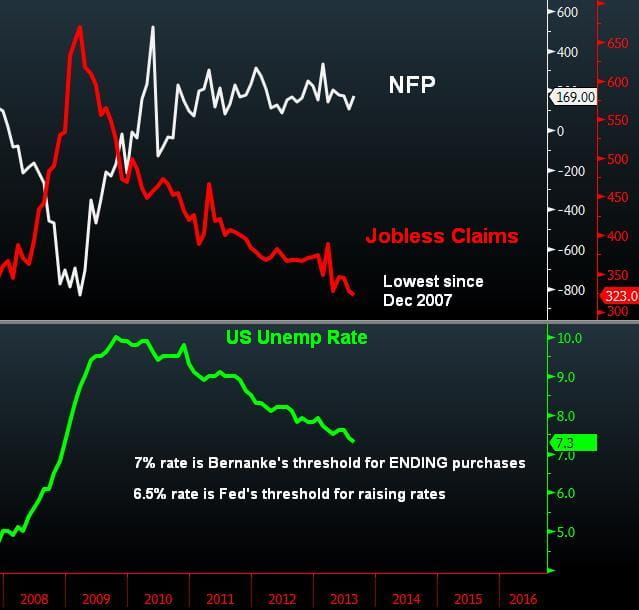

Unemployment Nears Bernanke 8217 s 7

Unemployment approaches the 7% level deemed by Fed Chairman Bernanke appropriate for ending monthly asset purchases, therefore the latest 7.3% suggests a tapering must start […]

Unemployment approaches the 7% level deemed by Fed Chairman Bernanke appropriate for ending monthly asset purchases, therefore the latest 7.3% suggests a tapering must start […]

Unemployment approaches the 7% level deemed by Fed Chairman Bernanke appropriate for ending monthly asset purchases, therefore the latest 7.3% suggests a tapering must start this month. The Fed has little time left. It is more appropriate to scale down purchases at smaller increments of $10 bn every quarter than to deliver a single $30 bn or $40 bn blow to the bond market.

NFP rose to 169K in August vs. an expected 180K, following a downward July revision to 104K from 162K. Although June and July revisions produced a total decline of 74K jobs, September NFP rose well above the 3-month average of 148K. The unemployment rate dropped to 7.3% from 7.4%, reaching its lowest since Dec 2008.

Unwarranted Bond & FX Reaction

The market reaction to sell USD and drag down bond yields proved a typical case of exaggeration as traders focused on the downward revisions, the decline in NFP away from the 200K whisper number and the decline in the labour participation to fresh 35-year lows at 63.2%.

And since when do traders trigger 100-pip declines in USDJPY and 100-pip jumps in GBPUSD in a matter of seconds based on the participation rate when the unemployment rate unexpectedly fell to 7.3%, nearing 5-year lows?

Let’s not forget that average hourly earnings rose 2.2% y/y reaching their highest level since July 2011. Meanwhile, jobless claims are at 5 ½ year lows below 330K while ISM manufacturing and services are at 2-year highs and 8-year highs respectively. This may not be “substantial progress” but sufficient to start tapering this month.

Bernanke: 7% Unemployment ==> “Substantial Progress”

Although 6.5% unemployment rate is the threshold level for a hike in rates, 7% unemployment is the rate deemed appropriate by the Fed Chairman for terminating asset purchases. In the words of Chairman Bernanke in June: “We look at participation, payrolls, a variety of other data. But the 7% unemployment rate is indicative of the kind of progress we’d like to make in order to say we’ve reached substantial progress.” “In this scenario when asset purchases ultimately come to an end the unemployment rate would likely be in the vicinity of 7%…”

War & USD Impact