TUI biggest loser easyJet resilient amid 8216 Grexit 8217 fear

Travel stocks led the Greece-fuelled market decline in Europe with dual listed TUI AG, the largest tour operator in the world, a sizeable weight on […]

Travel stocks led the Greece-fuelled market decline in Europe with dual listed TUI AG, the largest tour operator in the world, a sizeable weight on […]

Travel stocks led the Greece-fuelled market decline in Europe with dual listed TUI AG, the largest tour operator in the world, a sizeable weight on both the UK’s flagship FTSE 100 index and Germany’s benchmark DAX30.

TUI fell as hard as 10%-plus on Monday, before recouping about 3 percentage points to trade 7% lower as this article was published with investors weighing both the attack by a lone gunman on holidaymakers in Tunisia and Greece’s suddenly ratcheted-up monetary crisis.

TUI was at the epicentre of travel-related selling which also took Thomas Cook almost 7% lower and airlines, Air France-KLM down 3.8%, IAG 4.5% weaker, easyJet down 3.2% and Ryanair down 3.5% at their weakest.

The Stoxx 600 Travel & Leisure index touched a 6-month low earlier with a 3.1% loss, its deepest since early December.

FTSE 100-listed Coca Cola Hellenic Bottling Co., amongst the largest beverage distributors in Europe, with historic and continuing exposure to Greece, was the sixth-biggest loser by early afternoon on Monday.

As the day has worn on though, all major markets have found their way back from the deepest losses of the session, including the FTSE 100.

The main futures contract based on the gauge of the largest UK-listed stocks, one of the few ways of trading the benchmark directly, recouped 146 points from its weakest levels of Monday by early afternoon.

The most liquid corresponding asset within City Index, the UK100 Daily Funded Trade has also hauled back some losses, regaining more than 50% of Sunday night’s gap lower/Monday morning lows that spanned between approximately 6740 and 6574, at least in the hourly view.

However, with a major momentum study showing the market was within the ‘overbought’ zone, looking at the stochastic sub-chart (bottom) and the price currently vying with a major retracement of the collapse from Friday levels to the worst of Monday’s, absent significant positive Eurozone news, there were reasonable arguments to remove some ‘long risk’.

Please click chart for larger image

In another sign of the somewhat indirect financial market consequences of Greece’s crisis for the UK, a raft of UK asset management shares also stood out on the downside.

The most high-profile, Aberdeen Asset Management slid more than 2% at its worst, but Man Group, Henderson Group, Schroders, Jupiter Fund Management and Ashmore Group all also fell, by between 2% to almost 5%.

Aberdeen Asset Management reportedly saw its biggest outflow for the year so far, last week.

With investors having turned net purchasers of global listed funds for the first time in three months in May, according to Lipper Inc., a provider of mutual and fund market data, the UK fund sector became more exposed to ‘risk-off’ factors, such as Greece’s grasp of Eurozone membership becoming even looser.

EasyJet shares were a moderate 1.5% lower at pixel time, showing some resilience to the wider European sector which was worse off at the time of writing, judging by Thomson Reuters’ Europe Airlines Index which was 2.4% lower, suggesting the stock, like its German peer, Lufthansa, had some features that buffered it from deeper losses.

On a relative basis Lufthansa was already underperforming its European rival carriers and the wider DAX, and Europe-wide STOXX indices by almost 30 percentage points apiece over the year to date.

British Airways-owner International Consolidated Airlines Group (ICAG) was the deepest faller among larger carriers, with a 3% loss intraday.

Despite its on-going takeover saga with Aer Lingus, the Ireland’s government and even European competition regulators, its stock had gained 65% in the year to April.

ICAG’s ties with another troubled Eurozone country, Spain, via ownership of flag carrier Iberia, may also be at the forefront of its investors’ minds today.

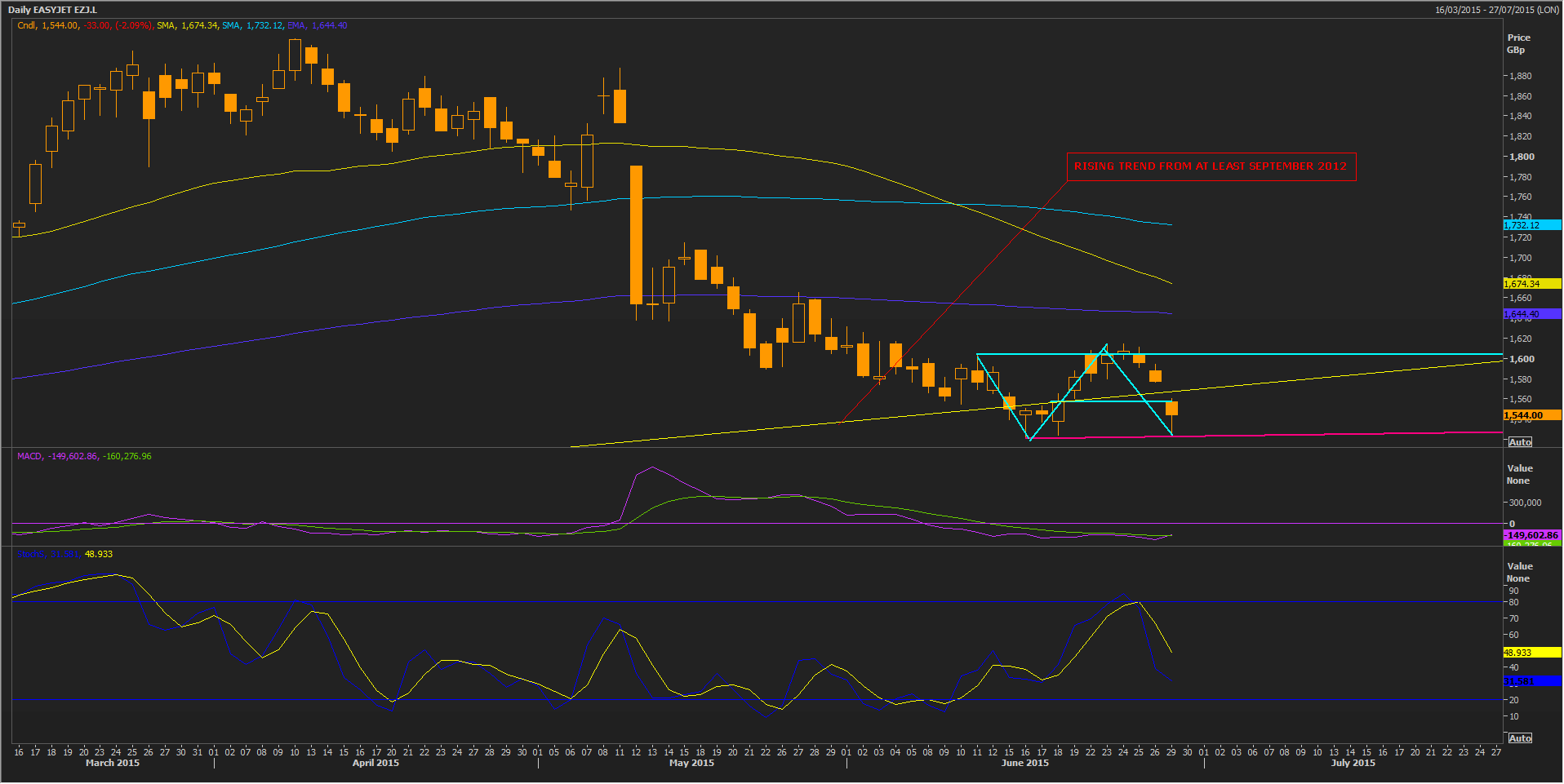

For the sector, this draws a tighter focus on to easyJet, and its relatively contained loss on the day of 1.5%.

Among the better performing European airline shares during the last year, from the beneficial impact of falling fuel costs in line with last year’s slump in crude oil prices, and expanding its total revenue per seat, load factor and passenger numbers—all at the expense of its arch rival Ryanair, the UK-based carrier has hit a spot of turbulence at the start to 2015.

In May the second-largest budget airline in Europe said it expected a negative impact from disruption to service in April from air traffic control strikes in France which caused it to cancel about 600 flights.

EasyJet also warned of a number of previously ‘hidden costs’ in its first half report, although not the kind that tend to upset travellers.

These included an expected rise in fuel costs, a £20m impact from adverse exchange rates, and a potentially higher bill from increased ‘navigation’ charges, mostly referring to air traffic management fees.

However, after losing about 20% in a month, easyJet shares look to be finding support close to January lows, perhaps as investors weighed the potential advantages of joint lobbying last week by Europe’s five largest airlines, who put aside their differences in favour of a united front to urge the EU to lower security and airport charges, remove passenger and “unreasonable” environmental taxes and ensure air-traffic control strikes did not do too much damage to their business.

The EU Transport Commissioner Violeta Bulc is due to unveil a series of measures later this year to boost the competitiveness of the aviation sector.

Obviously, the strongest carriers operating in the Eurozone, such as Ryanair and easyJet stand to benefit the most from the move.

EZJ certainly underpinned its progress in full-year 2014, shown most signally by its load-factor (an airline industry term for how well carriers filled available seats).

This consistently edged ahead of Ryanair’s for several quarters, as the latter struggled with a significant revamp of its cost base and public profile.

EasyJet shares could be buttressed further should they manage to retake levels above an underlying long-term rising trend that commenced in the latter half of 2012.

Currently, that trend would straddle prices between 5678p-5670p, and the stock would meet it after having bounced from supports earlier in June, though EZJ would have to breach resistance in the region of 1557p first.

Please click chart for larger image