March 9, 2020 11:50 PM

Overnight, validation for yesterday’s sharp selloff in key Asian stock markets, as European and U.S. equity markets fell in some cases by the largest amount since 2008, including a 2000 point fall for the Dow Jones. I am old enough to remember when the Dow Jones index falling by 150 points was a big deal!

Covid-19 concerns have been inflamed by the weekend breakdown in OPEC + negotiations and resulted in crude oil yesterday having its sharpest one day fall since 1991. A combination that has fueled fears of a global recession/deflation as well as a credit event.

In an attempt to short circuit the negative cycle in place, it appears a more proactive response by governments and central banks is close by. After cutting rates by 50bp last week, markets are now pricing in a 100% chance that the Federal Reserve will cut by 75bp at its meeting next week.

Furthermore, reports have emerged this morning, that President Trump and his team of advisors will later today announce policy initiatives including paid sick leave and a cut to payroll tax, to ease the fallout from the virus.

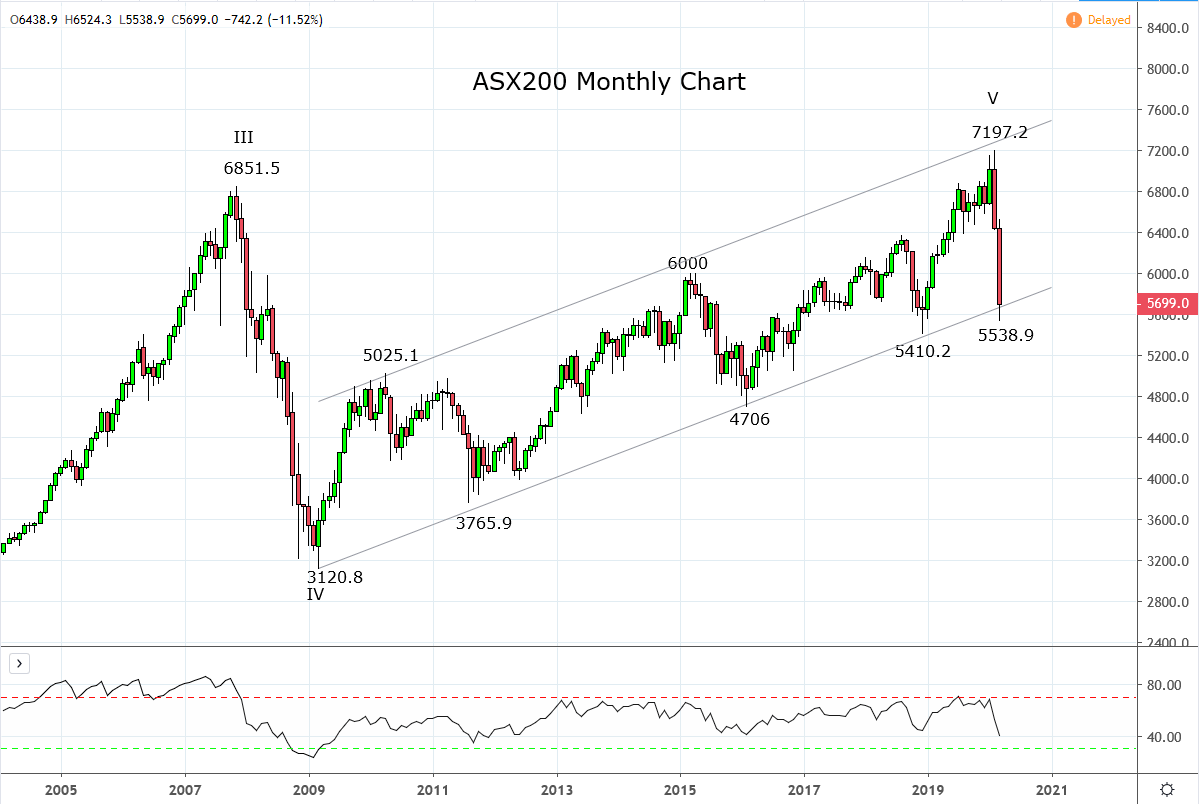

In our articles and videos on the ASX200, we regularly include the monthly chart of the ASX200 below. As can be seen, after a 23% fall over the past two and a bit weeks, the ASX200 earlier today tested and bounced from the trend channel support that has been in place since 2009.

It was leaning against this same trend channel in Mid-February that we advised “For those that bought the January dip, we would consider lightening up longs, particularly if the current rally extends towards the very top of the trend channel 7200/7300 region”. As it turned out 7197.2 was the high a few days later.

In this light, it makes sense to again lean on the well-established trend channel to increase exposure to beaten up equity markets and quality single name stocks in expectation of a recovery. Keeping in mind, that if the ASX200 were to break and close below support at 5400 (December 2018 low), it would warn that a fresh leg lower has commenced.

Source Tradingview. The figures stated areas of the 10th of March 2020. Past performance is not a reliable indicator of future performance. This report does not contain and is not to be taken as containing any financial product advice or financial product recommendation

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Latest Australia 200 articles

February 15, 2024 11:33 PM

February 15, 2024 01:42 AM

February 14, 2024 05:39 AM