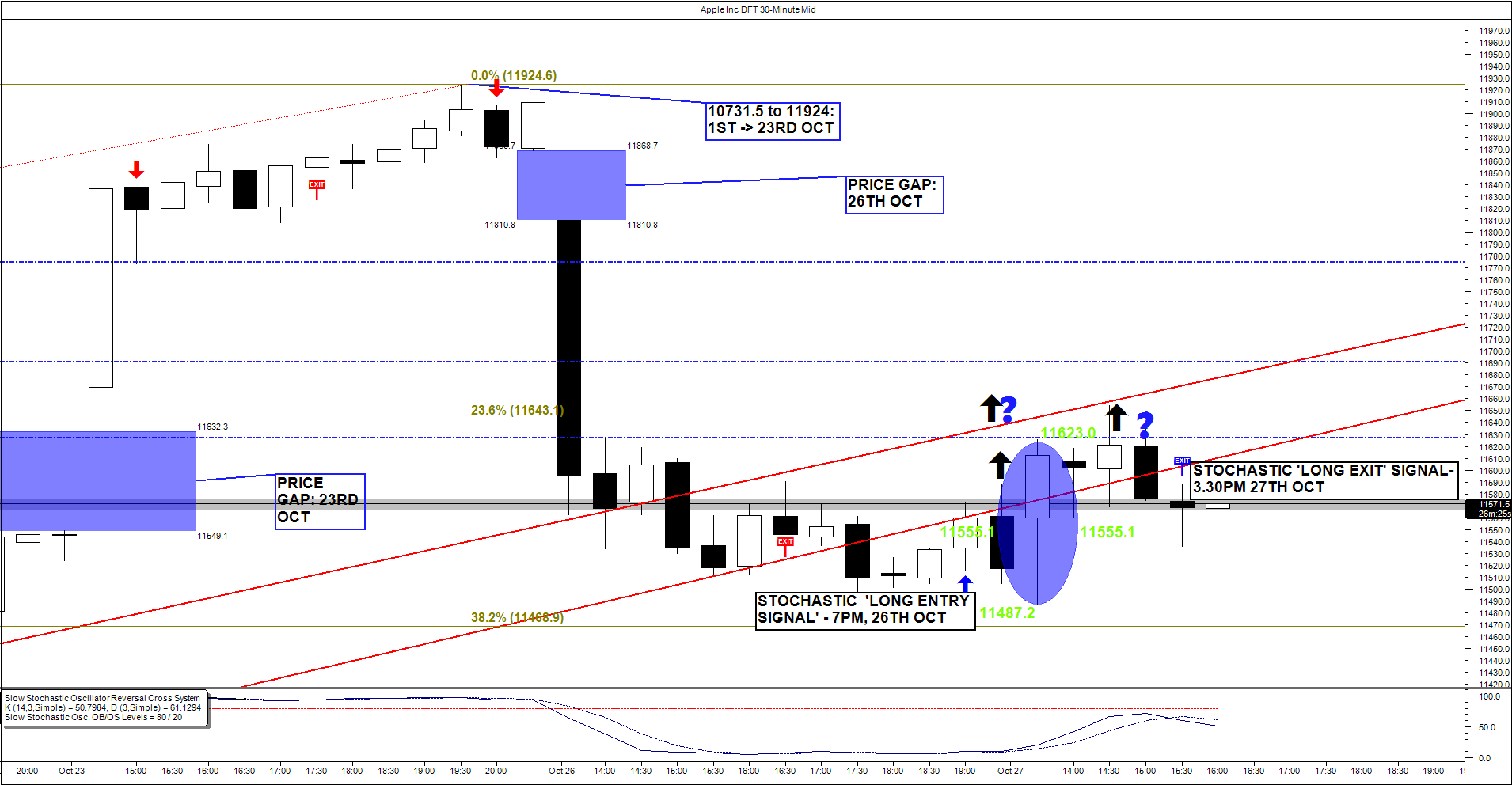

However, as this update was about to be published, short-term trading of Apple Daily Funded Trade, by City Index clients, seemed much less optimistic.

Here, Apple struggled to re-occupy a tapering channel formed by short-term uptrends from earlier in October.

It was probably no coincidence that the area offering most resistance corresponded with a gap that opened by a disorderly jump between 22nd and 23rd October: 11549-11632.5.

Formidable engulfment from Monday’s sell-off is also a major challenge.

That long candle is also straddled by prior resistances around 11628 and 11775.

A short-term rally also failed today, well sign-posted by the attached ‘Slow Stochastic Oscillator Reversal Cross System’.

Based on the momentum gauge of the same time, this flashed potential ‘long’ and ‘short’ signals.

A ‘long entry signal from Monday night was negated without great reward on Tuesday afternoon.

However, stochastic lines (sub-chart) were not classically bearish as this article went online given that they were well beneath the ‘oversold’ boundary.

Still, Apple’s DFT really needs to power through its current blockages to have any chance of rallying significantly.

Earnings the market deems to be strong would be key.

Earnings that disappoint the market again could easily risk a return to Tuesday’s lows (blue ellipse).

And that would probably be just for starters.

Please click image to enlarge

Published 26th October 2015

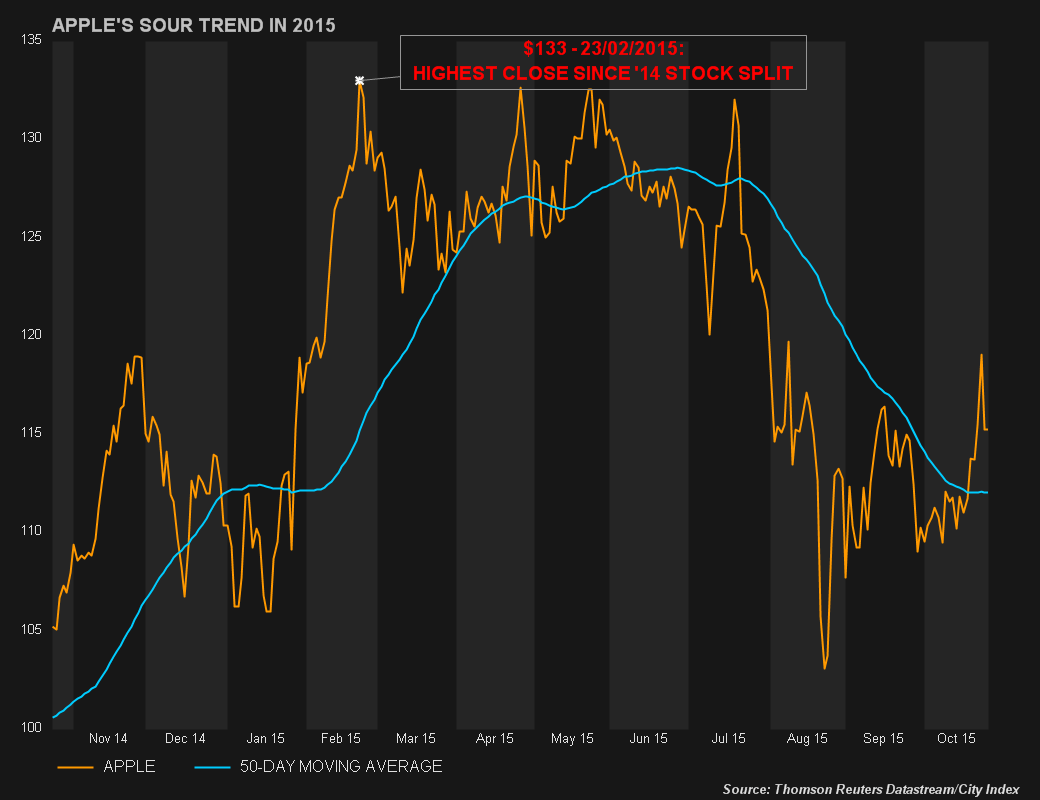

Apple shares have had a groundhog quarter.

Watchers of its stock will know its losing streak since February’s all-time highs.

Its failure to trade sustainably above its 50-day moving average since then, added weight to bearish views, even if that boundary’s importance is ordinarily debateable.

Please click image to enlarge

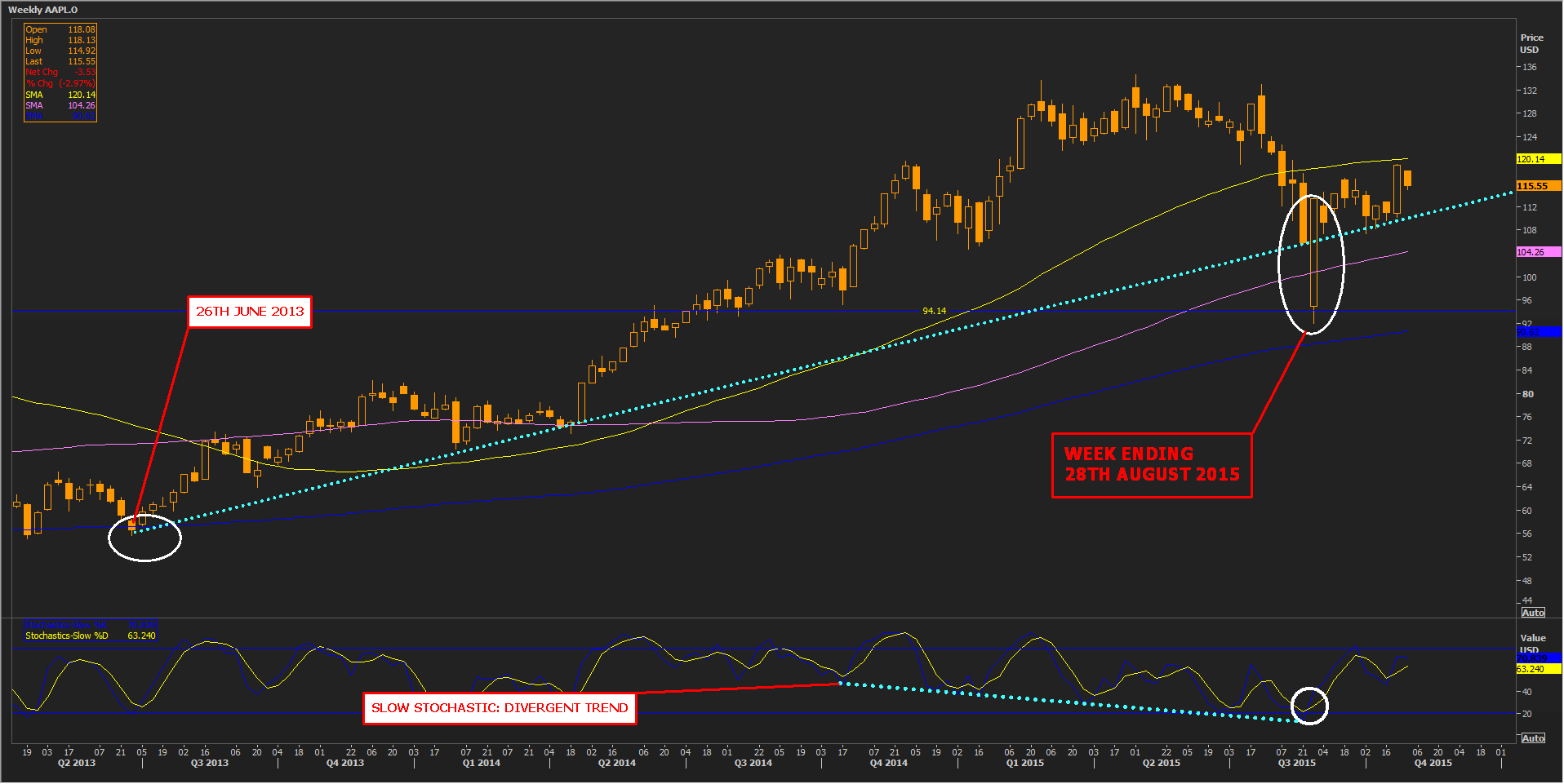

Late in the summer, the shares even fell, for the first time, beneath a formidable trend that dates back to June 2013, albeit when all markets were tanking.

The shares have rebounded 28% from August’s 2015 lows, but they’re underperforming the S&P 500’s 0.2% rise over the last three months with a 6% fall.

WEEKLY CHART

Please click image to enlarge

The obvious trigger for the souring of Apple’s uptrend—which had given the stock a preternatural halo for decades—was weaker-than-expected iPhone sales in the quarter ending in June.

That however was but a reflection of a much more familiar Apple trifle: ‘The overachiever’s bind’.

Apple’s run of increasingly lofty records keeps creating ever more challenging hurdles.

Cupertino California’s most famous resident still shifted 47.5 million handsets in the three months to the end of June—up 35%— but analysts were expecting 48.8 million.

Not to mention that it beat on the top and bottom line.

The problem was that Apple had set a run of all-but fantastic financial and revenue peaks in 2014.

All this–combined with the financial world’s apparent shock awakening this year to China’s decelerating economy–offered enough reasons for many shareholders to sell.

So the bigger question for AAPL on the eve of its fourth-quarter results is not whether it sold a huge amount of products and made an astounding amount of money, but whether the market will be satisfied, even if—once again—it does.

On that basis, Apple probably needs to pull one of its increasingly unicorn-like rabbits out of the hat on Tuesday night.

Its 12th straight quarter of above-forecast earnings may not suffice.

A summary of the market’s Q4 financial expectations:

Apple’s statistical record suggests all the above numbers are likely to be beaten.

If in the event they’re not, there’ll be an easy-to-imagine impact on the stock.

Apple’s product results will also be crucial—perhaps more important than in any of its quarters for years.

We fast-forward to the all-important iPhone, whilst remembering that Q4 tends to be a relatively slow one for all consumer electronics sales.

Once again, in line with the usual Apple pattern, consensus breaks down when we get to product data.

The giant consumer tech-to-fashion-to-who-knows-what-next-company did say in September iPhone 6S/6S Plus orders beat the 10 million ‘1st-weekend’ record set by 6/6 Plus.

At the very least then, total iPhones sold in Q4 are unlikely to slip below the 47.5 million from Q3.

Even if they match or beat that target though, sales would still have decelerated from the record 74.5 million rung through in the December 2014 quarter.

However, the market might still go berserk, in a ‘good’ way, if new iPhone users beat market hopes of around 17 million.

That would represent a bounce from less than 14 million new iPhone users in the June quarter—the weakest count of new iPhone devotees since September 2014.

It has to be said there are some high-profile pessimists in the market on handset sales for the last quarter—they loop their forecasts back to China.

It may be, after all, that Q4 is the one in which pessimistic Apple forecasts have the best chance, for a while, of being right.

Collective consciousness on other Apple products is even more opaque.

Wall St. and Main St. curiosity is heightened either way, regardless of the fact that Apple is still unlikely to break out exact numbers for Watch, Pay, Music, or refreshed TV.

For the next most-obsessed-over item, Watch, sales-channel evidence suggests earlier market doubts may have been closer to the mark than Apple would like.

Even so, persistent assessments around the 5,000-sales-per-day-mark, equating to about 1.8 million per year—would still place Watch in the Top 3 best-selling smartwatches around.

Even if that would be below the most optimistic forecasts from earlier in the year.

Importantly, meaningful EBIT returns, net of development and marketing costs, would remain out of reach if Watch isn’t selling almost double the amount currently reported.

CEO Tim Cook’s take on Watch, if he offers one at all, is likely to be among the highlights of the post-earnings analysts’ call on Tuesday night.

More concretely, total iPad sales can be expected to keep pace with, or slightly beat, 10.9 million seen in Q3.

If not they will be another drag on Apple shares.

And the Mac is likely to continue its renaissance with sales above 5.6 million