Uneasy calm over UK shares despite sterling anxiety

The pound, like the polls is balanced on a knife edge On our watch list: property companies, insurers, retailers, telecoms and utilities, banks […]

The pound, like the polls is balanced on a knife edge On our watch list: property companies, insurers, retailers, telecoms and utilities, banks […]

Regardless of whether you’re a ‘yes’ or a ‘no’ on the question of EU membership, in our view, the financial hit to the UK should be equity investors’ central concern, as a severe shaking and stirring for sterling emerges as the single clearest outcome, ahead of the vote, and potentially after.

Most polls continue to show voters are evenly split, including one by YouGov on Thursday, which had 39% on either side, though a ComRes phone survey for the Sun newspaper on Monday gave the ‘Ins’ a 7-point lead vs. 38% backing Brexit.

That was in line with most telephone polls showing an ‘in’ response, with more people willing to say they’d vote ‘out’ online.

The notorious failure of polls to predict the strong Conservative win in the 2015 General Election combined with ambiguous readings ahead of the Referendum obviously offer little relief for the pound, and it remained on precarious ground on Monday.

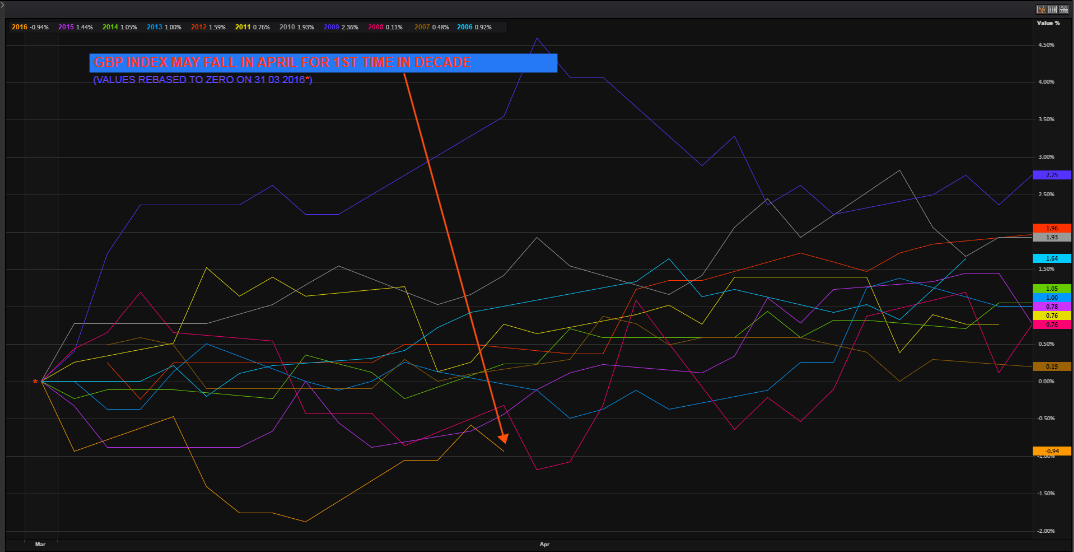

Either way, it was already looking like sterling was on course to break a consistent run of gains in April for at least a decade.

Figure 1 – Sterling Currency Index in April: 2006-2016

So, whilst definitive links to a destabilised pound and financial and economic impact remain arguable, we think it’s worth taking a look at what we expect to be the main stock market stress points, plus some ideas on how to get on the right side of them.

On the other hand, it’s worth remembering that whilst implied volatility (in currency options) remains at its highest since 2010, equity markets have been quite orderly since the first two months of the year. We should therefore be wary of overestimating market concern, regardless of the headlines.

That said, the pound remains a good place to start. It has regained some poise after lows at the beginning of the month, but the Bank of England’s trade weighted index is still 7% weaker in the year to date. There are several other major macroeconomic influences buffeting world currencies right now, but it’s difficult to dismiss nerves and uncertainty in the run-up to the referendum. In turn, this has kept risks to corporate sectors most exposed to the pound and ‘Brexit’ fallout in focus.

Our current assessment is below, though bear in mind that market trends can change quickly.

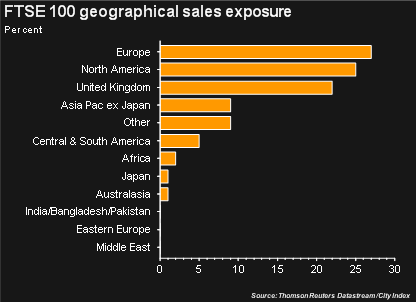

Another point worth remembering here, is that the largest UK-listed companies make a greater percentage of revenues overseas. That implies lower exposure to sterling, and more sales in Europe. (See below.)

Figure 2 – FTSE 100 company revenues by region

But there is another twist at the top end of the market: for industries perceived to be most closely tied to Britain, or dependent on Europe, size hasn’t been an advantage.

The FTSE 100’s biggest 20 losers over the last three months include three of the largest banks, two highly rated property stocks, Europe-focused easyJet, and Anglo-German tourism giant TUI.

The worst performer was the UK’s biggest clothing retailer Next. Dixons Carphone, another large ‘consumer discretionary’ name with a significant European presence, also appears.

| COMPANY | 3-MONTH % CHANGE |

| NEXT | -18.0586 |

| BERKELEY | -16.9095 |

| ASHTEAD | -14.1052 |

| BARCLAYS | -10.4715 |

| WORLDPAY | -10.1357 |

| BARRATT DEVELOPMENT | -9.8852 |

| RBS | -8.6087 |

| CAPITA | -8.3626 |

| TUI | -8.2834 |

| EASYJET | -8.1823 |

| ITV | -7.5727 |

| DIXONS CARPHONE | -7.3964 |

| HSBC HOLDINGS | -6.6186 |

| AVIVA | -5.6358 |

| STANDARD LIFE | -5.3969 |

| WHITBREAD | -3.5384 |

| TAYLOR WIMPEY | -3.3369 |

| SKY | -2.9069 |

| INMARSAT | -2.7884 |

Figure 3 – the weakest 20 FTSE 100 shares in percentage terms; 3 months to date

And underlining the likelihood that financial and political risks are a potent mix (think post-Brexit trade negotiations) a short trade on a basket of UK bank stocks opened in January, has outperformed buys of pharma, tobacco, and even oil & gas stocks, according to Thomson Reuters.

On the other side of the market, sectors perceived as likely to benefit from ‘Brexit fear’ have been much less clear-cut. A surge of demand for mining and oil stocks as mineral prices rebound has partially obscured the wider picture.

Looking more broadly, a 3-month view of London’s top 350 shares largely matches supposed pre-Referendum sentiment, mining and oil stocks aside.

BEST AND WORST FTSE 350 SECTOR’S OVER 3 MONTHS

Figure 4 – FTSE 350 sectoral performance: 3 months to 11th April 2016

But whilst our first few graphics at least leave open the possibility that a weaker pound might boost large exporters, consistent trade deficits since 1998—including record imbalances with Europe this year—remind us that most British companies—small-to-medium-sized enterprises (SMEs)—may not have the option of exporting new challenges away.

That’s quite apart from a potential hit to SMEs from a weaker pound, their main revenue currency, as shown below.

Figure 5 – FTSE SmallCap Index company revenues by region

Here again though, the evidence that small-cap stocks might underperform on Brexit fear is pretty ambivalent, so far.

The FTSE 100 has done better than a batch of small cap indices in the year to date, but not much.

Figure 6 – FTSE indices rebased to zero from January to date:

SmallCap, Fledgling, AIM, FTSE All Share, FTSE 330, FTSE 100

We’ll look at possible risks and opportunities in UK stocks in more detail over the next six weeks, so please check back frequently for updates.