Trump Trade v 2 0 weaker dollar and vulnerable stocks

A continuation of yesterday’s risk off tone dominates markets this morning, with the dollar taking another plunge lower in early morning trading. For some time […]

A continuation of yesterday’s risk off tone dominates markets this morning, with the dollar taking another plunge lower in early morning trading. For some time […]

A continuation of yesterday’s risk off tone dominates markets this morning, with the dollar taking another plunge lower in early morning trading. For some time we have spoken out against jumping on the bear-market bandwagon. However, in recent days the market is sending us some signals that could suggest a deeper pullback is on its way.

Lead indicators should worry the bulls

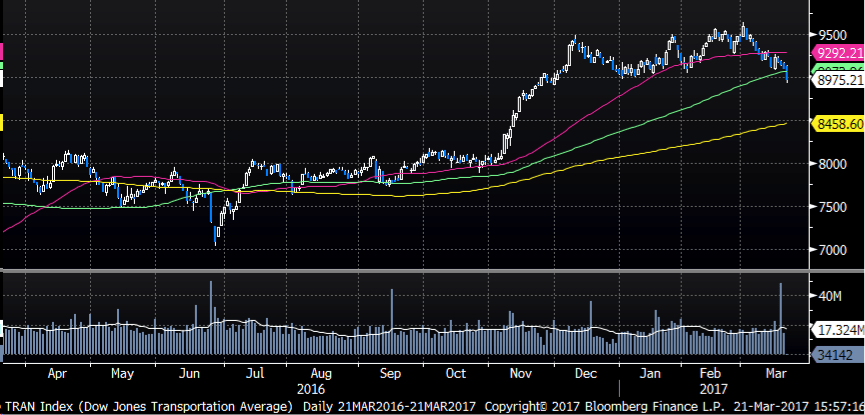

The first signal comes from the traditional lead indicator – the Dow Jones Transport Index. This index has had a rough March and is down more than 7% in the last three weeks. At first, this looked like a regular pause in the uptrend, however, the fact that selling pressure has been virtually consistent all month, the decline of more than 5% and the fall below the 100-day moving average is making us stand up and take notice. If this historical relationship is maintained, then this bodes ill for the broader US indices, which were under pressure again on Tuesday.

Treasury yields suggest risk-off tone

The second signal comes from the Treasury market. The 10-year Treasury yield has dropped more than 20 basis points since last week’s Fed meeting. This is a fairly large move in Treasury yields in just one week, which suggests that there is some nervousness in the market right now. The fact that stocks are falling at the same time as the market is buying Treasuries (hence the decline in yields), suggests that risk aversion has started to grip the market and we could see a broad-based decline in risky asset prices in the coming days and weeks. Watch yields on Wednesday, the 10-year managed to find some support at 2.4%, but if we get another risk-off day then this support level could easily be broken.

Don’t forget the Vix

Added to this, the Vix index, Wall Street’s fear gauge, rose on Tuesday, although it still remains at low levels. If it rises above 13.11 – the high from early February – this would be another bad omen for US stocks, as stocks tend to have a negative correlation with the Vix.

The S&P 500 had its biggest one-day drop since October on Tuesday; the biggest losers in the Dow Jones were the banks, including Goldman Sachs and JP Morgan, along with Caterpillar and Du Pont. The link between these stocks is the Trump trade. Financials and industrials were buoyed when Trump won the US Presidential election last November on the promise of big infrastructure spending and an end to some financial market regulation. However, as we near Trump’s first 100-days in office, there has not been any concrete promise of a infrastructure spending plan and plans to scrap financial market regulation haven’t made it to Congress yet. The big test for Trump comes with Thursday’s scheduled vote in the House on Trump’s healthcare bill. If the bill is passed then it may give the market some confidence in Trump pushing through the rest of his agenda.

A word on the buck

The dollar is also falling sharply, and the dollar index fell below 100.00 on Tuesday, a key support level. It is going to be hard for the buck to rally when Treasury yields are falling. The decline in yields is helping the pound, which was the strongest performer in the G10 on Tuesday and broke above 1.25 in early Wednesday trading. The pound is benefitting from higher levels of UK CPI and an increase in expectations of an interest rate hike: the probability of a rate hike in August jumped to 20% on Tuesday from 7% the week prior. The pound is likely to remain a chief beneficiary of dollar weakness for the next few days due to an unwind of some of GBP short positions, which reached a record low last week as measured by the CFTC.

Looking ahead to Wednesday, there is not too much economic data to change the risk-off tone for financial markets, which we expect to persist for the short-term. Whether or not stocks or the dollar can recover could depend on what Fed chair Janet Yellen, who speaks at 1200 GMT on Thursday, has to say and the healthcare vote in Washington. Until then we expect momentum to remain on the downside, and selling pressure could shift to Europe and Asia on Wednesday.

Figure 1: the decline in the Dow Jones Transport index is worth noting

Source: City index and Bloomberg