UK budget report 2015 Live Blog

Welcome to City Index’s Live Blog on Budget Day. Our team of market experts comprises our Chief Global Strategist Ashraf Laidi, Chief Market Strategist Joshua […]

Welcome to City Index’s Live Blog on Budget Day. Our team of market experts comprises our Chief Global Strategist Ashraf Laidi, Chief Market Strategist Joshua […]

Welcome to City Index’s Live Blog on Budget Day. Our team of market experts comprises our Chief Global Strategist Ashraf Laidi, Chief Market Strategist Joshua Raymond, experienced market analyst Ken Odeluga, and other industry analysts, traders and commentators. They’ll be guiding you through the budget speech as it happens and we’ll also be bringing you all the reaction live from the trading floor.

This page automatically reloads every two minutes so there’s no need to hit refresh.

That’s it for this year’s live budget blog. Thanks for joining us. Why not catch up with what else is moving the markets in our Market News & Analysis section?

Our live blog will be back to cover the 2015 General Election from the beginning of May.

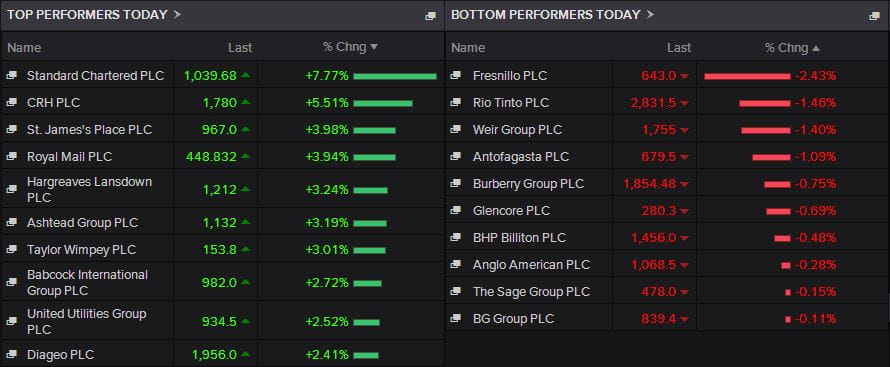

Joshua Raymond, City Index’s Chief Market Strategist: And so as many analysts, reporters and individuals focus on the fine print of the 2015 Budget Speech, traders of the FTSE will be happy to see that the benchmark UK 100 index has rallied over 100pts on the day and now looks primed for another assault on the crucial 6950-7000 level. Financial stocks such as Standard Chartered and Hargreaves Lansdown are adding the most to the index with Fresnillo, the precious metal miner, the top loser on the day.

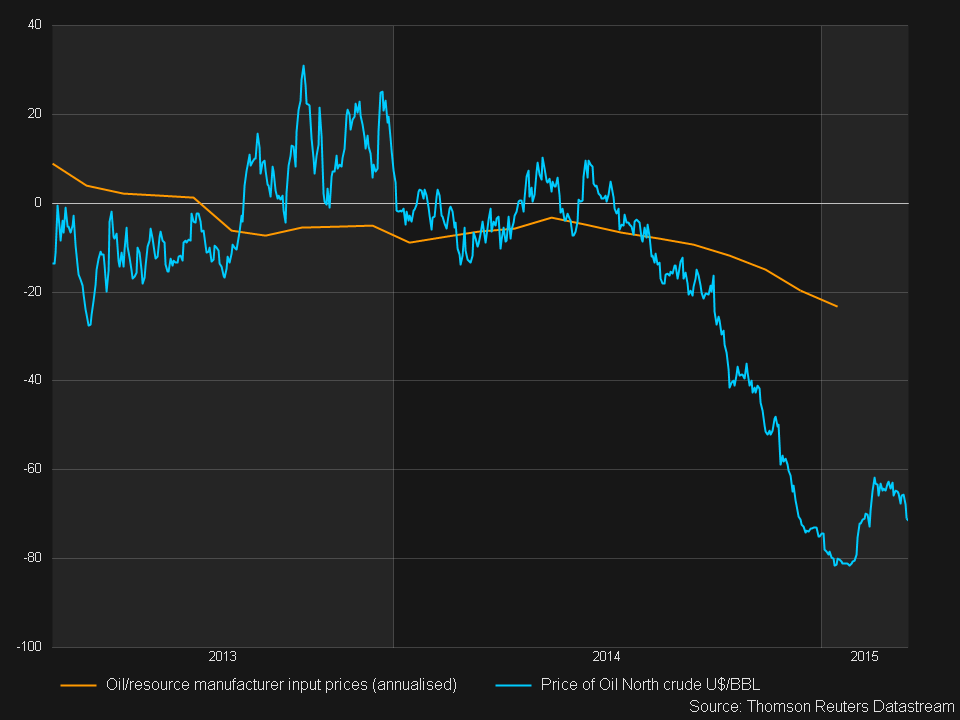

Ken Odeluga, City Index’s Market Analyst: Here’s a chart showing a variant of the Office for National Statistics’ (ONS) regular Producer Price Index.

The data from all industries except from the UK oil and ‘materials’ sectors (mostly miners), were stripped out.

The readings were annualised and plotted against the price of crude oil pumped out of the North Sea, also annualised.

The effect of oil prices falling below the costs of getting that oil onshore has made doing business in the region unviable for many companies, whilst pushing the indebtedness of smaller firms to critical levels.

Investment in the region has stalled, partly because the North Sea (AKA the ‘UK Continental Basin’), is one of the most mature in the world, and now one of the least attractive to invest in.

But the investments are currently worth around £5bn a year to the UK government and the industry employs around 450,000 people in the UK.

Oil output from North Sea fields has slipped to its lowest level since production began in the mid-1970s.

North Sea investments worth around £25bn are currently unsanctioned as companies have been waiting for the government to intervene.

Chancellor George Osborne introduced an Investment Allowance in The Budget to boost the UK oil industry

#GBP crushed by earnings & BoE minutes but still high in TWI terms #Budget2015

http://t.co/x4QHxVu6mc

#forex pic.twitter.com/RIlfUpRzU2

— Ashraf Laidi (@alaidi) March 18, 2015

Missed by some but UK govt set to spend £50m more in 2015/16 on Counter-terrorism and security

#Budget2015

— Joshua Raymond (@Josh_CityIndex) March 18, 2015

City Index’s Michael Willis: No major movements from stocks as a result of the budget as it looks like George Osborne met market expectations on most issues. A cut in Petroleum Revenue Tax from 50% to 35% has kept oil stocks in broadly positive territory; however, gains remain modest.

In the housing sector, Taylor Wimpey has picked up momentum following the announcement that the Government will help first time buyers with a new Help-to-Buy ISA, contributing £50 to every £200 saved by would be homeowners. The stock has sharply risen and seen a spike in volume compared to the 10-day average in the last 30 minutes.

Another expected tax reduction in the beverages sector has boosted Diageo modestly. We’ve seen increased volumes in the stock over the announcement that there’ll be reductions in beer, cider and scotch whisky duty and wine duty remaining frozen. Something to celebrate (in moderation) for consumers and investors alike.

Joshua Raymond, City Index’s Chief Market Strategist: Here are the revisions to public-sector net borrowing compared to previous budget forecasts. It shows that borrowing will fall in the next year to £75.3bn and £39.4bn in 2016/17.

This fall was expected but I had thought borrowing might drop as low as £73bn in 2015 and £38bn in 2016.

Stay tuned as we’ll be posting a key highlights graphic very soon so you can get all the important info in bite size.

#Oil micro-cap Parkmead's stock surges 10% up after N Sea tax relief. Here's how much it fell last yr: #Budget2015 pic.twitter.com/JG67UVOePk

— Ken Odeluga (@Ken_CityIndex) March 18, 2015

Joshua Raymond, City Index’s Chief Market Strategist: Here are some of the key projections that have been revised by the Office of Budget and Responsibility that you need to know. I think this makes the Bank of England less hawkish than a few months ago.

Well that’s it. Not a record-breaking speech by any means, but plenty to digest – including the government’s plans to provide ISAs for first-time buyers in the property market. If you’d like to read the whole document, here it is: UK Budget 2015 (PDF document).

Stay with us, though, for our analysis and reactions on the budget announcement’s impact.

#Budget2015 – thats it…

Birtain – "the comeback country"

Up steps Ed Balls, *turns off TV*

— Joshua Raymond (@Josh_CityIndex) March 18, 2015

#Budget2015 25% top up on your savings towards firt time buyers…… more free cash

— Joshua Raymond (@Josh_CityIndex) March 18, 2015

Joshua Raymond, City Index’s Chief Market Strategist: This is a fairly low headline budget so far, which is no real surprise given the election is merely six weeks away. The big takeaway for me is the fact that UK inflation will be lower than previously forecast, and for longer. That could boost consumer spending in the near term. However, UK GDP was upgraded less than expected this year and downgraded in line with expectations in the long term. So lower inflation and lower growth translates to interest rate hikes being pushed further afield.

#Budget2015

Will Miliband ever be able to live his 2 kitchens down? Osborne and Cameron making the most of it

— Joshua Raymond (@Josh_CityIndex) March 18, 2015

Ashraf Laidi, City Index’s Chief Global Strategist:

Falling borrowing – UK Chancellor Osborne sees UK Government borrowing falling to £90.2 bn, £1bn lower than the Autumn Statement in December. Borrowing will further decline to £75.3bn in 2015-16, then £39.4bn the following year.

Falling debt – Debt as a share of GDP is seen falling to 80.4% in 2014-15; 80.2% in 2015-16, 79.8% in 2016-17; and 77.8% in 2017-18.

Until a surplus is reached in 2018/19 – Osborne sees UK govt deficit 5% happening in 2015. The budget deficit is expected to reach 4% of GDP in 2015-16; followed by 2% in 2016/2017. A budget surplus is forecasted for 2018-19 at +0.2% of GDP.

#Budget2015

North Sea Oil – brings in a single simple tax allowance to support investment

— Joshua Raymond (@Josh_CityIndex) March 18, 2015

City Index’s Michael Willis: A number of major oil stocks have still been on the rise this morning. Gains are less impressive compared to yesterday’s in the sector, as traders await an announcement on a potential tax cut for oil producers. The mood is still positive, but how much can the government actually offer? The recent spike in tax receipts gives the treasury room to extend more of a helping hand than might previously have been expected. This is one to watch closely over the coming hours.

#Budget2015

Market snapshot:

GBP/USD $1.4640 (-0.7%)

EUR/GBP £0.7236 (+0.7%)

FTSE100 6903 (+65pts or 1%)

UK 10yr Gilt yields 1.59% (-9bp)

— Joshua Raymond (@Josh_CityIndex) March 18, 2015

#Budget2015

Ok so thats the headline UK economy numbers. Now need to know about TAX and sectors (housing/oil/tobacco/alcohol)

— Joshua Raymond (@Josh_CityIndex) March 18, 2015

Joshua Raymond, City Index’s Chief Market Strategist: The squeeze on public spending is set to end a year earlier than planned, with public spending set to increase in 2019/20.

#Budget2015

#Lloyds shares unmoved despite the £9bn share sale announcement pic.twitter.com/Q7smvR2cfH

— Joshua Raymond (@Josh_CityIndex) March 18, 2015

A further £9bn of #Lloyds Bank coming on the market. LLOY.L could go deeper into the red today #Budget2015

— Ken Odeluga (@Ken_CityIndex) March 18, 2015

UK officially estimates inflation at 0.2% for 2015. That's ZERO.TwoFive

Dude where's my rate hike?

#Budget2015

— Ashraf Laidi (@alaidi) March 18, 2015

Joshua Raymond, City Index’s Chief Market Strategist: The main headline so far is lower than expected near-term growth upgrade and lower UK inflation for three years.

#Budget2015

OBR see's UK inflation at 0.2% this year, not 1.2% previously forecast!!!!

— Joshua Raymond (@Josh_CityIndex) March 18, 2015

1st mention of #oil by #Osborne in #Budget2015–but not about industry taxes-it's about financial benefits partly fueled by lower oil prices

— Ken Odeluga (@Ken_CityIndex) March 18, 2015

GBP nudging up but it shouldn't be. 2.6% should have been the GDP number for 2015, not 2.5%. thats a miss in my book

#Budget2015

— Joshua Raymond (@Josh_CityIndex) March 18, 2015

#Budget2015

OBR: GDP projections 2015 +2.5% (from 2.4%), 2016 +2.3%, and 2017 2.3%.

LIVE BLOG

http://t.co/XrAvpOGnJK

— Joshua Raymond (@Josh_CityIndex) March 18, 2015

Central judgement of this budget is to reduce deficit & debt. no extra borrowing. no short term giveaway #Budget2015

http://t.co/XrAvpOGnJK

— Joshua Raymond (@Josh_CityIndex) March 18, 2015

#Budget2015 Osborne "took difficult decisions and it worked. Britain is walking tall again"

http://t.co/XrAvpOGnJK

— Joshua Raymond (@Josh_CityIndex) March 18, 2015

The time for speculation is over – George Osborne is set to take his place at the podium and deliver his speech in the next few minutes. Stay tuned for our live commentary.

Joshua Raymond, City Index’s Chief Market Strategist: Key stocks to look at

We think today’s #Budget2015 needs to recognise that households are still trying to recover from 6 years of stagnant wages and rising prices

— Citizens Advice (@CitizensAdvice) March 18, 2015

Ashraf Laidi, City Index’s Chief Global Strategist: GBP/USD at five-year lows. If Labour is looking for points of criticism in today’s Budget Statement, they can refer to the drop in UK average earnings for Jan, slowing to 1.6% y/y from 1.7% y/y, but that would be a moot point as earnings growth has tripled from the 2014 lows. But earnings growth adjusted for inflation remains at its highest level since 2008, after breaking into positive territory in late 2014. Prolonged declines in UK unemployment rate and falling inflation have helped shrink unused capacity (slack) in the economy.

…but pound remains strong. The charts below highlight the accelerating decline in GBP/USD, hitting five-year lows today at $1.4658. GBP selloff was partly caused by softer-than-expected earnings growth, unemployment rate remaining unchanged at 5.7%. The release of this month’s BoE meeting minutes made reference to GBP strength prolonging the slowdown in inflation. The chart below shows GBP remains strong on a trade-weighted index, when including the tumbling euro. If BoE policy makers are truly concerned with divergences in UK monetary policy with Eurozone, then further GBP strength would curb BoE hawkishness and trigger further GBP selling against USD.

Ken Odeluga, City Index’s Market Analyst: With the Chancellor of the Exchequer now widely expected to use a bank levy hike to signal no let-up in constraints to ensure the banking sector doesn’t go back to its old ways, here are some key facts about the ‘banking tax’.

With UK banks already well-adjusted to the levy, plus their stocks having been hit hard over the last year, prospects of a hike aren’t worrying investors too much.

RBS shares are trading 0.3% higher and Barclays is up 0.8%.

Standard Chartered trades 6.2% better after Barclays changed its recommendation in the stock to ‘overweight’ from neutral.

Lloyds is one of the few big banks whose shares are weak today, trading down 0.5%.

Today we set out the next stage in a plan that is working, with a Budget that works for you. We will deliver a truly national recovery

— George Osborne (@George_Osborne) March 18, 2015

The BBC’s Robert Peston highlights how austerity over the past five years has hit the public workforce.

The number of people employed in public sector is 5.4m, the lowest on record (or since 1999). Just 17.4% of employment is public sector

— Robert Peston (@Peston) March 18, 2015

Ken Odeluga, City Index’s Market Analyst: Chancellor George Osborne’s widely trailed assistance to the UK’s North Sea oil producers and services firms may have shifted the spotlight away a bit from a raft of further claw backs against other sectors likely to be announced today.

The Chancellor may turn the screws on big UK-based banks like RBS, Lloyds and Barclays and UK-listed Standard Chartered and HSBC, by increasing the rate of the annual Bank Levy.

The government introduced the Bank Levy—essentially an additional tax on banks—soon after many had to be bailed out with the public purse to the tune of billions.

The levy is meant to discourage excessive employee bonuses and generally foster financial discipline by reducing risky behaviour and attitudes and questionable spending.

The Bank Levy was and remains intensely political.

It has been a useful tool for the current Conservative government to counter accusations that it favours the very wealthy and ‘Big Business’ over ordinary people.

This Budget is also likely to include new taxations on multinationals that divert profits overseas to avoid taxes.

Joshua Raymond, City Index’s Chief Market Strategist: The GBP hits a near 5-year low against the US Dollar on the back of those BoE minutes, which highlighted concerns over GBP strength on low inflation for longer.

The translation from this essentially could mean the UK Central Bank refrains from hiking rates early next year and now moves to try and talk down the pound. A stronger pound makes exports more expensive for other non-GBP countries, which could hurt growth (especially to the Eurozone – the UK’s largest trading partner), and exacerbate deflationary pressures as exporters are forced to cut their prices to boost sales abroad.

UK-US 10 year bond yield spread pts away from hitting 9-year lows

#forex #FTSE #Budget2015 #gilts

— Ashraf Laidi (@alaidi) March 18, 2015

Interest on Her Majesty the Queen's credit card has just got cheaper ahead of #ukbudget2015 after those earnings figures #forex

— Ashraf Laidi (@alaidi) March 18, 2015

GBPUSD LOWEST SINCE June 2010 @ 1.4667 after weaker than expected earnings & BoE concern with deflation from Eurozone #forex

— Ashraf Laidi (@alaidi) March 18, 2015

UK Unemployment rate stays at 5.7% . Average weekly earnings 3mnth falls to 1.8% (from 2.1%) > not great timing for #Osborne

— Joshua Raymond (@Josh_CityIndex) March 18, 2015

Think we might see personal allowance rise to £11k. A key #LibDem aim, and something for them to use to sway #Labour votes #Budget2015

— Joshua Raymond (@Josh_CityIndex) March 18, 2015

Ken Odeluga, City Index’s Market Analyst: Oil firms buoy FTSE amid high hopes.

UK blue-chip oil sector firms kept the FTSE 100 benchmark rallying yesterday, at one point making it the only major stock market in Europe to trade in the black.

Energy sector investors look to be buying in advance of one of the best-leaked features of UK Chancellor George Osborne’s Budget on Wednesday: he is likely to announce an effective tax cut for the sector, which is struggling with rising costs amid the oil price slump.

BG Group shares rose 18.3p to 842p, Centrica added 5% more to its gains on Monday, closing yesterday at 251.2p; Royal Dutch Shell’s B shares gained 43p to 2068.5p.

One of the most indebted and beleaguered FTSE oil firms is Tullow. Its stock rose 6% yesterday.

But with the FTSE 350 Oil & Gas Production Index still down the better part of 25% since June 2014, and tax simplification seen likelier than outright breaks, the sector will have some head-scratching to do if it wants to capitalise on Osborne’s probably subtle changes today.

Joshua Raymond, City Index’s Chief Market Strategist: We have some important data and information out at 9.30am this morning which could well give Osborne a welcome boost ahead of today’s speech.

Today’s major data and announcements (outs