British banks remained firmly out of favour over the past few months. Just last month the FTSE350 Banks Index fell below the nadir struck during the financial crisis. The trajectory for the UK’ largest listed banks has been firmly southwards, although we have seen a slight pick up in share price across the board over the last week or so heading towards the results. There is also a growing expectation that the worst is behind us.

What to watch for:

1. Bad loan charges

Bad loans provisions are expected to ease in this quarter, after huge impairment charges in Q1 & Q2. Tis would be a similar story to what we have seen stateside. As some economic stabilisation returns, bad loan charges have returned to more normal levels, this offers some hope for the UK banks.

Bad loans provisions are expected to ease in this quarter, after huge impairment charges in Q1 & Q2. Tis would be a similar story to what we have seen stateside. As some economic stabilisation returns, bad loan charges have returned to more normal levels, this offers some hope for the UK banks.

2. Net interest income

After the BoE slashed interest rates to a record low 0.1% net interest income is being squeezed. The central bank is still considering negative rates would hit banks hard. Domestically focused, high street lenders such as Lloyds are more at risk

After the BoE slashed interest rates to a record low 0.1% net interest income is being squeezed. The central bank is still considering negative rates would hit banks hard. Domestically focused, high street lenders such as Lloyds are more at risk

3. Investment banking

The larger the investment banking arm the more it stands to gain from volatile markets. Barclays is well positioned here.

The larger the investment banking arm the more it stands to gain from volatile markets. Barclays is well positioned here.

4. Brexit

Brexit uncertainty was an issue for the banks even before covid and remains an issue despite the transition period ending in around 10 weeks’ time. Investors continue to weigh up the impact that a no deal Brexit will have on the economy.

Brexit uncertainty was an issue for the banks even before covid and remains an issue despite the transition period ending in around 10 weeks’ time. Investors continue to weigh up the impact that a no deal Brexit will have on the economy.

5. Dividends

Banks are keen to end the restriction and bring back dividends to distribute excess capital, attract more investors and build confidence I the financial system. Dividends will be a hot topic on earnings calls.

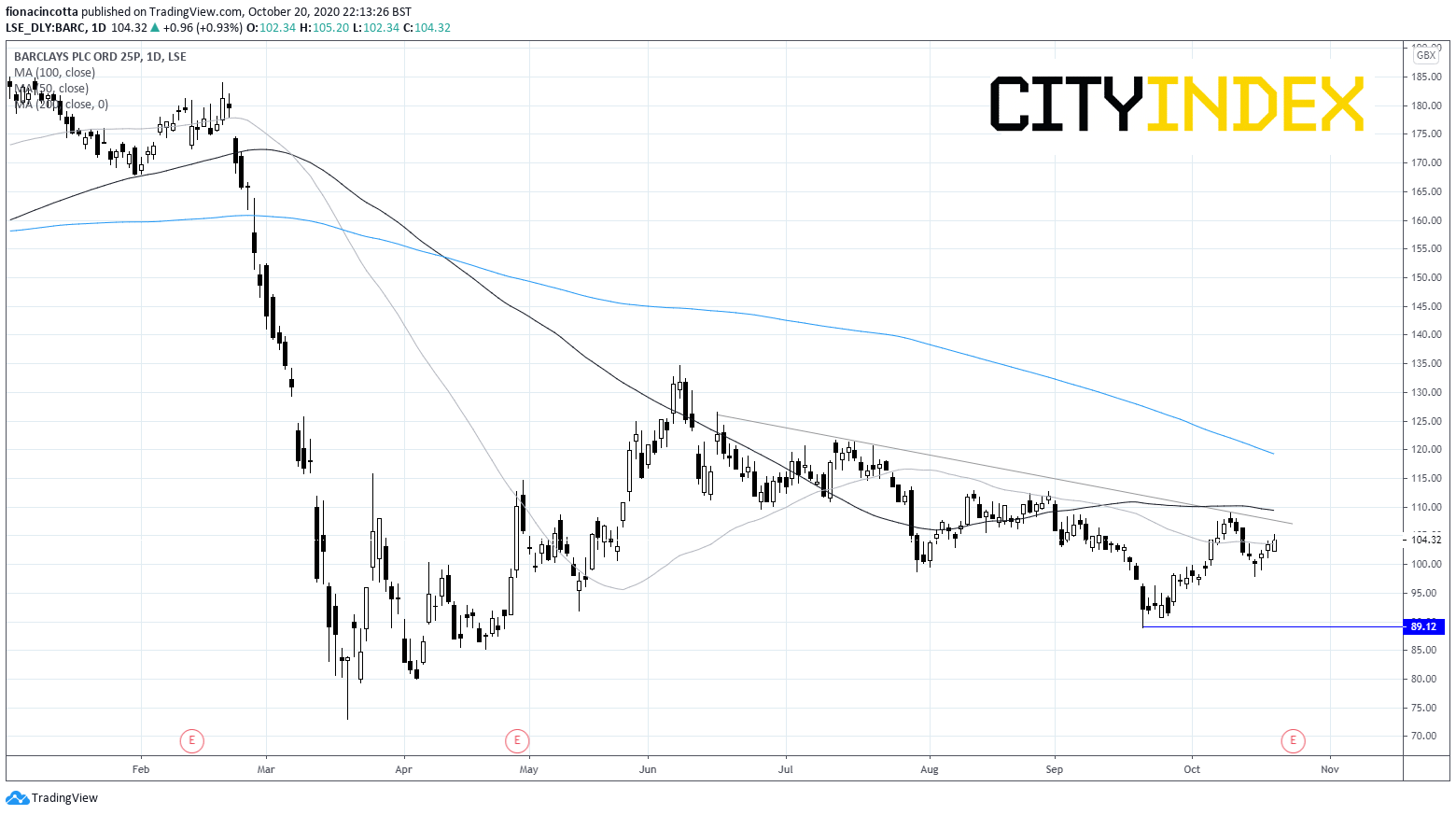

Barclays

Barclays is trading down around 45% YTD, hammered by the covid pandemic. Bad loans are the biggest concern for not only Barclays but for the sector as a whole. In H1 Barclays set aside £3.7 billion as expectations of rising unemployment meant bad loans were also expected to soar. Like in the US, bad loan provisions aren’t expected to be as bad in previous quarters. Net interest income is also under pressure amid record low interest rate and the threat of negative rates. However, Barclays has a sizeable investment banking arm which is likely to have benefitted from high volatility in the markets. This is expected to help offset weakness in the core banking activities.

After rebounding firmly from the mid-March low Barclays has been on a downward trend since early June. It trades below its descending trend line from that date. It also trades below its 100 & 200 DMA, and is testing its 50 DMA, the chart is bearish. Upbeat results could see Barclays push above its descending trendline around 108p and its 100 DMA at 110. A move above these levels could negate the current bearish trend.

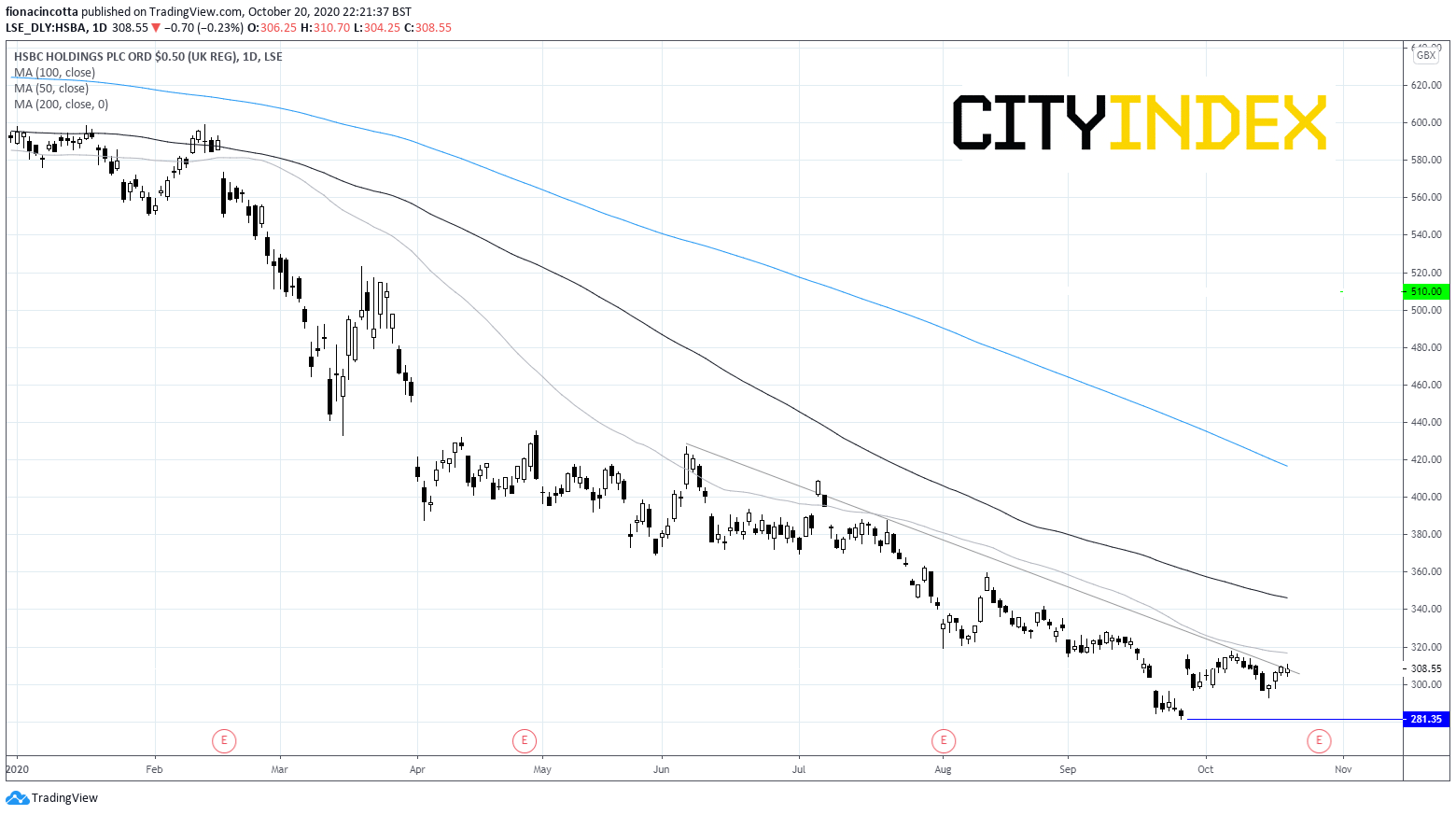

HSBC

In August HSBC, Europe’s largest bank by assets, warned that bad debt charges could reach $1.3billion as the covid crisis hit both its retail and corporate customers across the globe. The pandemic hit came as the bank was already in the midst of restructuring. Profits in H1 were down 69%. HSBC has not only been facing covid headwinds and Brexit headwinds but also geo-political headwinds as relations with China deteriorate. Hardly ideal for a firm that derives most of its profits from Asia. Whilst a strong rebound in economic activity in China could offset some weakness from Europe & US, the outlook for the bank remains particularly gloomy.

The stock fell at the start of the covid pandemic and hasn’t stopped falling since. The pair struck a 25 year low in September having appeared to have found a bottom around 280p at least for now. Whilst the stock trades firmly below its 50, 100 & 200 DMA’ s in a bearish chart, we are seeing some signs of life as it looks to move above its descending trendline dating back to early June. Immediate resistance can be seen at 315p (50 DMA) and 350p (100 DMA).

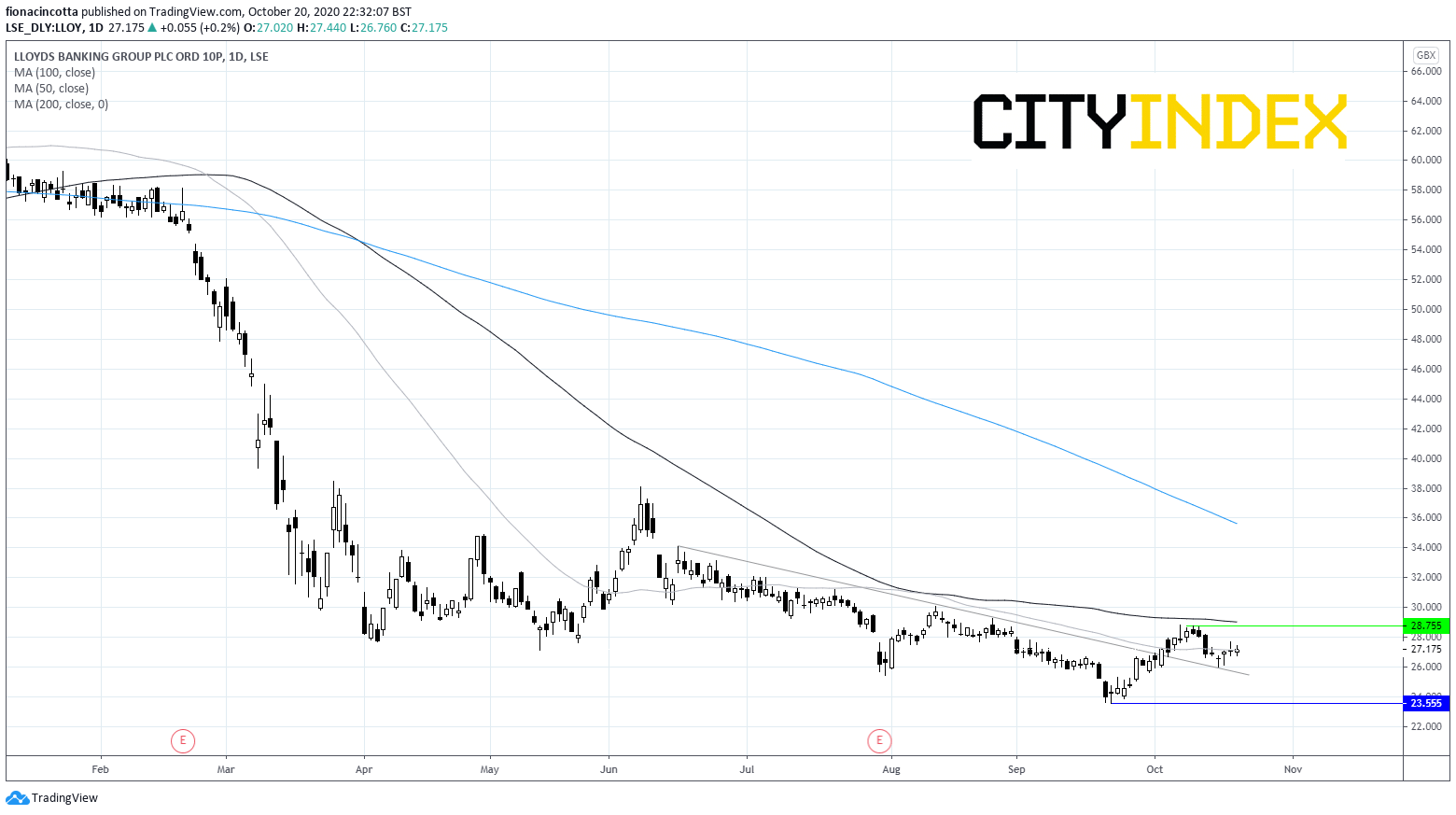

Lloyds

Unlike Barclays, which has a large investment banking arm, Lloyds is much more dependent on interest rates to make money. Lloyd’s position as the UK’s biggest lender and lack of diversification means that it is particularly vulnerable to low interest rates. With interest rates in the UK at a record low 0.1%, net interest income is expected to remain depressed. Bad loan provisions will continue to be under the microscope, although they are expected to be less than in the previous quarter thanks to a fragile economic stabilization. The stocks trade -57% YTD after continuing to fall from mid-March when the pandemic hit.

Lloyds fell at the start of the pandemic in March and has continued falling since, hitting a nadir in September of 23p. The stocks trades below its 50, 100 & 200 DMA - a bearish signal. However, it has managed to climb back over its descending trendline which has been in play since mid-June. Immediate resistance can be seen at 29p, October high & 100 DMA. Immediate support can be seen at 25p, the descending trend line resistance turned support, prior to 23p.

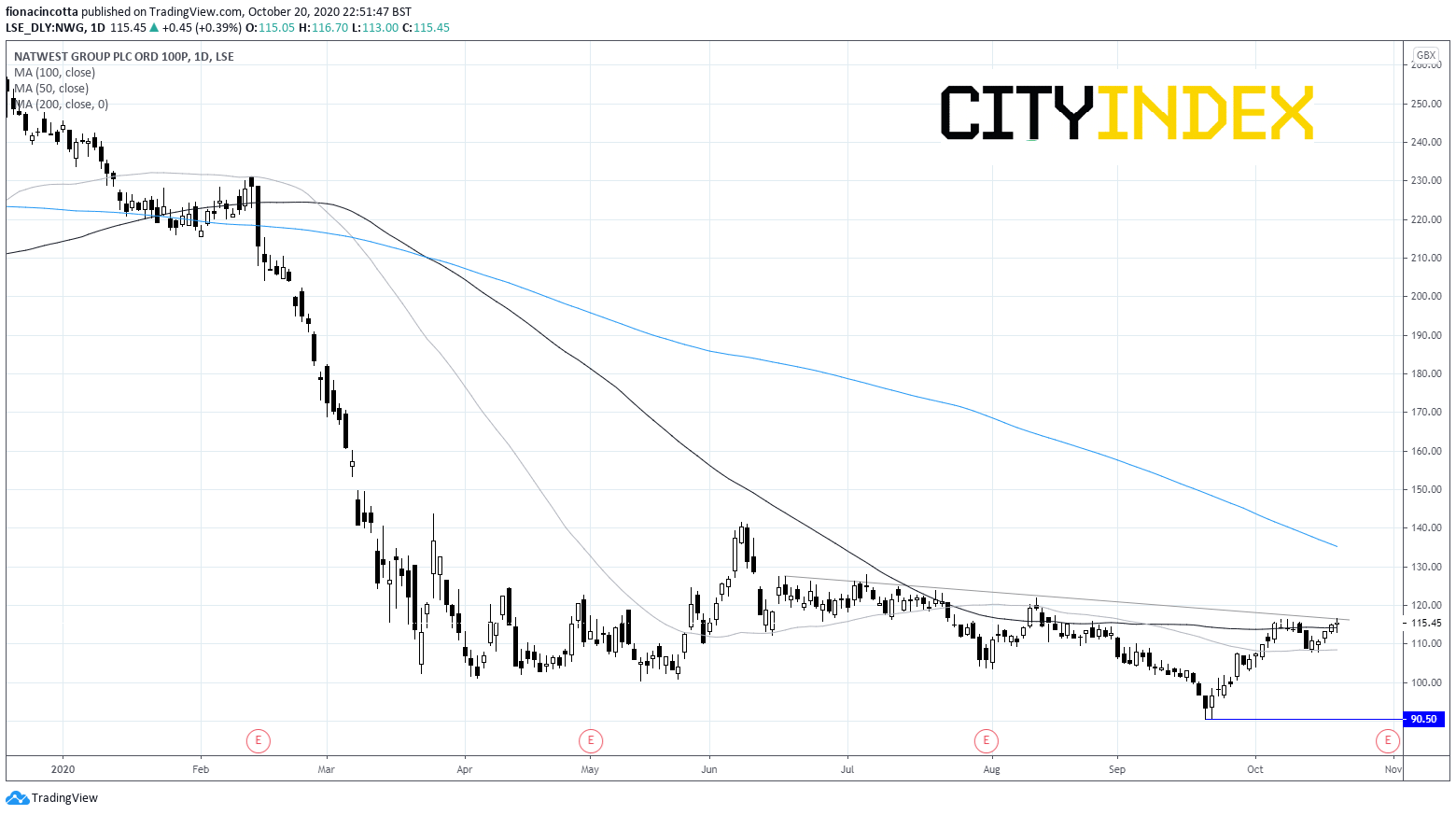

NatWest

Q2’s impairment charge of £2.1 billion from the impact of coronavirus was worse than expected and pushed the bank into a loss of £770 million from a profit of £2.7 billion the year before. Bad loan impairment charges are expected to be less this time round. Net interest income will also be in focus especially as the interest rate is expected to stay so low for so long. However, NatWest, like Lloyds is not very diversified leaving it vulnerable in today’s climate. The stock trades down -55% YTD.

The share price tumbled in early March NatWest experience a small rebound before selling off again since June. The bank struck a nadir of 90p last month and has been attempting to claw back lost ground since. The share price has clawed back over the 50 dma and is testing the 100 DMA and descending trendline at 115/6p. A break above here could negate the bearish trend and be a positive sign that there re more gains on the cards.

Latest market news

Today 08:33 AM

Latest Bank Stocks articles

October 10, 2023 09:31 AM

October 6, 2023 02:28 PM

July 17, 2023 04:03 PM

July 11, 2023 02:28 PM