UK CPI preview is the inflation genie out of the bottle

UK inflation data for September is scheduled for release on Tuesday at 0930 BST. The market is expecting prices to rise by an annual 0.9% […]

UK inflation data for September is scheduled for release on Tuesday at 0930 BST. The market is expecting prices to rise by an annual 0.9% […]

UK inflation data for September is scheduled for release on Tuesday at 0930 BST. The market is expecting prices to rise by an annual 0.9% rate last month, up from 0.6% in August. Core prices, which exclude energy and food prices, are also expected to pick up to 1.4% from 1.3%.

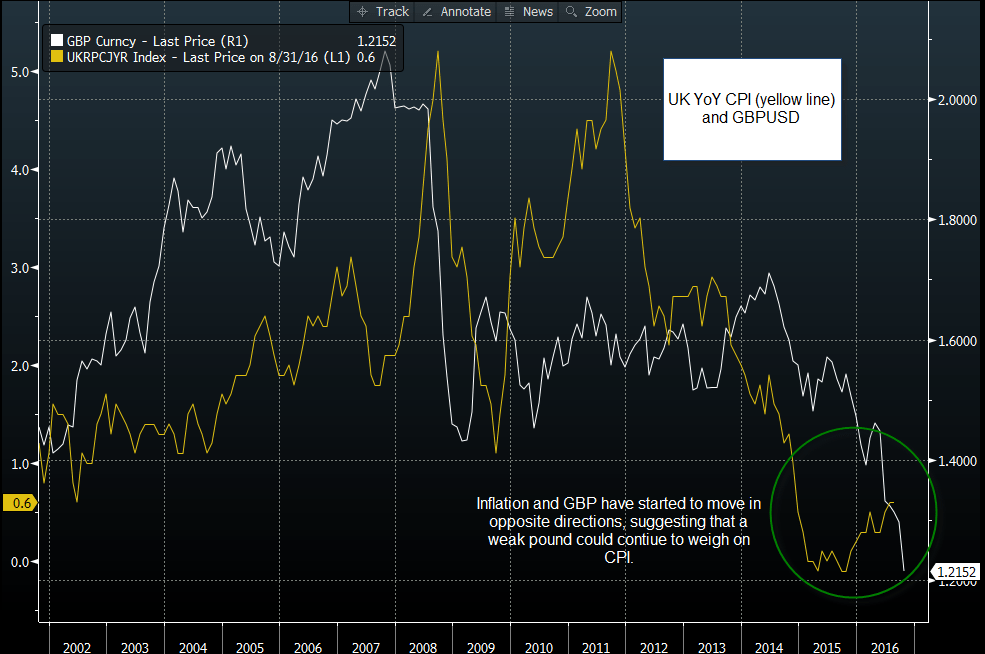

We believe that the risks are to the upside for September’s price data, as the impact of a weak pound continues to weigh on price pressure. This theme is likely to persist, since the pound’s flash crash on Friday 7th October, GBPUSD has made fresh record lows each day, suggesting that higher prices may stick around for some time.

How a weak pound impacts inflation:

Below is a simple guide to how the pound can impact prices in the UK.

While a weak pound is likely to boost consumer prices, the actual relationship between a weak pound and inflation is not as clear cut as it seems. It is difficult to determine the exact impact on inflation because it depends on how producers and retailers react to the price rises. Firms could absorb some of the higher cost of imports rather than pass on the increase to their consumers if they think the economic outlook is weak. Thus, the degree of pass-through is difficult to calculate, this means that UK CPI data has the potential to surprise market expectations, which may trigger volatility and trading opportunities.

Trading opportunities around inflation data:

Sterling: In usual economic conditions rising inflation, especially from such a low base, could be sterling positive because it may put pressure on the Bank of England to raise interest rates. However, the uncertainty around Brexit means that these are not normal economic conditions, and the BOE has said that it could look through a sterling-induced period of high inflation. Thus, we could see sterling fall on the back of rising inflation, as it only darkens the outlook for the UK economy.

Equities: The impact of rising prices hit home last week after a spat between Unilever and Tesco threatened to lead to shortage of Marmite on UK supermarket shelves. Tesco did not want to pay a 10% increase in prices for some Unilever goods as it embarks on a price war with its rivals to entice customers.

Consumer sectors could be hit by falling profitability

Going forward, Tesco may absorb price increases rather than pass them onto their customers, which could further squeeze Tesco’s margins, and may impact the future profitability of the firm. Since profits are a key driver of share prices, signs that firms are struggling with rising inflation, could weigh on the FTSE. Sectors that are particularly vulnerable, include consumer staples and consumer discretionary, while utilities and health care are likely to be more resilient to price rises, as they are more likely to pass on any increases to consumers rather than squeeze their own margins.

Overall, CPI data is going to be a key economic release for traders going forward. We think that the risk is for an upside surprise, and annual CPI could breach the 1% mark for September, while the market expects a reading of 0.9%. A strong inflation reading could be another reason to sell the pound tomorrow, which, ironically, could lead to even higher inflation in the coming months. If prices rise as we expect, then the MPC’s 2% inflation target to be breached at some point in Q1 2017.

If, against the odds, CPI does not rise by as much as expected, then we would expect the pound to rally as it could brighten the UK economic outlook and put less pressure on future consumption. However, we view this outcome as unlikely at this stage.

Figure 1: The pound and CPI over the years

Source: Bloomberg and City Index