UK Retail Sales Budget amp FTSE100

UK retail sales excluding fuel items rose 3.3%, posting their highest increase since May 2008. UK retail sales ex fuel m/m rose 1.9% highest since […]

UK retail sales excluding fuel items rose 3.3%, posting their highest increase since May 2008. UK retail sales ex fuel m/m rose 1.9% highest since […]

UK retail sales excluding fuel items rose 3.3%, posting their highest increase since May 2008. UK retail sales ex fuel m/m rose 1.9% highest since April 2011

Although the UK Treasury reduced its GDP forecasts and the peak in debt was estimated to be later than anticipated, it does not appear that either S&P or Fitch will join Moody’s in downgrading the UK. Many comparisons have been made with France (which has been downgraded by S&P and Moody’s). Although both the UK and France have a debt of 89% of GDP, France’s debt deficit (total debt minus government receipts from exports and taxes) is below 5.0% of GDP versus nearly 8.0% of GDP for the UK. And if the UK economy dips back into recession for the 3rd time, then prospects of improved government revenues may be slim. Another key factor considered by credit rating agencies (but not as much by the public) is the maturity of the debt –how much needs to be repaid this year and the next. By end of 2013, the UK must repay over £132 bln in principal and interest payments, half the amount owed by France.

One key reminder is that the UK the enjoys greater monetary autonomy than France or any other Eurozone member via currency policy (ability to talk down the pound via BoE’s inflation & growth pronouncements), monetary policy

(stepping up asset purchases programs to reduce supply of outstanding gilts and reduce borrowing costs) and European policy (unburdened by contributing into the European Financial Stability Facility or upcoming European Stability Mechanism).

2013 growth forecast was halved to 0.6% from December forecast, 2014 expected at 1.8% from the initial 2%.

The UK deficit is projected at 7.4% of GDP this year, 6.8% of GDP in 2014 and 5.9% of GDP in 2015.

Debt/GDP seen at 79.2% in 2013/14, 82.6% in 2014/15, 85.1% in 2015/16 and peaking to 85.6% in 2016-2017, before falling to 84.8% in 2017/18. In otherwords, Debt as a percentage of GDP, will peak in 4 years (instead of the anticipated 3 years)

Chancellor Osborne reiterated the definition of price stability at 2% inflation, but kept the door open for the growth element to be added when Marc Carney is appointed at the helm of the BoE in July. The corporation tax was cut to 20% from 21% starting in 2015, which is a general positive for equities. Stamp duty eliminated on AIM shares if held in ISA.

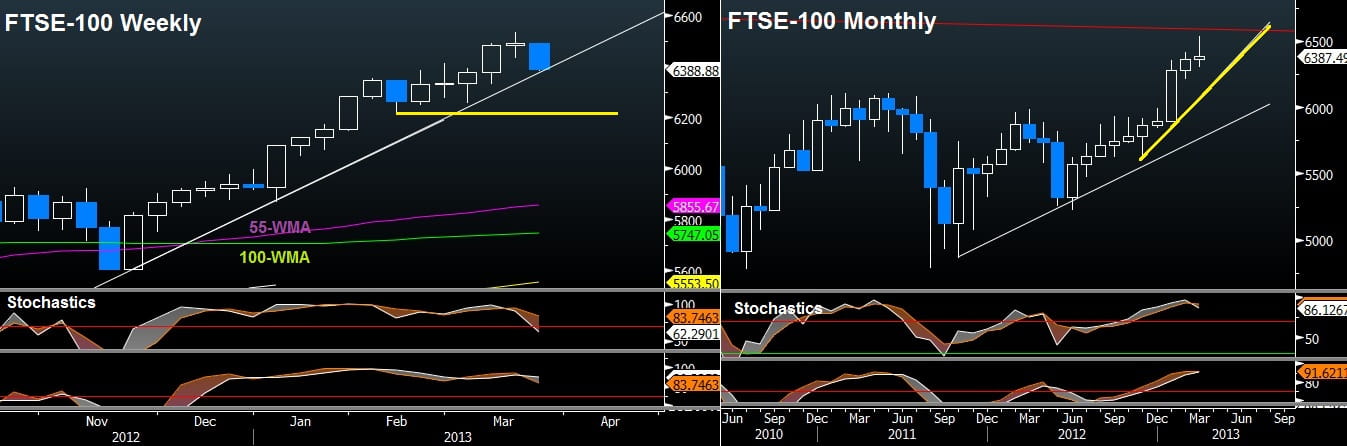

FTSE100 tests the December trendline support at 6,380, a break of which (weekly close) may extend the sell-off towards 6215-20. FTSE will have to close the month at or above 6360 in order to post 10 consecutive monthly gains, the longest since 1997. In the event of a monthly close between 6360-6370, a bearish doji may be in effect.