Tullow shares bounce off all time low banks keep lending

Resource companies’ access to credit has been a powerful influence on their shares this week, and Tullow Oil is the latest big example. Shares of […]

Resource companies’ access to credit has been a powerful influence on their shares this week, and Tullow Oil is the latest big example. Shares of […]

Resource companies’ access to credit has been a powerful influence on their shares this week, and Tullow Oil is the latest big example.

Shares of the deeply leveraged explorer and producer surged more than 10% on Thursday after a favourable outcome from its twice-yearly credit review.

So-called Reserve-Based Lending Reviews, common for oil and gas producers, are a key decider for banks extending credit secured against undeveloped reserves.

Tullow posted a $67.9m half-yearly loss in June, its seventh in a row, but retained a $3.7bn lending facility.

It has cash and undrawn credit worth $2.1bn, with no near-term maturities pending as of 30th September.

It also has around US$6.3bn of committed debt facilities with no near term maturities.

Lenders continued to support Tullow despite low oil prices thanks to the high quality of its asset portfolio, the company said.

It said it was on track and on budget to deliver first oil and cash flow from the key TEN deepwater fields offshore Ghana, in mid-2016.

Tullow’s good news needs to be balanced against news in March that it amended a financial ‘covenant’ (ratio-based agreement) which was at risk of breaking.

Banks agreed to change the reserve-based covenant because there was a risk it might be breached during a period of oil price volatility.

Investment in production and development of assets in West Africa were another pressure.

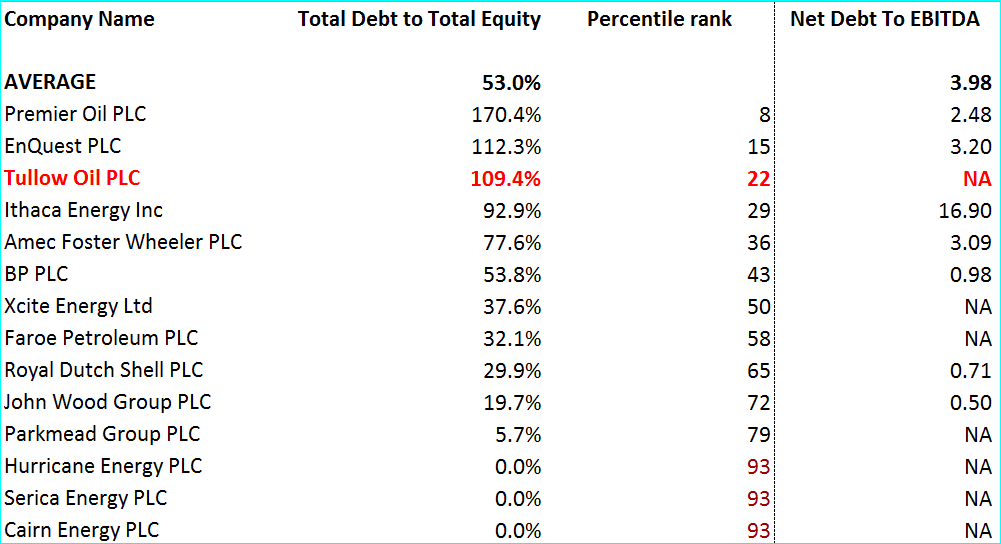

Balance sheets of E&P firms have been strained by last year’s oil price collapse and production costs now exceed profits for the smallest.

Source: Thomson Reuters Eikon

Please click image to enlarge

This has led investors to focus more sharply on their debts, particularly after high-profile bankruptcies.

Aim-listed Afren was the best-known UK-based casualty.

It went bust in July after pre-tax losses of $1.95bn.

Increasingly strict credit conditions this year have weighed on small-to-mid-cap oil firms, pushing their shares into deeper losses.

The FTSE Aim Oil & Gas Index is down 32% in the year to date whilst the FTSE 350 Oil & Gas Index is down 20%.

The wider European picture for the sector remains just as grim.

In response, many firms have sold their futures to survive in the present.

The number of companies forward-selling crude production has jumped, with prices widely anticipated to stay weaker for longer than thought.

Second-quarter figures showed that oil companies increased their hedging positions compared with the previous year.

Tullow Oil has hedged some 2016 production at an average floor price of $79.29 a barrel, falling to $76.68 in 2017 and $68.04 in 2018.

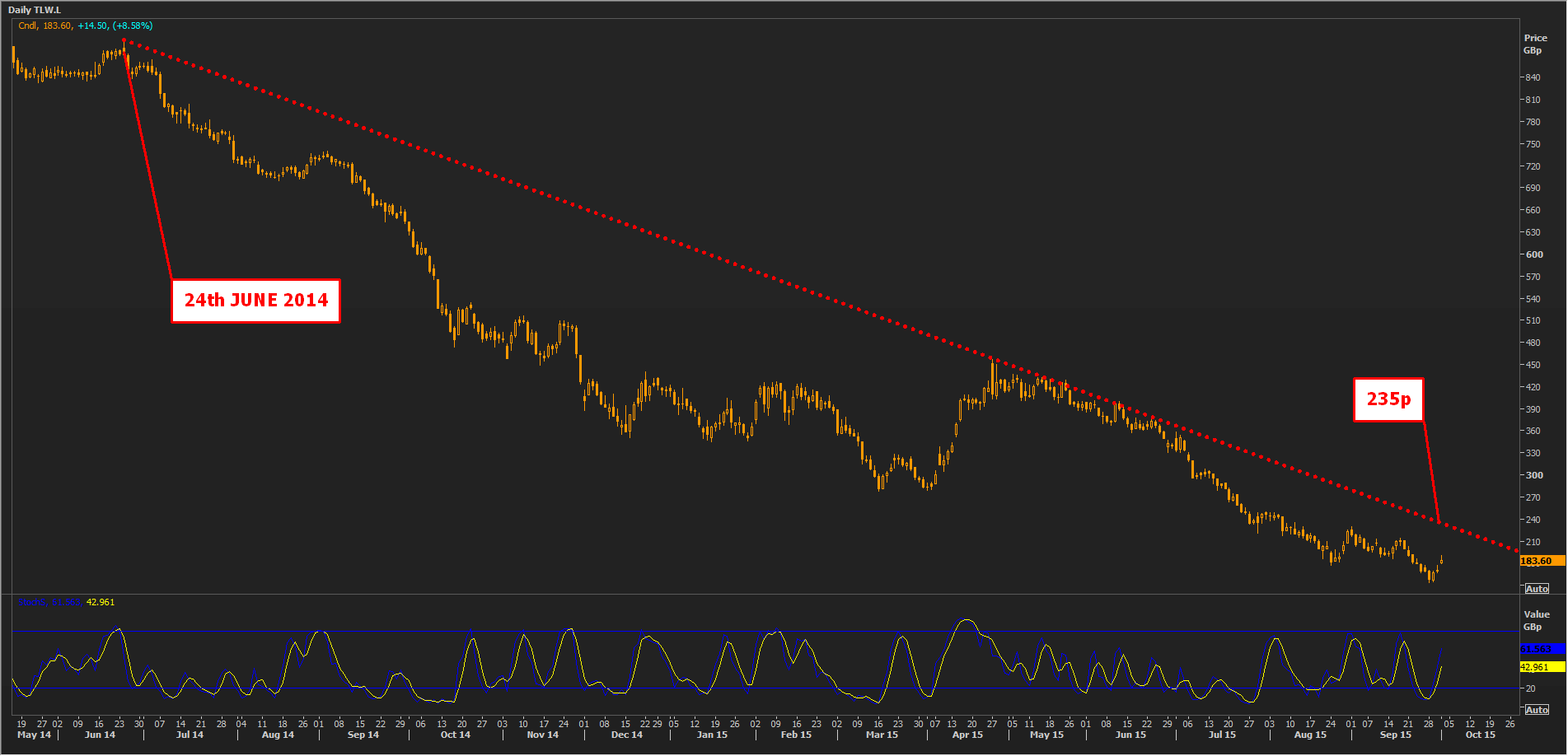

Shares in Tullow, among the most leveraged of UK-based SME oil firms, are 56% lower so far this year.

They hit an all-time closing low of 153.5p on Monday, 90% lower than their peak around 1611p in February 2012.

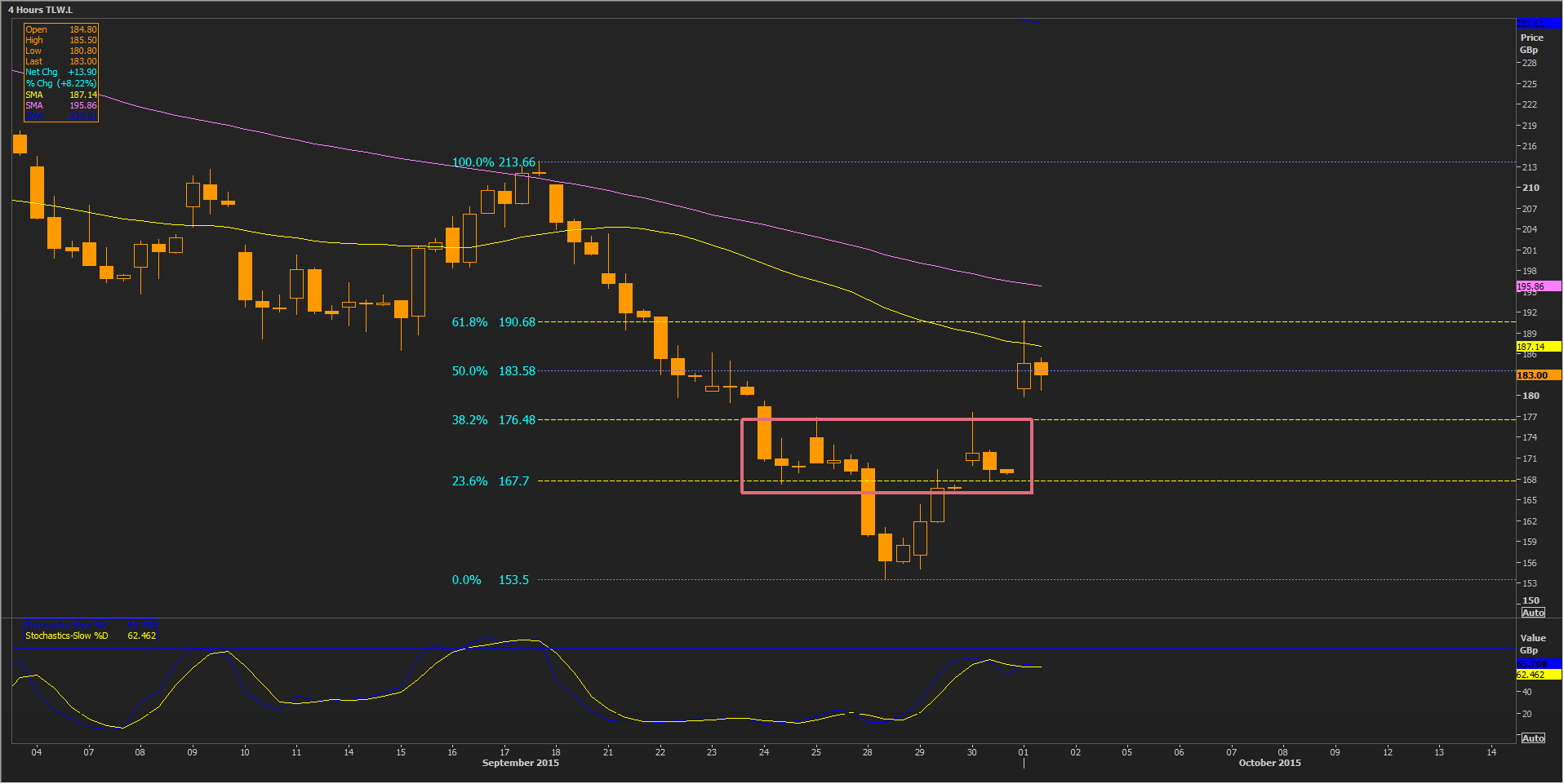

On a relative basis the shares are still floundering, despite Thursday’s bounce.

Thurday’s gains haven’t made it past the 50-period MA and 61.8% interval in a four-hour chart.

Should cheer from the good news dissipate further, the stock looks set to fall back to its near-term support zone between 168p and 177p.

Please click image to enlarge

For the longer term, TLW needs to get above the descending trend that has capped it since 2014.

Whilst oil prices are beneath the level of its hedges, the chances don’t look great.

The nearest point overhead is c. 235p.

Please click image to enlarge