UK Plc leaves Brexit scramble too late

The ‘Brexit trade’ might look like it’s taking a break at the end of a dramatic week, but hedging markets beg to differ as companies scramble to protect cash.

The ‘Brexit trade’ might look like it’s taking a break at the end of a dramatic week, but hedging markets beg to differ as companies scramble to protect cash.

Global markets largely held on to a positive tone on Friday, enabling the pound to get back above $1.42, and oil, European bank stocks and government bond yields to tick up from lows.

Still, whilst the pound was settling some 80 points higher than the day before, demand for deals to insure large sterling/dollar transactions remained strong.

Friday brought the umpteenth record high reading in short-term sterling/dollar implied volatility within a few weeks.

That suggested not everyone shared the view that tumultuous events on Thursday might shift voters from choosing Brexit.

In other words, some speculators and companies were still doing deals aimed at shielding foreign exchange trades from whipsaws in currency markets following a Brexit.

Reuters reported on Friday afternoon that such deals “still showed good volumes despite concerns over liquidity”. Thursday was the third-busiest day for cable option volumes, the data provider said, with a mix of puts and calls highlighting last-minute hedging and position taking.

Volumes were highest in ‘puts’ (options to sell) with $1.35 standing out, pinpointing that level as one traders expect sterling against the dollar to fall to. The move would be some 5% from current levels.

FTSE companies which at any one time hold large chunks of cash denominated in dollars include Rolls-Royce, BAE Systems, GlaxoSmithKline, Diageo and British American Tobacco.

However Reuters said that according to its soundings, many major groups had still not finalised plans to deal with turmoil from a Brexit.

And as of February, more than three-quarters of Britain’s FTSE 250 companies had not made any contingency plans for a possible UK exit from the EU, according to a survey by the Chartered Institute of Internal Auditors.

Lower down the financial food chain, small to medium-sized enterprises, whilst worried about the impact of sterling volatility, have been reluctant to insure against it.

World First, a currency transfer service, said earlier in the year that almost half the SMEs it surveyed admitted to ‘not really taking any notice of the currency markets’.

Maybe the currency markets have drawn more corporate attention now a Brexit is perceived to be likelier.

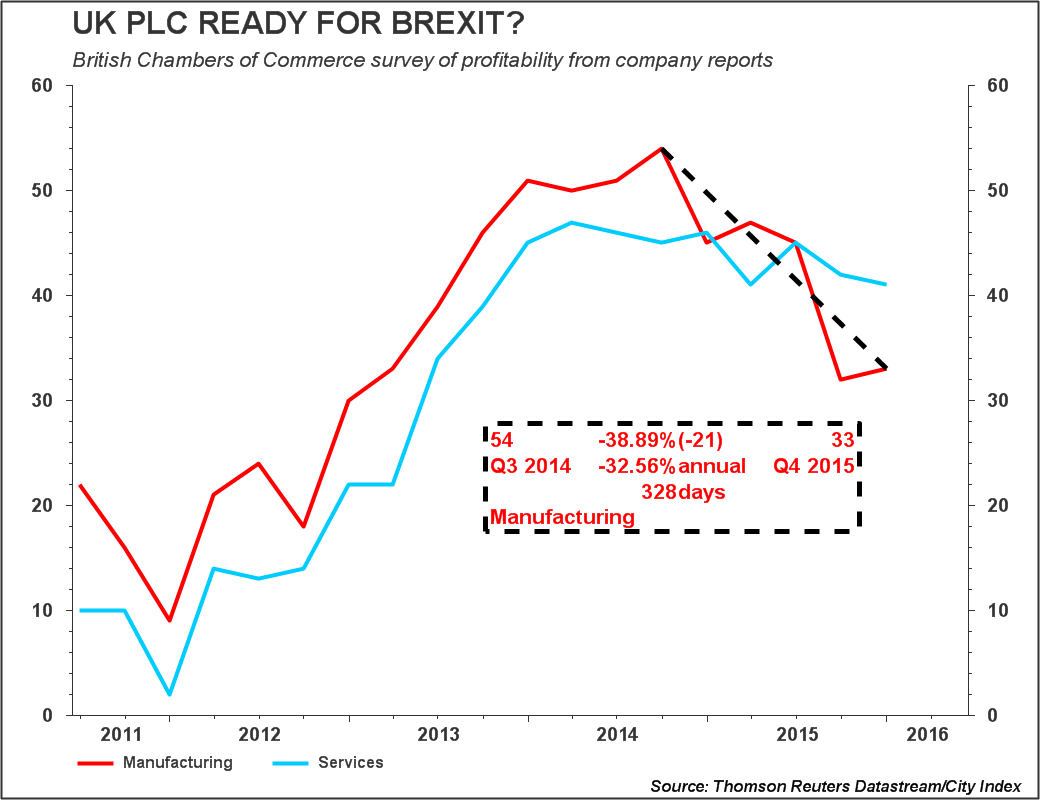

Unfortunately, corporate confidence in future profits dipped last year, particularly among manufacturers.

The British Chambers of Commerce’s corporate ‘confidence in profitability’ index of UK manufacturers showed a c.40% fall between the third quarter of 2014 and the end of last year.

New headwinds against British profits would be particularly unwelcome. Cross-market fireworks and patchy corporate preparation would compound any hit to earnings, leaving FTSE indices lower for the year.