UK oil giants report earnings amid price collapse

How will oil price tank affect oil earnings? The UK’s petroleum behemoths will hog market attention this week with a raft of closely-watched quarterly earnings. […]

How will oil price tank affect oil earnings? The UK’s petroleum behemoths will hog market attention this week with a raft of closely-watched quarterly earnings. […]

The UK’s petroleum behemoths will hog market attention this week with a raft of closely-watched quarterly earnings.

The market is particularly keen to know how oil revenues have fared following a tumultuous collapse of oil prices over the last four months.

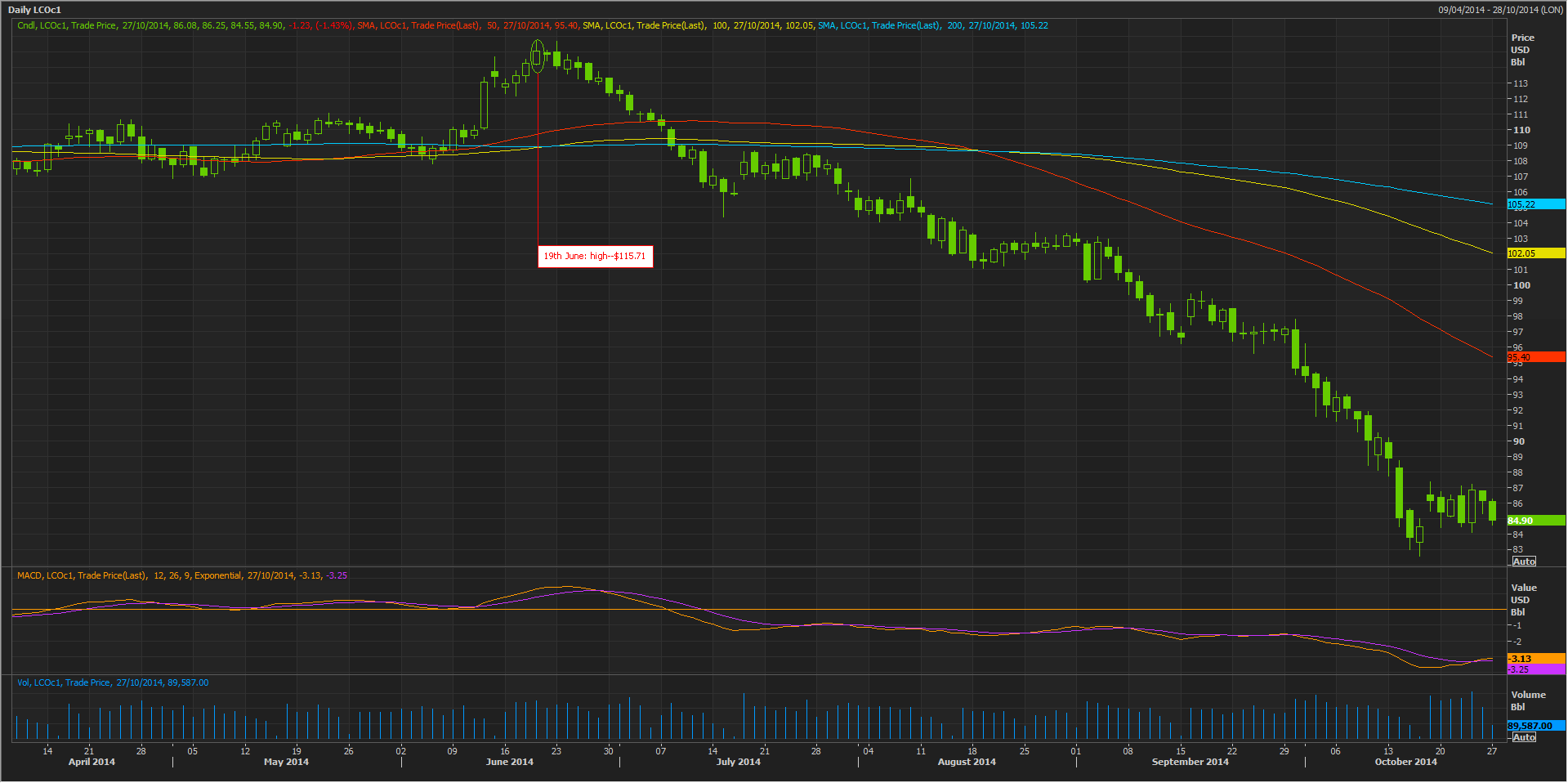

The price of the US-focused Nymex Light Sweet Crude Oil for delivery in three months has dived from a high of $106.91 a barrel in mid-June, to lows below $80 dollars a barrel, in late October, prices not seen for half a decade.

Nymex crude’s more Europe-facing counterpart oil futures contract, ICE Brent Crude, fell by a similar amount, approaching 30%, over the same period.

The fall in crude all prices will train sharp attention among investors on how Europe’s major oil companies plan to carry out ambitious cost-cutting plans in an increasingly tough environment.

Oil companies have seen billions wiped off their stock market values in reaction to the fall of crude prices, due to slowing global demand particularly in China, and ample supplies.

Investors have scrambled to re-calculate the amount of leeway oil majors have left to protect earnings by cutting investment and operating expenses.

Shell is in the midst of a push to shed $15bn in assets this year. BP has sold $40bn of assets since the 2010 Gulf of Mexico spill and announced an additional $10bn by 2015.

After selling low-margin oil fields and downstream assets in recent years, some oil majors have been shifting focus to reducing operating costs.

Shell and Chevron cut hundreds of jobs in the North Sea and BP slashed 275 in Alaska earlier this year.

On the whole, third-quarter profits are set to be down by around 10%-to-25% from last year and 13% from the previous quarter.

Shell however is likely to be an exception.

It is expected to see a year-on-year rise in profits, according to analysts’ consensus forecasts.

In the short term, oil companies are probably able to deal with the crude price slump by tapping into existing free cash flow in order to maintain operations, borrowing targets and dividends.

Refining trends for all major oil producers will be an unusual bright spot after refining margins reached a two-year high this month at nearly $9 a barrel, mainly in line with lower crude prices and plant outages.

The dollar having strengthened during the quarter will also offset some oil price weakness.

Shares of the UK’s leading oil firms, Royal Dutch Shell, BP and BG Group have tumbled 15%-20% since June, whilst their European counterparts like Eni SpA. and Total SA. have fallen by a similar amount.

A consensus of analysts compiled from polling by Thomson Reuters gives probable adjusted earnings per share (EPS) for the quarter to the end of September of $0.146, a fall of more than 25% compared to $0.196 in the same quarter a year ago.

We note there appears to be a relatively large consideration of one-off effects expected by analysts given that an average forecast with the exceptional income included gives an EPS of $0.552.

Net income is seen at $2.948bn compared with $3.692 the year before.

BP is expected to increase dividends and maintain share buybacks, despite weaker revenue from its 20% stake in Russia’s Rosneft.

With strong organic cash flow, BP is likely to raise its quarterly dividend from 9.75 cents per share to 10 cents.

For BP, falling oil prices and revenue are just the latest challenge it has faced this year.

Its 20% stake in Rosneft came under scrutiny due to western sanctions on Moscow and as the scale of its fine over the 2010 Gulf of Mexico oil spill threatened to mushroom, following signs of further litigation over the incident.

In September, BP was found guilty of “gross negligence” and “wilful misconduct” under the Clean Water Act for its actions leading up to the Macondo oil spill in the Gulf of Mexico in 2010.

The maximum penalty BP faces now looks to be about $18bn (£11bn)—that suggests about 47p a share on top of BP’s existing provisions of $3.5bn for this particular penalty.

However, with BP making it clear it will appeal and appeals (and counter-appeals) not set to begin until January 2015 at the earliest, there is ample time for the negative effect on earnings and sentiment to be diluted.

It is expected to show earnings progress following delivery of key projects.

Even so, its EPS is still expected to have sagged under the weight of oil price falls. For the September quarter, the adjusted figure is seen at $0.225, compared with $0.310.

Revenues are forecast to be $5.724bn after $4.426bn in September 2013 whilst net income is seen at $786.51m after $1.070bn in same quarter last year.

BG may also provide guidance on the potential for further disposals after the group in June sold a majority stake in one of Europe’s biggest gas pipelines to Antin Infrastructure Partners for nearly $1bn.

There were news reports during the summer BG was considering selling its largest operations in the North Sea for about $1.7bn.

BG’s gas well flows will also be a focus, after it produced higher-than-expected flows of gas from a test well off the coast of Tanzania, boosting the financial viability of its planned liquefied natural gas export terminal in the country.

Net income is expected to be $5.584bn, more than 25% higher than a year ago but down about 9% on the previous quarter.

The Anglo-Dutch major has enjoyed a rapid recovery over the past year through asset disposals and the ramp up of production in the Gulf of Mexico.

Adjusted EPS for Shell is expected to come in at $1.731 compared with $1.420 in the September quarter of 2013.

Aside from relatively strong earnings, investors will be seeking updates on RDSA’s disposal program.

One particular focus may be a failed deal by Shell to sell its stake in Australia’s Woodside Petroleum back to the firm for $2.68bn, after the Australian group’s shareholders declined to approve the deal.

That left Shell holding a 14% stake in Woodside that it intends to sell.

However, Shell indicated after the failed sale it was not dependent on Woodside buying the stake back for Shell to meet its target of selling $15bn in assets.

Relative value, though dividends face pressure

Shell, Total and BP shares are trading at between 9.1 and 9.9 times forecast earnings, suggesting relative value compared to a ratio of 10.7 for the STOXX Europe 600 Oil and Gas.

Yet analysts also cite a rise in European energy bond yields as a sign of increasing concerns about the sustainability of dividends in the energy sector – assuming oil prices remain lower for longer.