Trump blurs risk on risk off line for now

Those who have yet to get a handle on the Trump Trade might just be too late.

Those who have yet to get a handle on the Trump Trade might just be too late.

The widely discussed rotation out of higher-yielding assets like emerging markets (EM), ‘junk’ bonds, growth stocks, etc.—is looking shaky.

Many ‘reflation’ plays are still heading lower after losing momentum at mid-week.

Trump-predicated infrastructure stock buying has also slowed, as reflected by iShares Global Infrastructure ETF.

It has fallen 6.5% since 1st November and closed lower for a fifth session out of seven.

iShares Nasdaq Biotech ETF slipped 0.8% and is down 3.6% since racing 14% higher last week.

Biotech is seen as a beneficiary (like the wider pharma sector) now the threat of tougher price regulation from by Democratic presidential candidate Hillary Clinton has passed.

Another pair of closely watched ‘Trump’ ETFs are counter-trending iShares S&P 500 Growth and iShares S&P 500 Value.

They are designed to reflect similar qualities as ‘growth’ and ‘value’ stocks like groups in new technology and internet spheres, and industrials and utilities respectively.

Value outperformed and Growth slumped in the wake of Trump’s win but that trend has reverted over the last two sessions.

Shares of the highest profile Wall St. banks, Citi, Goldman and JPMorgan bounced on Thursday having slipped a day before.

Their rallies on the back of robust quarterly earnings were reloaded by Trump’s advocacy of lighter-touch financial regulation.

Almost all constituents of the S&P 500 Pharmaceutical Industry sub-index inched up a little on Thursday from declines a day ago, though most only by a little.

Global defence-linked shares have slipped too having been in demand after Trump said NATO members should pick up more of the spending burden from the U.S.

BAE Systems, Lockheed Martin and Raytheon remained weak or lower on Thursday.

Overall, the recent sell-off of EM assets reflects the fact that developed market yields had finally got some wind in their sails.

This brought the highest outflows from such equity markets in 19 weeks, totalling $400m, and the highest DM inflows in 17 weeks at $5bn, according to Bank of America Merrill Lynch’s survey last week.

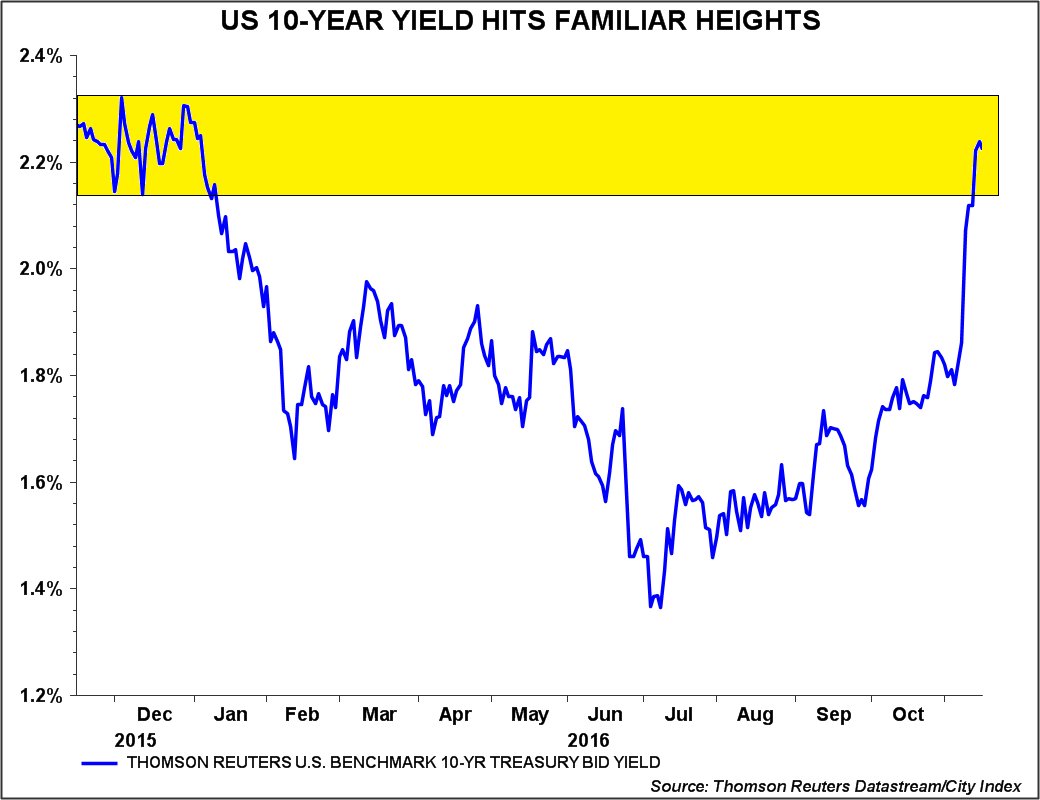

By mid-week though, the bellwether of western borrowing costs, the U.S. 10-year Treasury yield (charted below) was stalling at the same highs that capped it in January.

The last time this happened, bonds saw a sharp and sustained rally that only abated in the summer. By then, the 10-year U.S. yield had backed up by over a percentage point.

Please click image to enlarge

There remains sufficient uncertainty about the near-term outlook for risk to go round for all global investors.

The re-emergence of what many believe to be ‘The Real Donald Trump’ overnight adds another layer.

Signs of erratic and unconventional protocol in arrangements for informal talks with foreign leaders may be rekindling nerves about the President-elect.

His tendency to take to Twitter to conduct verbal retaliation against critics has also resurfaced, and may be another reason for investors to question the wisdom of granting him the benefit of the doubt.

On Thursday, sentiment firmed during Janet Yellen’s testimony on Capitol Hill. It was reassuring in that the likelihood of gradual tightening beyond December was reiterated.

For now, hope as much as conviction may account for the inversion of long-standing market factors that investors have used to gauge whether ‘risk on’ or ‘risk off’ applies.

Lack of clarity may pose risks in itself.