Thought it was all over for the FTSE...It isn't yet

European indices are expected to open higher after steep declines in the previous session.

Concerns over the health of the global recovery, rising Delta cases, the Fed moving towards tapering and weaker commodity prices dragged the UK index to a three-week low on Thursday. A weaker than expected UK GDP could add to growth concerns, although isn't hurting sentiment so far.

GDP for May MoM came in at 0.8% well below the 1.5% growth forecast and down from April's 2% print. With growth already showing signs of slowing, the economy is in need of a leg up. At a stretch this could come from football-induced euphoria translating into some sort of an economic bounce, but that won’t show until July.

The weaker Pound is offering support to the index.

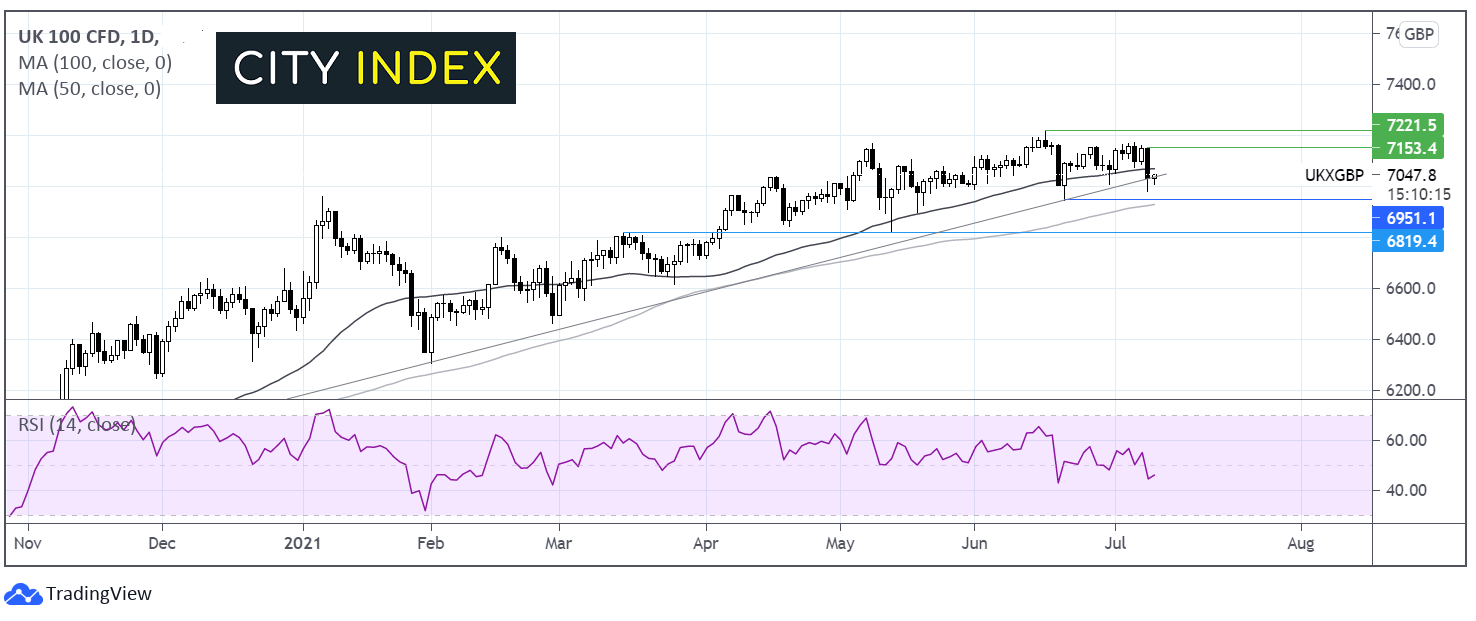

Where next for the FTSE?

Yesterday’s selloff in the FTSE saw the index drop through its 50 day moving average and spike below its ascending trendline dating back to early November. The index also breached 7000 hitting a low 6980 before rebounding.

The RSI is in negative territory but pointing higher, offering mixed signal.

The index is attempting a move higher. Any recovery would need to retake the ascending trendline at 7040 and the 50 sma at 7070 before looking towards yesterday’s high of 7150.

Failure to push back above the ascending trendline could see the FTSE look to take out yesterday’s low of 6980 ahead of 6950 the June 21 low to create a new lower low which could se the sellers gain traction.

EUR/GBP remains below 50 sma, ECB minutes in focus

After getting a kicking in the previous session the Pound is drifting lower versus the Euro in the final session of the week.

The EUR/GBP rose 0.57% on Thursday in its largest one-day rally in two months. The Euro was boosted by the softer tone surrounding the US Dollar and gained despite the ECB moving its inflation goal higher to 2%, a dovish move.

UK GDP data came in weaker than forecast, concerns are growing over the rise of the Delta variant across England and Brexit tensions with the EU over the Northern Ireland protocol are refusing to die down adding to the downbeat mood towards the Pound.

Looking ahead Industrial output from Italy is expected to rise 0.3% month on month in May, down slightly from 1.8% increase in April.

The minutes from the latest ECB meeting are due to be released President Lagarde is also expected to speak.

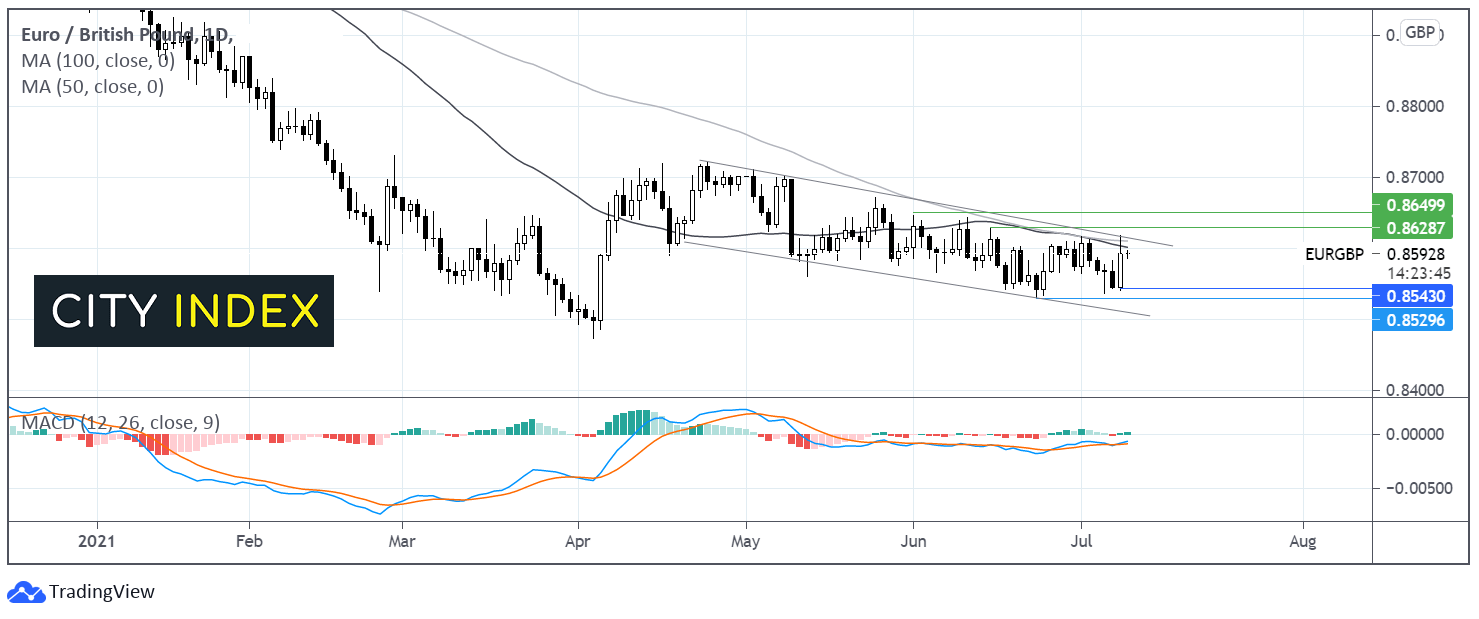

Where next for EUR/GBP?

EUR/GBP has been trading in a descending channel since the highs made in mid-April.

The pair trades below its 50- & 100-day ma keeping the bears hopeful. The MACD is neutral, trading just below the mid-line. A downtick in the MACD could see sellers look towards yesterday’s low of 0.8540 ahead of the June low of 0.8530. Support can also be seen at 0.8510 the lower band of the descending channel.

Any further move higher would need to make a sustained move beyond 0.8600/10 the 50 sma, the 100 sma and the upper band of the descending channel. A break above here could see 0.8625 the June 15 high and 0.8645 the June high.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels

- Place the trade.

Latest market news

Latest EUR articles

April 13, 2024 08:00 PM

March 25, 2024 02:55 AM

January 22, 2024 04:19 AM

January 18, 2024 04:46 AM