UK GDP amp Gilt Yield Superiority

UK Q3 GDP growth rose 0.8% q/q, its highest level in 13 quarters, while the y/y rate rose 1.5%, the highest in 10 quarters, as […]

UK Q3 GDP growth rose 0.8% q/q, its highest level in 13 quarters, while the y/y rate rose 1.5%, the highest in 10 quarters, as […]

UK Q3 GDP growth rose 0.8% q/q, its highest level in 13 quarters, while the y/y rate rose 1.5%, the highest in 10 quarters, as the improving pace of expansion underlines the breadth of data and sentiment improvement across all manufacturing, services and construction sectors. Services’ aggressive strengthening is highlighted by the 0.4% rise in the index of total services industries, which remained in positive territory for the eighth consecutive month, a feat not seen since 2007.

GDP growth exceeded the 0.7% 1/1 pace recently forecast by the BoE, while annualised growth is seen at 3.2%, according to unofficial ONS estimates.

Three weeks after the IMF’s growth upgrade of the UK (2013 GDP raised to 1.4% from initial forecasts of 0.9% and 2014 GDP raised to 1.9% from initial 1.5%) was the biggest single improvement forecast for all G7 nations: the latest hard data confirms the upgrade. This was especially highlighted as the IMF cut its forecast for 2013 global growth to 2.9% from 3.2%.

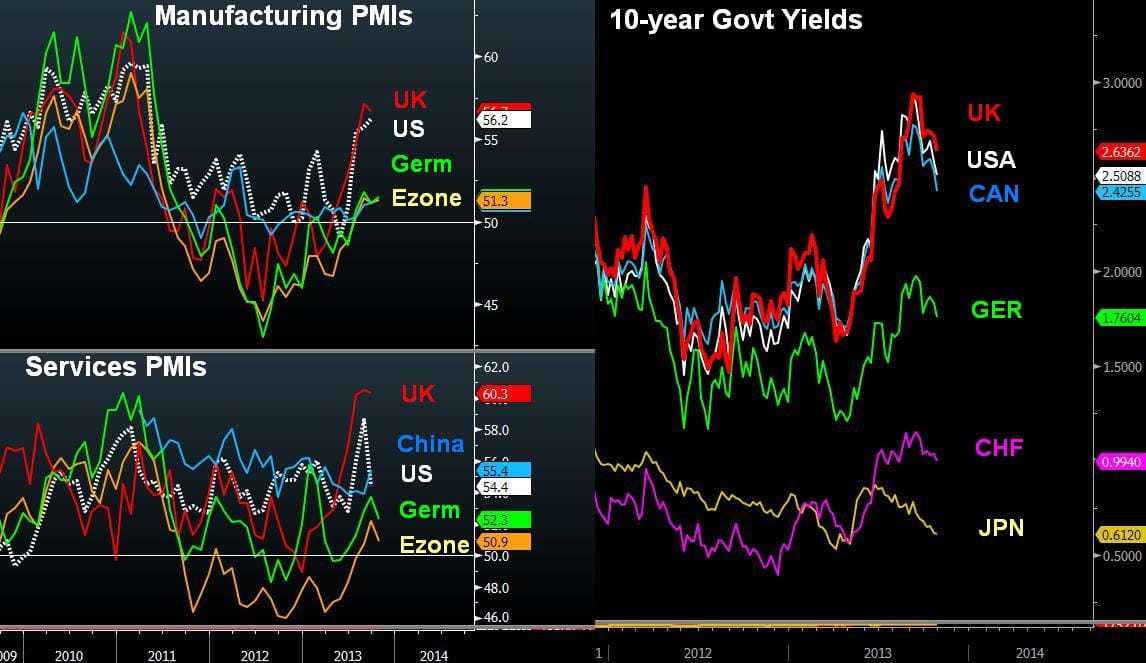

Back to usual UK yield superiority

UK 10-year yields have outperformed their counterparts in the US, Canada, Germany, China and Switzerland since late August. Yield superiority in UK 10-year gilts relative to the rest of the world is nothing new as this had prevailed during most of 2011, 2010, 2009, 2008 and 2007: with 2012 being the exception as UK GDP growth contracted in 2 quarters of the year.

While UK 10-year yields below their Australian counterpart at a -1.33% (UK-Aussie spread), the yield differential reached -1.0% in September, the smallest negative spread since April 2009.

GBP is the highest performing currency in the G10 over the last 3 months, rising 5.2% vs USD while beating the Swiss franc, euro and Aussie.

One particularly favourable sterling development going forward is the gradual retreat from the Bank of England’s efforts to talk down bond yields in the face of the blitz of positive data surprises from the UK.

Another favourable prospect for GBP is that the BoE may tacitly encourage currency strengthto act as a deterrent against stubborn inflation, as CPI remains well above the 2.0% objective and 2.5% maximum.