UKretail sales cap week full of poor UK data

The pound was dropping quite noticeably this morning even before the publication of the January UK retail sales data. It was clear someone knew something […]

The pound was dropping quite noticeably this morning even before the publication of the January UK retail sales data. It was clear someone knew something […]

The pound was dropping quite noticeably this morning even before the publication of the January UK retail sales data. It was clear someone knew something because the numbers were indeed very weak. According to the ONS, retail sales fell a further 0.3% in January after tumbling 1.9% the month before. On a year-over-year basis, sales eased to +1.5% compared to expectations of print of +3.4%. Economists were clearly left scratching their heads. Some concluded that Britain’s surprisingly strong consumer spending since the Brexit vote has come to an abrupt end, in part because of rising inflation. Others said that the slowing consumer spending and weaker wages growth could see the Bank of England hold rates unchanged this year despite some hawkish commentary of late by some MPC members with regards to having limited tolerance of higher inflation. But as the pound was already lower on day – and the week, after disappointing inflation and wages data in mid-week – we didn’t see any significant continuation in the selling pressure, although the currency was holding near its lows at the time of this writing.

The pound could recover despite soft data

But with all the news out of the way, could the pound now stage a recovery as the sellers take profit? I think this a strong possibility, particularly as there are no economic pointers scheduled from the US either this afternoon or on Monday. Apart from this week, economic numbers out of the UK have been strong and although things may start to turn sour again, I am of the view that the worst is behind us. I therefore still think that the cable is mostly likely heading higher in the weeks and months to come than fall below 1.20 again. The bank of England is unlikely to cut interest rates again, while the potential rate rises from the Fed this year are possibly already priced in.

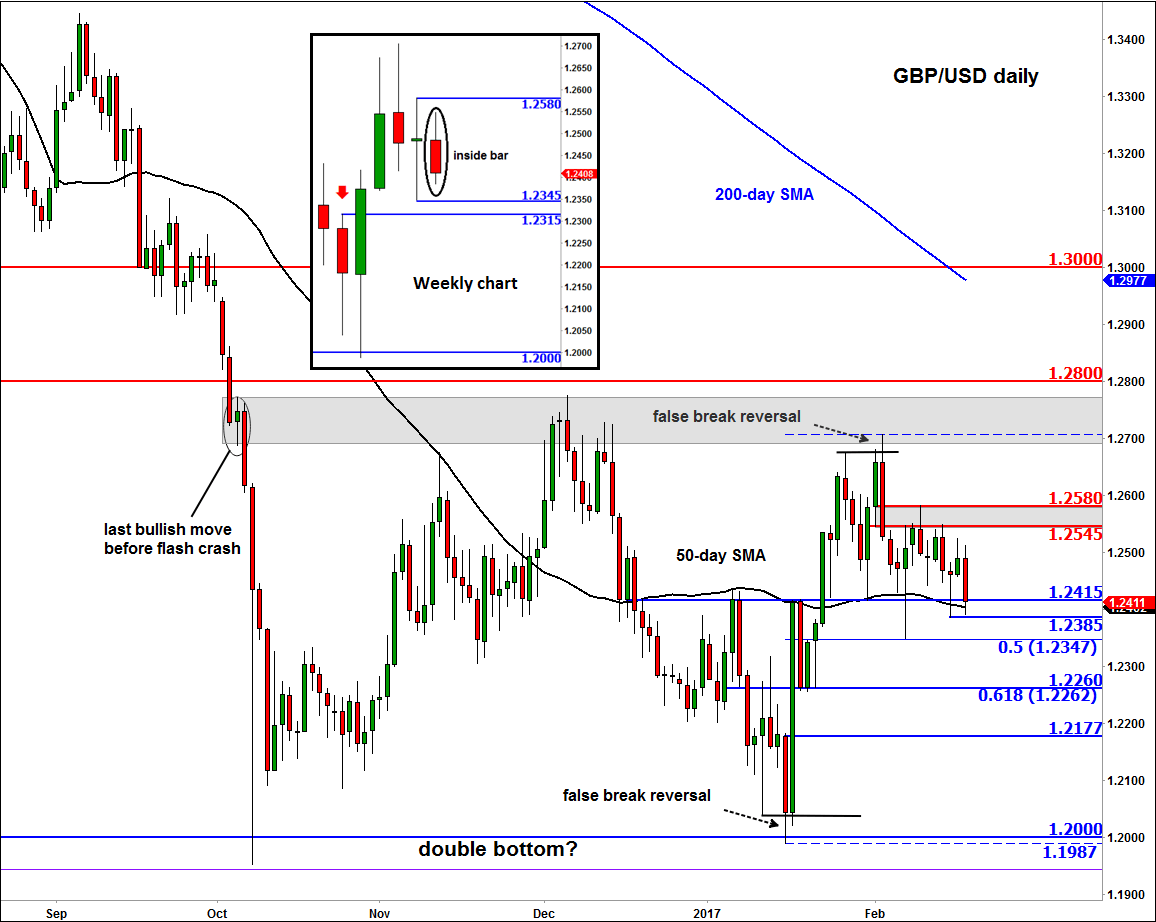

GBP/USD testing key 1.24 support

Well if the cable was going to bounce back, it would do so around these levels. As can be observed from the main daily chart, below, the area around 1.2400 has been strong support in recent days. This level was previously resistance and where the 50-day moving average comes into play. Given the still bullish market structure (because of the double bottom reversal formation at 1.20), we wouldn’t be surprised if the GBP/USD were to bounce back at around 1.2400 once again, especially as the EUR/GBP was correspondingly testing its own resistance around the 0.8580 level at the time of this writing.

Unless the cable now goes on to fall below 1.2345 or rise above 1.2580 (i.e. last week’s range), it is set to create an inside bar formation on the weekly chart (see the inset). If so, this would leave behind an interesting setup to look forward to next week. Specifically, traders will want to see what the cable would do around this week’s range extremes. A typical scenario that I would be looking for in this case would be if in early next week the cable dips below this week’s low and into a key support level such as 1.2315, trap the bears, before rising back above the low of this week. In this scenario we would be anticipating the cable’s next move, possibly around mid-week, to be bullish.

In any case, a potential move back above the 1.2545-80 resistance area would re-affirm the bullish technical bias. If that were to happen then we would expect to see a rally back to the top of the range and possibly towards 1.28 or even 1.30 next. However, should support at 1.2315 on the weekly or 1.2260 on the daily time frame (which is also the 61.8% Fibonacci level) break then we may see the start of a move towards 1.20 again.