UK jobs numbers no more hiccups

After years of a surprisingly robust labour market underpinned by strong jobs growth, things took a turn for the worst, at least at face value, […]

After years of a surprisingly robust labour market underpinned by strong jobs growth, things took a turn for the worst, at least at face value, […]

After years of a surprisingly robust labour market underpinned by strong jobs growth, things took a turn for the worst, at least at face value, in the UK’s last labour market report. In the three months to May, the unemployment rate edged up for the first time in two years and the level of employment unexpectedly fell, but there was also a very encouraging jump in wage growth. In fact, wage growth has steadily been trending higher and higher ever since mid-2014, suggesting that the labour market is indeed one of the strongest in the developed world.

Furthermore, while the economy lost 67K jobs in the three months to May, fulltime employment actually increased 45K, meaning that the massive drop in employment came entirely from self-employed, part-time and temporary workers. It’s a healthy sign that workers are transitioning into full-time roles as the economy improves, at the same time as wage growth increases and claimant count rate broadly decreases – the latter actually remained flat in June, but it has been trending lower ever since the beginning of 2013.

In the three months to June, the economy is expected to shed 55K jobs – it’s an encouraging sign that employment is at least heading in the right direction – and the unemployment rate may remain at 5.6%. The market is also anticipating that average weekly earnings growth falls to a still encouraging 2.8% over the same period. In July, the claimant count rate is expected to remain at its lowest level since Q1 1974 (2.3%). Overall, the data may help reinforce the idea that last month’s release was only a blip on the BoE’s jobs radar.

After last week’s surprisingly dovish ‘super Thursday’, the market pushed back its expectations for higher interest rates until late Q1. This set of employment numbers is an important part of this mix, as the stronger the labour market is the more likely the BOE will be to raise interest rates. A stronger report here could dispel any remaining doubt about the health of the labour market, sending investors flocking towards the pound.

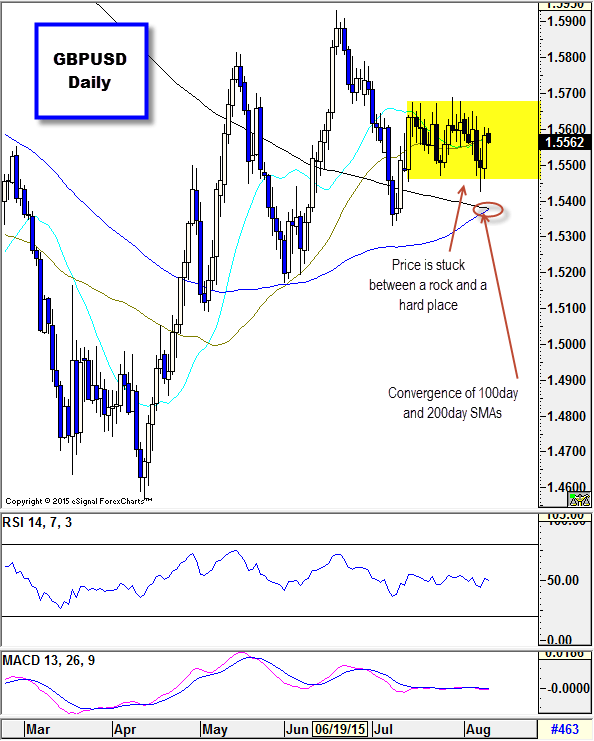

GDPUSD is being hit by widespread US dollar strength at the time of writing, after the PBoC dropped the USD/CNY reference rate by 1.9% in Asia, the most on record. However, a stronger than expected report could easily send the pair back to an important resistance zone between 1.56/57. On the downside, we’re watching support around 1.5450 and then 1.5425 in the event that the numbers miss expectations.